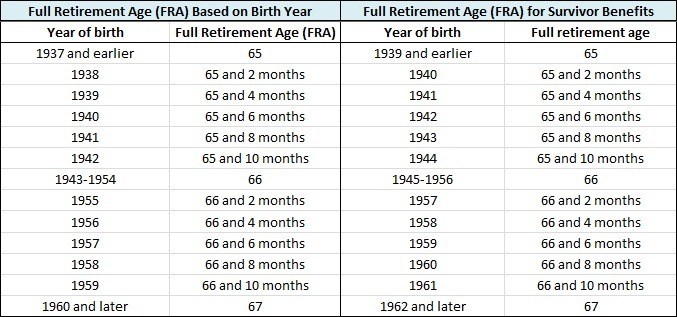

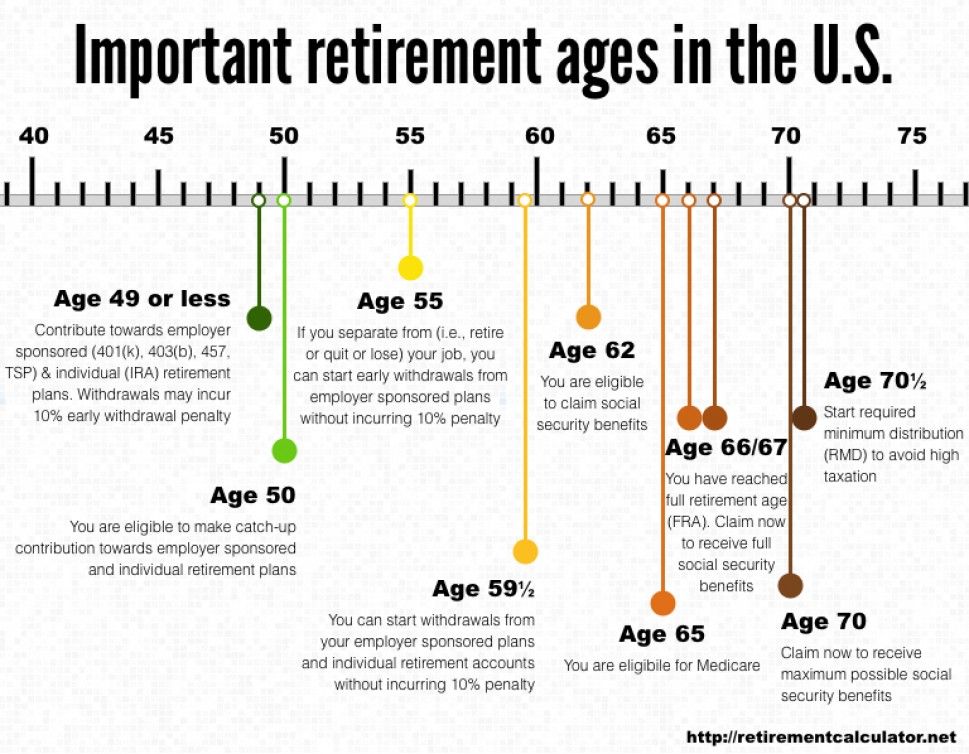

| When To Start Receiving Retirement Benefits Benefit calculators How we calculate benefits | Workers planning for their retirement should be aware that retirement benefits depend on age at retirement. If a worker begins receiving benefits before his/her normal (or full) retirement age, the worker will receive a reduced benefit. A worker can choose to retire as early as age 62, but doing so may result in a reduction of as much as 30 percent. Starting to receive benefits after normal retirement age may result in larger benefits. With delayed retirement credits, a person can receive his or her largest benefit by retiring at age 70. | Early retirement reduces benefits | In the case of early retirement, a benefit is reduced 5/9 of one percent for each month before normal retirement age, up to 36 months. For example, if the number of reduction months is 60 (the maximum number for retirement at 62 when normal retirement age is 67), then the benefit is reduced by 30 percent. This maximum reduction is calculated as 36 months times 5/9 of 1 percent plus 24 months times 5/12 of 1 percent. | Delayed retirement increases benefits | Delayed retirement credit is generally given for retirement after the normal retirement age. To receive full credit, you must be insured at your normal retirement age. No credit is given after age 69. If you retire before age 70, some of your delayed retirement credits will not be applied until the January after you start benefits. The calculator below gives you the amount with all credits applied for comparison purposes. Delayed retirement credits increase a retiree's benefits. The table below shows the delayed retirement credit by year of birth. | Compute the effect of early or delayed retirement | If you enter your date of birth and the effective month for beginning your benefits, we will tell you the effect of early or delayed retirement as a percentage of your primary insurance amount. Please note that benefits are generally paid in the month following the effective month.

