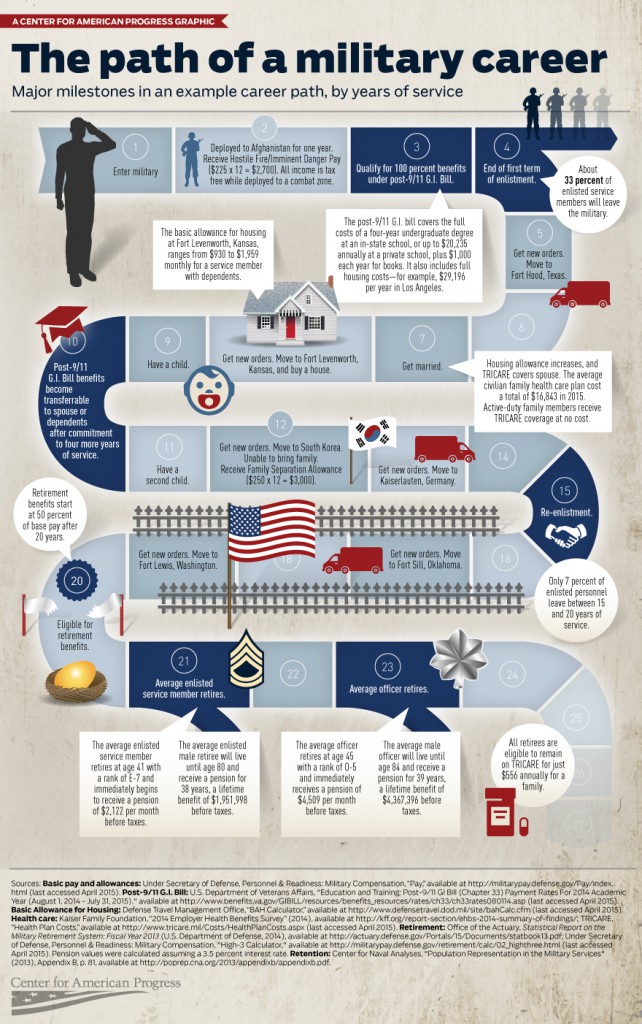

That’s a bold headline, especially if you a retired enlisted military member only bringing in a little over a thousand dollars a month in retirement pay. But it’s true. A military retirement is worth well over a million bucks. In some cases it is worth millions of dollars.

Before we get too deep into this, I want to define what I am talking about. I’m talking about two factors – the long term value in regard to how much you will receive in direct pension over the lifetime of your retirement benefits and the value of the retirement benefits including healthcare coverage, and other benefits. Combined, these benefits are easily worth over a million dollars, even if you don’t have the spending power of a million dollars right now.

Let’s look at an example of retirement pay for an average military career. Since military members are eligible for retirement benefits at 20 years, we will use a reasonable rank and service time for our examples.

It is reasonable to assume that the average enlisted member will be able to retire at 20 years having achieved the rank of E-7, and the average officer should be able to retire at 20 years at the rank of O-5. Of course there will be outliers based on when you served, your career field and other factors, but these ranks and service times should apply to the majority of careers (if anything I am aiming on the conservative side because many people choose to serve longer than the 20 year mark, earning an extra 2.5%-3.5% on their retirement pay per additional service year, depending on whether they take the high 3 retirement plan or the Redux retirement plan).

Track your TSP and other investments with Personal Capital’s free financial dashboard

As we mentioned, we will look at a military retiree with 20 years service at the ranks of E-7 for enlisted and O-5 for officers. The base pay for these ranks in 2009 is:

40

40Most retirees at 20 years will receive 50% of their base pay, which would equal the following amounts:

The next factor to consider is that military retirement pay will be there day in and day out. There are few places in the world that someone can receive a lifetime pension starting at or around age 40. Many military retirees will receive a monthly cash payment for over 40 years. When you add in cost of living adjustments and inflation adjustments, we’re talking about some serious cash!

Using the numbers above from a recently retired E-7 or O-5, we get the following lifetime payments (note: these military retirement pay numbers are not adjusted for inflation and do not include any COLA increases; this is not a planning tool, but for illustration purposes only. Your specific retirement benefits will vary based on your situation):

Your specific retirement benefits will vary based on your situation):

Even without COLA or other inflation adjustments, we can see that we are reaching some serious numbers. Each additional year you serve before you retire can add another 2.5% to your monthly and annual pay, and each higher pay grade you achieve can add hundreds, or even thousands of dollars per year. As previously mentioned, the numbers used in this article are meant to be a conservative estimate.

