Home » Misc » How much do retired air force officers make

How much do retired air force officers make

Pay & Benefits - U.S. Air Force

We can only carry out our mission with the efforts and commitment of our Airmen. That’s why we continue to help them grow with advanced training, ongoing career opportunities and excellent pay and benefits.

BASE SALARY PLUS

In the Air Force, every Airman is paid equally based on their rank and years of service. But your base salary is only part of the over-all package you receive. The moment you put on this uniform you’re also eligible to receive additional compensation based on your job and where you are stationed as well as low-cost insurance, food and housing allowances, 30 days vacation with pay yearly, tuition assistance, and a generous retirement package.

$1,833.30

Entry Level

Payment table

Years

Benefit

< 2 years

$1,833. 30*

2 years

$1,833.30

3 years

$1,833.30

4 years

$1,833.30

6 years

$1,833.30

AIR FORCE BENEFITS

Low-cost insurance

Food and housing allowances

30 days vacation with pay yearly

Tuition assistance

Generous retirement package

$2,054.70

Entry Level

Payment table

Years

Benefit

< 2 years

$2,054. 70

2 years

$2,054.70

3 years

$2,054.70

4 years

$2,054.70

6 Years

$2,054.70

AIR FORCE BENEFITS

Low-cost insurance

Food and housing allowances

30 days vacation with pay yearly

Tuition assistance

Generous retirement package

$2,160.60

Entry Level

Payment table

Years

Benefit

< 2 Years

$2,160. 60

2 Years

$2,435.70

3 Years

$2,435.70

4 Years

$2,435.70

6 Years

$2,435.70

AIR FORCE BENEFITS

Low-cost insurance

Food and housing allowances

30 days vacation with pay yearly

Tuition assistance

Generous retirement package

$2,393.40

Entry Level

Payment table

Years

Benefit

< 2 Years

$2,393. 40

2 Years

$2,515.80

3 Years

$2,652.00

4 Years

$2,786.70

6 Years

$2,905.50

AIR FORCE BENEFITS

Low-cost insurance

Food and housing allowances

30 days vacation with pay yearly

Tuition assistance

Generous retirement package

$2,610.30

Entry Level

Payment table

Years

Benefit

< 2 Years

$2,610. 30

2 Years

$2,786.10

3 Years

$2,920.80

4 Years

$3,058.50

6 Years

$3,273.30

AIR FORCE BENEFITS

Low-cost insurance

Food and housing allowances

30 days vacation with pay yearly

Tuition assistance

Generous retirement package

$2,849.40

Entry Level

Payment table

Years

Benefit

< 2 Years

$2,849. 40

2 Years

$3,135.60

3 Years

$3,274.20

4 Years

$3,408.60

6 Years

$3,548.70

AIR FORCE BENEFITS

Low-cost insurance

Food and housing allowances

30 days vacation with pay yearly

Tuition assistance

Generous retirement package

$3,294.30

Entry Level

Payment table

Years

Benefit

< 2 Years

$3,294. 30

2 Years

$3,595.50

3 Years

$3,733.50

4 Years

$3,915.30

6 Years

$4,058.10

AIR FORCE BENEFITS

Low-cost insurance

Food and housing allowances

30 days vacation with pay yearly

Tuition assistance

Generous retirement package

01

INSURANCE

The Air Force provides our Airmen and their families with world-class insurance plans. They receive excellent rates, low cost, comprehensive medical and dental care at military or civilian facilities, full pay and allowances for sick days and low-cost life insurance.

02

FOOD AND HOUSING

The Air Force takes care of the basic needs of every Airman. Living expenses, including utilities and maintenance, are covered for those who choose to live in on-base housing. A monthly tax-free housing allowance based on rank, family status and geographic location is provided for off-base residents to help pay for living expenses.

Food allowances are also provided, and single Airmen have a meal account that allows them to eat as many as four meals a day in the on-base dining facility for free. Tax-free, on-base department and grocery stores also help costs to continue to stay low.

03

RETIREMENT

The Air Force provides a generous retirement plan. Airmen are eligible to retire after 20 years of service and begin receiving benefits the day they retire. The Air Force retirement plan requires no payroll deductions. Those who’d like to save a little extra each month can take part in the Thrift Savings Plan (TSP)*, which allows participants to place a portion of their monthly pay into an account similar to a 401(k) investment plan.