The month you will reach your normal retirement age is . |

Many adults look forward to retirement and some wouldn’t mind leaving the workforce a little earlier than they are expected to. However, few people think about the drawbacks of retiring early, especially if they haven’t thought through and fully planned out the decision for years. Few realize that early retirement might affect their long-term financial plan and their access to certain social security benefits. A financial advisor can help you figure out all of your retirement and social security issues.

However, few people think about the drawbacks of retiring early, especially if they haven’t thought through and fully planned out the decision for years. Few realize that early retirement might affect their long-term financial plan and their access to certain social security benefits. A financial advisor can help you figure out all of your retirement and social security issues.

The earliest you can start receiving Social Security benefits is age 62. The earlier you elect to receive your benefits, however, the smaller your monthly checks will be (decreasing by as much as 30%). To receive full benefits, you will have to avoid collecting Social Security until you reach your full (or normal) retirement age. For people born in 1960 or later, that age is 67. And with the delayed retirement credits, you can get your largest benefit at age 70.

If you decide to retire early, you have the option of delaying your Social Security benefits. This strategy may work particularly well for married couples but you have to factor in the amount of time you’ll need to fund your lifestyle until social security kicks in.

This strategy may work particularly well for married couples but you have to factor in the amount of time you’ll need to fund your lifestyle until social security kicks in.

If you’re wondering how much you’ll get from Social Security, you can check out our Social Security calculator. It estimates how much you’ll earn depending on your annual income, the year you were born and when you choose to start receiving benefits.

The calculations for Social Security benefits come from your highest 35 years of earnings. That’s how the Social Security Administration comes up with your average monthly indexed earnings (AIME). If you retire too early (i.e. before earning a paycheck for at least 35 years), you’ll receive less Social Security. That’s the downside to early retirement.

By retiring early, you’ll also miss out on the chance to claim delayed retirement credits. Social Security increases a percentage of your retirement benefits each month that you delay after full retirement age until you turn 70. So if your full retirement age is 67 but you avoid taking Social Security until three years later, then you can claim 124% of your full monthly benefit amount.

So if your full retirement age is 67 but you avoid taking Social Security until three years later, then you can claim 124% of your full monthly benefit amount.

The table below comes from the Social Security Administration’s benefits retirement planner and calculates the monthly increase rate by birth year:

| Delayed Retirement Increase | |||||

| 1933 to 1934 | 5.5% | 11/24 of 1% | |||

| 1935 to 1936 | 6% | 1/2 of 1% | |||

| 1937 to 1938 | 6.5% | 13/24 of 1% | |||

| 1939 to 1940 | 7% | 7/12 of 1% | |||

| 1941 to 1942 | 7.5% | 5/8 of 1% | |||

| 1943 and later | 8% | 2/3 of 1% | |||

By comparison, if you choose to retire early, your Social Security check gets reduced by 5/9 of 1% for each month you collect benefits before your full retirement age (up to 36 months). If you retire more than 36 months early (up to a maximum of 60), your Social Security benefit will be reduced by an additional 5/12 of 1% per extra month.

If you retire more than 36 months early (up to a maximum of 60), your Social Security benefit will be reduced by an additional 5/12 of 1% per extra month.

This means that the maximum number of retirement months is 60 for those retiring at age 62 when the full retirement age is 67. So your benefits could be reduced by up to 30%. Social Security calculates this maximum by multiplying 36 months by 5/9 of 1% and then adds a total of 24 months multiplied by 5/12 of 1%.

What If I Want to Work in Retirement?Sometimes leaving the workforce is neither feasible nor appealing. That’s why some retirees find part-time jobs to pass the time or earn extra money. Getting a part-time job after retiring early may reduce your benefit amount until you reach full retirement age. The SSA may withhold a certain amount of money from your benefit check if your earnings exceed the annual limit. For 2022, your benefits will be reduced by $1 for every $2 you earn above $19,560.