Visit PersonalCapital.com

OK, there is a minimal TriCare payment, but compared to what civilians pay, it is basically a non-issue. Benefits for retired military members are also guaranteed – they won’t drop you after you have required expensive procedures or for pre-existing conditions. Guaranteed medical coverage is a huge blessing in today’s American society. Here is a little more information about kinds of insurance available to civilians: comparing individual and group health insurance. Hopefully that will hep you better understand the value of military retiree medical benefits!

Benefits for retired military members are also guaranteed – they won’t drop you after you have required expensive procedures or for pre-existing conditions. Guaranteed medical coverage is a huge blessing in today’s American society. Here is a little more information about kinds of insurance available to civilians: comparing individual and group health insurance. Hopefully that will hep you better understand the value of military retiree medical benefits!

Military sponsored medical benefits are incredibly valuable, especially as you get older and when they cover your spouse. There are very few civilian plans that are similar to this. Most people spend several thousand dollars per year for basic medical coverage, and this doesn’t include out of pocket expenses for doctors visits, medical procedures, prescription medication and other associated costs. It would not be unreasonable to place a value of $10,000 per year on military retiree medical benefits, even for a healthy individual. Add a spouse to the benefits, guaranteed coverage, little to no out of pocket expenses for complex medical procedures, and other factors, and the medical benefits alone can be worth hundreds of thousands of dollars or more over the course of a lifetime (and in some instances, into the millions of dollars for people who receive complex medical care over a long term period).

Add a spouse to the benefits, guaranteed coverage, little to no out of pocket expenses for complex medical procedures, and other factors, and the medical benefits alone can be worth hundreds of thousands of dollars or more over the course of a lifetime (and in some instances, into the millions of dollars for people who receive complex medical care over a long term period).

I won’t even try to assign a value to these benefits because they don’t apply to all military retirees equally. Some people may practically live on base, visiting the base clubs, shopping at the exchanges, using the gyms, auto hobby shops, etc. and other people may not live near a base and may not be able to take advantage of any of these benefits. So this category falls in the “good deal if you can get it” benefit, but not a core part of the equation. But it is still worth mentioning because many retirees save a lot of money each year by shopping on base.

One challenge to the analysis is that the military pension includes a cost of living adjustment, so the amount of the income stream has to rise every year by the rate of inflation.

Another problem is that no one knows how long the pensioner will live, so it’s difficult to predict how long the pension will be paid out.

Finally, the calculated lump sum has to be invested in a safe and stable asset to make sure that it survives for decades. Unfortunately, the safe and stable assets have a very low yield, so it takes a larger lump sum to produce an income stream big enough to pay the pension.

The answer to these puzzles involves the mathematical process of “discounting”.

Accountants and actuaries devote entire careers to studying asset yields, human longevity, and other risks. They calculate the statistical probability that a certain lump sum will be able to pay a particular pension for the necessary number of years.

The good news for pension recipients is that the calculations are much more accurate when the analysis is simultaneously applied to hundreds of thousands of pensions as a group. Even better, the Department of Defense can rely on the number-crunching skills of another giant bureaucracy of inflation-adjusted payments: Social Security.

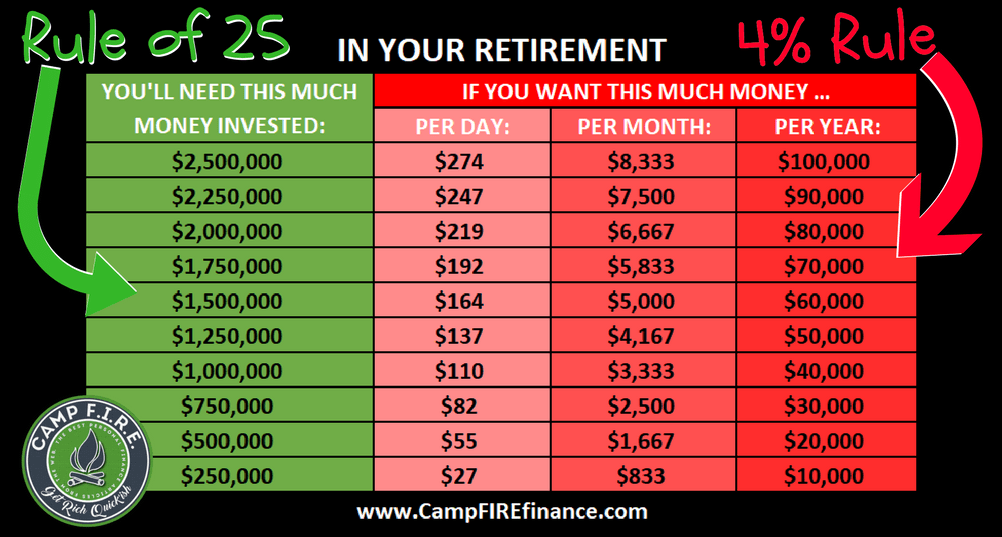

The mathematical details of discounting an inflation-adjusted annuity are well beyond the scope of this post. There’s not an easy formula to convert that $100/day pension to a precise lump sum. However, there are a few simpler estimates that are reasonably close to the more complicated methods.