*TSP contributions are considered pretax dollars and therefore reduce the amount of income subject to tax, and the accounts grow tax-free. Enrollment is available when members first join the military and anytime thereafter. Unlike traditional military retirement, which requires a commitment of at least 20 years of active duty, money invested in the TSP belongs to individual members, no matter how many years they serve. Income contributed to the TSP is not taxed until withdrawn from the account. Withdrawal before age 59½ may be subject to penalty; however, the TSP accounts can be rolled over into an IRA or another employer’s retirement account.

04

RECREATION

Most Air Force bases have golf courses, arts and crafts facilities, bowling alleys, tennis courts, swimming pools and even equipment rentals, which can be either used for free or at better rates than similar facilities or options off base.

Every base is also equipped with social activities and recreational programs geared toward the interests of every family member. These include Enlisted and Officer Clubs, base sponsored youth activities and youth centers where children can spend time in a safe environment.

05

VACATION AND TRAVEL

All Airmen receive 30 days of vacation with pay, during which they are free to travel and take time to explore local and foreign destinations. Airmen can take advantage of available space on Air Force aircraft to travel to many international destinations as well as almost any state in the U. S. For destinations near another military facility, they can enjoy hotel-quality lodging on base for a reduced cost.

06

EDUCATION

The Air Force offers an array of educational opportunities so you can achieve your true potential. On day one you’ll be enrolled in Community College of the Air Force earning college credit starting with Basic Military Training. The Air Force also offers scholarships to outstanding Airmen who wish to attend or complete their college education. Or you can receive up to 100% tuition assistance through the Air Force Tuition Assistance program, the Post-9/11 GI Bill, or the Montgomery GI Bill.

Value of Military Retirement: Over One Million Dollars

That’s a bold headline, especially if you are a retired enlisted military member only bringing in a little over a thousand dollars a month in retirement pay. But it’s true. Military retirement is worth well over a million bucks. In some cases, it is worth millions of dollars.

Before we get too deep into this, I want to define what I am talking about. I’m talking about two factors – the long-term value regarding how much you will receive in a direct pension over the lifetime of your retirement benefits and the value of the retirement benefits, including healthcare coverage and other benefits. Combined, these benefits are easily worth over a million dollars, even if you don’t have the spending power of a million dollars right now.

How Much is Military Retirement Really Worth?

Take an example of retirement pay for an average military career. Since military members are eligible for retirement benefits at 20 years, we will use a reasonable rank and service time for our examples.

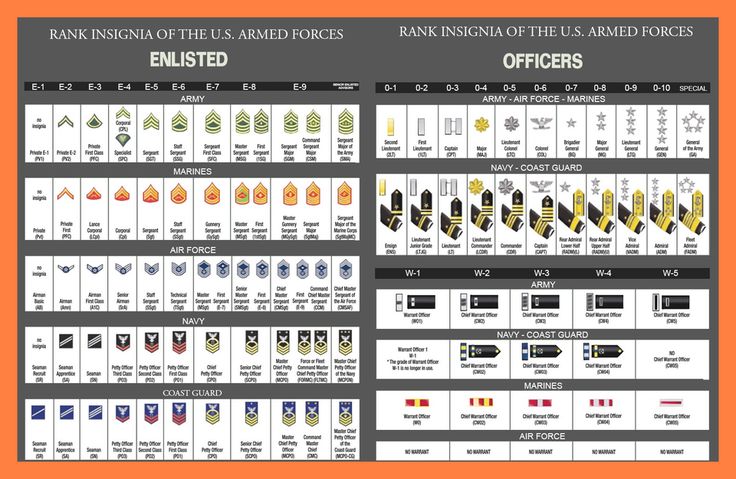

It is reasonable to assume that the average enlisted member will be able to retire at 20 years, having achieved the rank of E-7, and the average officer should be able to retire at 20 years at the rank of O-5.

Of course, there will be outliers based on when you served, your career field, and other factors, but these ranks and service times should apply to the majority of careers (if anything, I am aiming at the conservative side because many people choose to serve longer than the 20-year mark, earning an extra 2.5%-3.5% on their retirement pay per additional service year, depending on whether they take the high 36 retirement plan or the Redux retirement plan).