If you’ll reach your full retirement age in 2022, your benefits will be reduced by $1 for every $3 you earn above a different limit ($51,960) up until the month you turn 67. For comparison, benefits were reduced in 2020 by $1 for every $2 earned above $18,240 and reduced by $1 for every $3 earned above $48,600 for those who reached full retirement age that year.

For comparison, benefits were reduced in 2020 by $1 for every $2 earned above $18,240 and reduced by $1 for every $3 earned above $48,600 for those who reached full retirement age that year.

The SSA doesn’t penalize working retirees forever. You’ll receive all of the benefits the government withheld after you reach your full retirement age. At that time, the SSA recalculates your benefit amount.

Can Too Many Early Retirees Affect Social Security?Regardless of when you retire, you’ll receive around the same amount of Social Security benefits over your lifetime. This is due to cost-of-living adjustments that attempt to protect seniors from inflation.

In other words, Social Security balances itself out. Early retirees receive lower monthly benefits over a long period of time while late retirees receive larger benefit amounts over a short period of time. Retiring early does not affect the Social Security program’s finances because the amount of benefits available does not depend on how early or late someone retires.

Not everyone can retire early. But let’s say you’re preparing to quit your job before you reach your full retirement age. In that case, it’s important to think about how that might affect the size of your Social Security checks. If you can wait to take Social Security, you’ll end up with larger benefit checks. Whatever you choose to do, it’s best to make sure your money will last throughout your entire retirement.

Tips for Retirement Planning An easy way to get ahead on saving for retirement is by taking advantage of employer 401(k) matching.

An easy way to get ahead on saving for retirement is by taking advantage of employer 401(k) matching.Photo credit: ©iStock.com/DNY59, ©iStock.com/gpointstudio, ©iStock.com/DragonImages

Lauren Perez, CEPF® Lauren Perez writes on a variety of personal finance topics for SmartAsset, with a special expertise in savings, banking and credit cards. She is a Certified Educator in Personal Finance® (CEPF®) and a member of the Society for Advancing Business Editing and Writing. Lauren has a degree in English from the University of Rochester where she focused on Language, Media and Communications. She is originally from Los Angeles. While prone to the occasional shopping spree, Lauren has been aware of the importance of money management and savings since she was young. Lauren loves being able to make credit card and retirement account recommendations to friends and family based on the hours of research she completes at SmartAsset.

Cherkessk, November 8, 2021. On January 1, 2019, Federal Law No. 350-FZ “On Amendments to Certain Legislative Acts of the Russian Federation on the Assignment and Payment of Pensions” came into force, aimed at ensuring a balance and long-term financial stability of the pension system.

Changes approved in accordance with the law fix the generally established retirement age at 65 for men and 60 for women. The increase in the retirement age is gradual and will last until 2028.

At the same time, changes in the retirement age will not affect people who have early retirement benefits. For example, miners, miners, rescuers, as well as other workers employed in difficult, dangerous and harmful working conditions, for which employers pay additional contributions to pension insurance. For the majority of such workers, as before, the right to retire comes upon reaching the age of 45 (list 1) and 50 years (list 2) for women, 50 years (list 1) and 55 years (list 2) for men.

The right to early retirement is also retained by teachers, doctors and representatives of other professions, who receive payments after acquiring the required length of service. At the same time, from 2019, the appointment of a pension for this category of workers is postponed, taking into account the transition period from the moment of acquiring the required length of service by profession.

The right to early retirement is also reserved for persons whose pensions are awarded for social reasons. So, for example, for women with five children, the visually impaired, parents and guardians of the disabled and other citizens, early exit remains completely unchanged.

But there were also norms in the law concerning women who gave birth and raised three and four children, which cause a large number of appeals.

For clarifications, we turned to Irina Tambiyeva, Deputy Head of the GU-OPFR for the KChR.

As Irina Viktorovna explained, according to the amendments and additions made to Article 32 of the Federal Law of December 28, 2013 N 400-FZ "On Insurance Pensions", a mother of three children will be able to retire early at the age of 57, and a mother of four children - at age 56, subject to transitional provisions. The main requirements are 15 years of insurance experience, the required number of pension points and raising a child up to 8 years old.

The main requirements are 15 years of insurance experience, the required number of pension points and raising a child up to 8 years old.

Also in the law there was a norm giving the right to retire 2 years earlier than the generally established retirement age for a long insurance period: for women - 37 years of experience, for men - 42 years of experience.