The easiest estimate assumes that a military pension keeps up with inflation. This eliminates the more complicated factors of correcting future dollars for inflation. If a military pension keeps up with inflation then the pension’s value in today’s dollars stays constant. The lump-sum value of the pension is the total amount to be received during the rest of the veteran’s life:

A 38-year-old veteran receiving $3000/month with a COLA might reasonably look forward to 35 more years of life. The estimate of the present value of their pension would be

The estimate of the present value of their pension would be

The life-expectancy estimate ignores other discounting factors in favor of simplicity and speed. Its main advantage is that a veteran can quickly estimate a lump sum for their own personal expected lifespan. Veterans in good health with long-lived ancestors may decide that they have 40 or even 50 years of retirement, raising the current value of their pension.

Another quick estimate is to assume that the pension is the income stream from a lump sum of Treasury Inflation-Protected Securities (TIPS). TIPS are an extremely safe and stable asset with built-in inflation protection. The market for buying and selling TIPS is huge and liquid so their prices are fairly accurate.

One flaw of this estimate is that, unlike a military pension, when the pensioner dies there’s still a lump sum of TIPS generating a stream of income. Another drawback is that a TIPS’ maturity (now a maximum of 30 years) is usually less than the pensioner’s remaining life expectancy.

Another drawback is that a TIPS’ maturity (now a maximum of 30 years) is usually less than the pensioner’s remaining life expectancy.

The advantage of this estimate is simplicity and speed:

A January 2009 Treasury auction sold 20-year TIPS at an inflation-adjusted annual percentage yield of 2.5%. So for that $3000/month pension,

Another estimate of the lump-sum value of an inflation-adjusted pension is a commercial annuity. The annuity market is generally regarded as liquid because insurance companies compete to offer the “best” price without losing money. However, they still charge more than the actual value of the annuity to make their profit.

Insurance companies could be unable to make annuity payments or even go bankrupt and should be considered a riskier source of annuity payments than TIPS or other government bonds.

One of the “less risky” annuities comes from an agency sponsored by the federal government– the Thrift Savings Plan. TSP annuities are actually purchased from an insurance company and are not guaranteed by the federal government, but the insurance company is presumably charging a smaller fee (to sell a large volume of annuities) and the annuity’s cost would be closer to its value.

TSP annuities are priced each month and do not offer full protection against inflation. The advantage of estimating a pension’s lump-sum value from a TSP annuity is its lower price and the TSP website’s calculator. Assuming that the $3000/month pension is paid to a 38-year-old veteran and limited to 3% annual inflation:

$1.4 million is the price that a veteran would pay in the market to buy a TIPS portfolio or an annuity that would yield their inflation-adjusted pension of $3000/month for the rest of their life. Other research analyzes the theoretical cost of annuities and discounted values– only the cost and not its market price. (This includes a research paper on military pensions– the citation is in the book.)

Other research analyzes the theoretical cost of annuities and discounted values– only the cost and not its market price. (This includes a research paper on military pensions– the citation is in the book.)

These estimates range from about $1 million to $1.2 million. They’re only theoretical estimates. These annuities can’t actually be purchased like the assets of the other estimates, but they’re a more conservative estimate of the probabilities of longevity and other risk factors.

Let’s get back to the veteran who’s just finished 10 years of service and is wondering if it’s worth staying in the military for another decade. After an analysis of the pension’s present value, which sounds more compelling now: $100/day, or lifetime income of over $1 million?

Thousands of dollars coming in on a regular basis quickly add up over the years. Add in increases for inflation, essentially free health care, and other benefits and you can see how the value of a military retirement can quickly be worth millions of dollars over a lifetime.

I didn’t stay in long enough to qualify for military retirement benefits – I separated from the USAF with an Honorable discharge after 6.5 years of service. Part of me looks at the military retirement system with a bit of longing. It is a great system for those who qualify and I would love to be able to receive military retirement benefits for the rest of my life. However, separating from the military was the best move for me at the time and I have no regrets regarding my separation or my military service. I am proud to have served and the military is a large part of who I am today.

*disclaimer about this article: The calculations are for illustrative purposes only and do not reflect the exact retirement benefits you will receive. This is a simplified look at military retirement benefits and does not take many factors into consideration, including taxes, disability benefits, inflation, COLA, and other factors.