Track your TSP and other investments with Personal Capital’s free financial dashboard

Example Monthly and Annual Military Retirement Pay

As we mentioned, we will look at a military retiree with 20 years of service at the ranks of E-7 for enlisted and O-5 for officers. The base pay for these ranks in 2009 is:

E-7 Monthly: $5,232.46

E-7 Annually: $62,789.52

O-5 Monthly: $10,081.03

O-5 Annually: $120,972. 36

Example 1 High-36 Retirement Plan

Most retirees under the High-36 Plan will receive 50% of their base pay at 20 years, which would equal the following amounts:

E-7 Monthly: $2,616.23

E-7 Annually: $31,394.76

O-5 Monthly: $5,040.515

O-5 Annually: $60,486.18

Example 2 Blended Retirement System

Those under the BRS would receive 40% of their base pay at 20 years (2% per year of service), which would be the following amounts:

E-7 Monthly: $2,092.98

E-7 Annually: $25,115.81

O-5 Monthly: $4,032.41

O-5 Annually: $48,388.94

How Much is Military Retirement Pay Worth Over a Lifetime?

The next factor to consider is that military retirement pay will be there day in and day out. There are few places in the world that someone can receive a lifetime pension starting at or around age 40. Many military retirees will receive a monthly cash payment for over 40 years. When you add in the cost of living and inflation adjustments, we’re talking about some serious cash!

Using the numbers above from a recently retired E-7 or O-5, we get the following lifetime payments (note: these military retirement pay numbers are not adjusted for inflation and do not include any COLA increases; this is not a planning tool, but for illustration purposes only. Your specific retirement benefits will vary based on your situation):

Cumulative Retirement Pay Under High 36

E-7 retirement pay for 20 years: $627,895.20

E-7 retirement pay for 30 years: $941,842.80

E-7 retirement pay for 40 years: $125,5790.40

O-5 retirement pay for 20 years: $1,209,723.60

O-5 retirement pay for 30 years: $1,814,585.40

O-5 retirement pay for 40 years: $2,419,447. 20

Cumulative Retirement Pay Under BRS:

E-7 retirement pay for 20 years: $502,316.20

E-7 retirement pay for 30 years: $753,474.30

E-7 retirement pay for 40 years: $100,4632.40

O-5 retirement pay for 20 years: $967,778.80

O-5 retirement pay for 30 years: $1,451,668.20

O-5 retirement pay for 40 years: $1,935,557.60

Even without COLA or other inflation adjustments, we can see that we are reaching some serious numbers. Each additional year you serve before you retire can add another 2.5% to your monthly and annual pay, and each higher pay grade you achieve can add hundreds or even thousands of dollars per year. As previously mentioned, the numbers used in this article are meant to be a conservative estimate.

OK, there is a minimal TriCare payment, but compared to what civilians pay, it is basically a non-issue. Benefits for retired military members are also guaranteed – they won’t drop you after you have required expensive procedures or for pre-existing conditions. Guaranteed medical coverage is a massive blessing in today’s American society. Here is a little more information about the kinds of insurance available to civilians: comparing individual and group health insurance. Hopefully, that will help you better understand the value of military retiree medical benefits!

Military-sponsored medical benefits are incredibly valuable, especially as you get older and when they cover your spouse. There are very few civilian plans that are similar to this. Most people spend several thousand dollars per year for basic medical coverage, which doesn’t include out-of-pocket expenses for doctor visits, medical procedures, prescription medication, or other associated costs.

It would not be unreasonable to place a value of $15,000-$20,000 per year on military retiree medical benefits, even for a healthy individual. Add a spouse to the benefits, guaranteed coverage, and little to no out-of-pocket expenses for complex medical procedures. Other factors and the medical benefits alone can be worth hundreds of thousands of dollars or more throughout a lifetime (and sometimes into the millions of dollars for people who receive complex medical care over a long-term period).

Commissary, Base Exchange, and other Base Benefits

I won’t even try to assign a value to these benefits because they don’t apply to all military retirees equally. Some people may practically live on base, visiting the base clubs, shopping at the exchanges, using the gyms, auto hobby shops, etc., and others may not live near a base. They may not be able to take advantage of any of these benefits. So this category falls in the “good deal if you can get it” benefit but is not a core part of the equation. But it is worth mentioning because many retirees save a lot of money each year by shopping on base.

How to Calculate the Present Value of a Military Retirement Pension

One challenge to the analysis is that the military pension includes a cost of living adjustment, so the amount of the income stream has to rise every year by the rate of inflation.