As before the amendments to the legislation, in order to receive a pension in 2021, the minimum requirements for the length of the insurance period and the number of pension points must be met. The right to a pension this year will be given to people with 12 years of service and 21 pension coefficients.

*For women born in the indicated years, it is advantageous to take out an old-age insurance pension on a general basis.

Please note that the changes in the law do not affect the social disability and survivor's pensions, which are assigned regardless of the generally established retirement age. Citizens who have lost their ability to work retain the right to apply for a pension, regardless of age when establishing a disability group.

If you have any questions, please contact the specialists of the Pension Fund of the KCHR by calling the "Hot Line": 8-800-600-02-91.

Share news

From January 1, 2019, a new basis for early retirement is provided for citizens who have a long work record. Women can use the right to retire 2 years earlier than the generally established deadlines if they have a seniority of 37 years and men - 42 years, but not earlier than reaching the age of 55 for women and 60 for men.

Since the retirement age will be raised in stages, in 2019, if you have a long service, you can become a pensioner ahead of schedule only six months ahead of schedule. The general retirement age in 2019 is respectively 55 years and 6 months for women and 60 years and 6 months for men.

For example: a man with a date of birth - 05/15/1959 has the right to retire at 60 years and 6 months, that is, 11/15/2019. However, if he has 42 years of experience, he can retire at 60 - that is, 05/15/2019.

However, if he has 42 years of experience, he can retire at 60 - that is, 05/15/2019.

If a citizen has worked out the above number of years of work experience in 2022, for example, it will be a woman born in 1966, then she has the right to retire at 56 years old, 2 years earlier than the generally established period.

What is included in the length of service for early retirement?

- For the appointment of an early pension due to long service, the periods of work that were performed on the territory of the Russian Federation and for which insurance premiums were paid to the Pension Fund, as well as periods of receiving benefits for compulsory social insurance during a period of temporary disability are taken into account. Non-insurance periods, such as: military service, parental leave, periods of receiving unemployment benefits are not included in the length of service.

Residents of St. Petersburg and the Leningrad Region can check the current experience in the Personal Account of a citizen on the PFR website or on the public services portal. Information about the experience can also be obtained from the client services of the PFR and the MFC.

Information about the experience can also be obtained from the client services of the PFR and the MFC.

If you think that any information is not taken into account or not taken into account in full, contact your employer to clarify the data and submit it to the Pension Fund.

Statistics:

As of May 1, 2019year on the above grounds, pensions were assigned to 162 citizens, of which 26 were men and 136 were women.

for information:

TECHIPS OF ACTION OF PERFORMANT OF PERFORMANCE

| Year of birth | Men | Release year for retirement with 42 years of service | |||

| Retirement age giving the right to an old-age pension | Entitlement to an insurance pension | Retirement age with 42 years of service | |||

| 1959 | 60 years 6 months | II half of 2019 H1 2020 | 60 | 2019 | |

| 1960 | 61 years 6 months | II half of 2021 H1 2022 | 60 | 2020 | |

| 1961 | 63 | 2024 | 61 | 2022 | |

| 1962 | 64 | 2026 | 62 | 2024 | |

| 1963 onwards | 65 | 2028 etc. | 63 | 2026 etc. | |

| Year of birth | Women | Release year for retirement with 37 years of service | |||

| Retirement age | Entitlement to an insurance pension | Retirement age with 37 years of service | |||

| 1964 | 55 years 6 months | II half of 2019 H1 2020 | 55 | 2019 | |

| 1965 | 56 years 6 months | II half of 2021 H1 2022 | 55 | 2020 | |

| 1966 | 58 | 2024 | 56 | 2022 | |

| 1967 | 59 | 2026 | 57 | 2024 | |

| 1968 onwards | 60 | 2028 etc. | 58 | 2026 etc. | |

02.27.2023

March 1 in St. Petersburg will be a comprehensive technical verification of the certificate of the population of the population

A short certificate of our district

until 2009 was called the municipal district No. 58. 9. 9.

Name changed to comply with law

Petersburg No. 109-27 dated April 15, 2009 "O

amendments to the Law of St. Petersburg "On

territorial structure of St. Petersburg" and separate

laws of St. Petersburg in the field of territorial

devices of St. Petersburg and local organizations

self-government in St. Petersburg.

Provision of services

Provision of services and assistance to its citizens -

priority area of local work

Administration of the Municipal District Vvedensky.