Another problem is that no one knows how long the pensioner will live, so it’s difficult to predict how long the pension will be paid out.

Finally, the calculated lump sum must be invested in a safe and stable asset to ensure it survives for decades. Unfortunately, the safe and stable assets have a very low yield, so it takes a larger lump sum to produce an income stream big enough to pay the pension.

The answer to these puzzles involves the mathematical process of “discounting”.

Accountants and actuaries devote their entire careers to studying asset yields, human longevity, and other risks. They calculate the statistical probability that a specific lump sum can pay a particular pension for the necessary number of years.

The good news for pension recipients is that the calculations are much more accurate when the analysis is simultaneously applied to hundreds of thousands of pensions as a group. Even better, the Department of Defense can rely on the number-crunching skills of another giant bureaucracy of inflation-adjusted payments: Social Security.

The mathematical details of discounting an inflation-adjusted annuity are well beyond the scope of this post. There’s not an easy formula to convert that $100/day pension to a precise lump sum. However, a few more straightforward estimates are reasonably close to the more complicated methods.

The easiest estimate assumes that a military pension keeps up with inflation. This eliminates the more complicated factors of correcting future dollars for inflation. If a military pension keeps up with inflation then the pension’s value in today’s dollars stays constant. The lump-sum value of the pension is the total amount to be received during the rest of the veteran’s life:

Lump sum = (annual pension amount) * (remaining life expectancy)

A 38-year-old veteran receiving $3000/month with a COLA might reasonably look forward to 35 more years of life. The estimate of the present value of their pension would be

The life-expectancy estimate ignores other discounting factors in favor of simplicity and speed. Its main advantage is that veterans can quickly estimate a lump sum for their expected lifespan. Veterans in good health with long-lived ancestors may decide that they have 40 or even 50 years of retirement, raising the current value of their pension.

Another quick estimate is to assume that the pension is the income stream from a lump sum of Treasury Inflation-Protected Securities (TIPS). TIPS are an extremely safe and stable asset with built-in inflation protection. The market for buying and selling TIPS is huge and liquid, so their prices are reasonably accurate.

One flaw of this estimate is that, unlike a military pension, when the pensioner dies, there’s still a lump sum of TIPS generating a stream of income. Another drawback is that a TIPS’ maturity (now a maximum of 30 years) is usually less than the pensioner’s remaining life expectancy.

The advantage of this estimate is simplicity and speed:

Lump sum = (annual pension) / (TIPS annual percentage yield)

A January 2009 Treasury auction sold 20-year TIPS at an inflation-adjusted annual percentage yield of 2.5%. So for that $3000/month pension,

Another estimate of the lump-sum value of an inflation-adjusted pension is a commercial annuity. The annuity market is generally regarded as liquid because insurance companies compete to offer the “best” price without losing money. However, they still charge more than the actual value of the annuity to make their profit.

Insurance companies could be unable to make annuity payments or even go bankrupt and should be considered a riskier source of annuity payments than TIPS or other government bonds.

One of the “less risky” annuities comes from an agency sponsored by the federal government– the Thrift Savings Plan. TSP annuities are purchased from an insurance company. The federal government does not guarantee them, but the insurance company is presumably charging a smaller fee (to sell a large volume of annuities), and the annuity’s cost would be closer to its value.

TSP annuities are priced monthly and do not offer complete protection against inflation. The advantage of estimating a pension’s lump-sum value from a TSP annuity is its lower price and the TSP website’s calculator. Assuming that the $3000/month pension is paid to a 38-year-old veteran and limited to 3% annual inflation:

Lump sum (TSP website annuity calculator) =$1.4 million.

$1.4 million is the price that a veteran would pay in the market to buy a TIPS portfolio or an annuity that would yield their inflation-adjusted pension of $3000/month for the rest of their life. Other research analyzes the theoretical cost of annuities and discounted values– only the cost and not its market price. (This includes a research paper on military pensions– the citation is in the book.)

These estimates range from about $1 million to $1.2 million. They’re only theoretical estimates. These annuities can’t actually be purchased like the assets of the other estimates, but they’re a more conservative estimate of the probabilities of longevity and other risk factors.

Let’s get back to the veteran who’s just finished 10 years of service and is wondering if it’s worth staying in the military for another decade. After analyzing the pension’s present value, which sounds more compelling now: $100/day, or lifetime income of over $1 million?

Your military retirement is worth millions

Thousands of dollars coming in regularly quickly add up over the years. Add in increases for inflation, essentially free health care, and other benefits, and you can see how a military retirement can quickly be worth millions of dollars over a lifetime.

I didn’t stay in long enough to qualify for military retirement benefits – I separated from the USAF with an Honorable discharge after 6.5 years of service. Part of me looks at the military retirement system with a bit of longing. It is an excellent system for those who qualify, and I would love to be able to receive military retirement benefits for the rest of my life. However, separating from the military was the best move for me at the time, and I have no regrets regarding my separation or my military service. I am proud to have served, and the military is a large part of who I am today.

*disclaimer about this article: The calculations are for illustrative purposes only and do not reflect the exact retirement benefits you will receive. This is a simplified look at military retirement benefits and does not take many factors into consideration, including taxes, disability benefits, inflation, COLA, and other factors.

About Post Author

Ryan Guina

Ryan Guina is The Military Wallet’s founder. He is a writer, small business owner, and entrepreneur. He served over six years on active duty in the USAF and is a current member of the Illinois Air National Guard.

Ryan started The Military Wallet in 2007 after separating from active duty military service and has been writing about financial, small business, and military benefits topics since then.

Featured In: Ryan’s writing has been featured in the following publications: Forbes, Military.com, US News & World Report, Yahoo Finance, Reserve & National Guard Magazine (print and online editions), Military Influencer Magazine, Cash Money Life, The Military Guide, USAA, Go Banking Rates, and many other publications.

See author's posts

90,000 Pension Israel: the hardest way to repatriates

70

70 60

60 40

40 30

30 40

40 30

30 They receive excellent rates, low cost, comprehensive medical and dental care at military or civilian facilities, full pay and allowances for sick days and low-cost life insurance.

They receive excellent rates, low cost, comprehensive medical and dental care at military or civilian facilities, full pay and allowances for sick days and low-cost life insurance. Airmen are eligible to retire after 20 years of service and begin receiving benefits the day they retire. The Air Force retirement plan requires no payroll deductions. Those who’d like to save a little extra each month can take part in the Thrift Savings Plan (TSP)*, which allows participants to place a portion of their monthly pay into an account similar to a 401(k) investment plan.

Airmen are eligible to retire after 20 years of service and begin receiving benefits the day they retire. The Air Force retirement plan requires no payroll deductions. Those who’d like to save a little extra each month can take part in the Thrift Savings Plan (TSP)*, which allows participants to place a portion of their monthly pay into an account similar to a 401(k) investment plan.

S. For destinations near another military facility, they can enjoy hotel-quality lodging on base for a reduced cost.

S. For destinations near another military facility, they can enjoy hotel-quality lodging on base for a reduced cost. Military retirement is worth well over a million bucks. In some cases, it is worth millions of dollars.

Military retirement is worth well over a million bucks. In some cases, it is worth millions of dollars.

36

36 Many military retirees will receive a monthly cash payment for over 40 years. When you add in the cost of living and inflation adjustments, we’re talking about some serious cash!

Many military retirees will receive a monthly cash payment for over 40 years. When you add in the cost of living and inflation adjustments, we’re talking about some serious cash! 20

20 personalcapital.com%2F”>Visit PersonalCapital.com</a>

personalcapital.com%2F”>Visit PersonalCapital.com</a>

But it is worth mentioning because many retirees save a lot of money each year by shopping on base.

But it is worth mentioning because many retirees save a lot of money each year by shopping on base.

The estimate of the present value of their pension would be

The estimate of the present value of their pension would be Another drawback is that a TIPS’ maturity (now a maximum of 30 years) is usually less than the pensioner’s remaining life expectancy.

Another drawback is that a TIPS’ maturity (now a maximum of 30 years) is usually less than the pensioner’s remaining life expectancy.

Other research analyzes the theoretical cost of annuities and discounted values– only the cost and not its market price. (This includes a research paper on military pensions– the citation is in the book.)

Other research analyzes the theoretical cost of annuities and discounted values– only the cost and not its market price. (This includes a research paper on military pensions– the citation is in the book.)

He is a writer, small business owner, and entrepreneur. He served over six years on active duty in the USAF and is a current member of the Illinois Air National Guard.

He is a writer, small business owner, and entrepreneur. He served over six years on active duty in the USAF and is a current member of the Illinois Air National Guard.