ABOUT R&A PAY

R&A Pay establishes, maintains and pays military retirees, and their eligible surviving spouses and other family members.

Who We Are, What We Do

Who to Contact? DFAS, the VA or the Military

How Long Does It Take?

Retiree Newsletter

Survivor SBP Newsletter

Find out the latest news and other helpful information.

Retiree payments will be made as scheduled on November 1, 2022. Annuitant payments will be made as scheduled on November 1, 2022.

The 2023 Cost of Living Adjustment (COLA) for military retirees and SBP annuitants is expected to be officially announced in November. We will post the information here when the information is available.

We have new, helpful guides to assist in navigating the use of the online tools available for retirees and SBP annuitants.

Click here to download the PDF guide for retirees

Click here to download the PDF guide for SBP annuitants

We have new helpful tips for you if you are new to Retired Pay: Quick links to the pay calendar, information about taxes and SBP, the VA Waiver, CRDP, CRSC, and more!

Right click HERE and choose save as to download your PDF today!

January 2023 marks the third and final phase of the SBP-DIC Offset Phased Elimination, in accordance with the National Defense Authorization Act for Fiscal Year 2020, which modified the law that requires an offset of Survivor Benefit Plan (SBP) payments for surviving spouses who are also entitled to Dependency and Indemnity Compensation (DIC) from the Department of Veterans Affairs (VA).

In the third and final phase that begins January 1, 2023, the SBP-DIC offset will be fully eliminated. That means spouses will begin to receive their full SBP monthly payments beginning with their January 2023 entitlement, which will be paid on February 1, 2023.

See our full range of FAQs on the SBP-DIC News webpage.

*Note: the change in the law does NOT affect the amount of DIC you receive from the VA. You should continue to receive your normal DIC amount from the VA.*

The National Defense Authorization Act for Fiscal Year 2020 directed that as of January 1, 2023, the Optional Annuity for Dependent Children will be eliminated and the SBP annuity payment must revert to the surviving spouse (if the spouse submits documentation and is eligible).

If you are the surviving spouse of an Active Duty/Line of Duty member who requested to have the Survivor Benefit Plan (SBP) annuity paid directly to an eligible dependent child or children and you have NOT submitted a Spouse Eligibility Packet, we need your information as soon as possible. Please download, fill out and submit the eligibility packet from our special focus webpage as soon as possible: https://www.dfas.mil/sbp2023childoptrev

If you are the surviving child (or the parent or guardian of a surviving child) of an Active Duty/Line of Duty member whose surviving spouse requested to have the Survivor Benefit Plan (SBP) annuity paid directly to you and you are currently receiving the monthly SBP annuity payment, we have started sending informational letters about what will happen in 2023. Please see our special focus webpage for examples of the letters and more information: https://www.dfas.mil/sbp2023childoptrev

Please check our special focus webpage for news and information regarding this change and transition. We will post updates on this webpage: https://www.dfas.mil/sbp2023childoptrev

We will post updates on this webpage: https://www.dfas.mil/sbp2023childoptrev

The 216-522-5955 local phone number is no longer available to use (after July 1, 2022).

The DSN number to reach Retired & Annuitant Pay Customer Service also changed. The new DSN number is 699-0551.

This change does NOT affect the toll-free number (1-800-321-1080). The toll-free number remains the same.

Military retired pay is paid for many different reasons under many different laws. There are differences in the types of pay a military retiree might receive and the tax laws that apply to them. Whether a portion or all of an individual’s military retired pay is subject to federal income taxes depends on his/her individual circumstances.

A military retiree can either use myPay or send an IRS Form W-4 to alter the amount DFAS withholds for federal income taxes from their military retired pay.

An individual’s choice to have no withholding for federal taxes does not impact whether the individual’s military retired pay is actually subject to federal income taxes. Ultimately, the IRS will determine the amount of taxes owed on the military retired pay.

Please note: the IRS requires any individual claiming exemption from federal withholding to provide a new Form W-4 at the beginning of each tax year certifying their exemption from withholding.

Please see our webpage regarding taxation of retired pay :https://www.dfas.mil/RetiredMilitary/manage/taxes/isittaxable/

DFAS cannot provide tax advice. Please consult a tax professional or the IRS.

We are working to simplify the process of verifying continuing eligibility for retirees. The newest change reduces the number of retirees who need to submit a Report of Existence (ROE). Now, the only retirees who need to submit an ROE are those who receive a paper check to a foreign address. Previously, the legal representatives for all incapacitated retirees were required to submit an ROE twice each year.

The newest change reduces the number of retirees who need to submit a Report of Existence (ROE). Now, the only retirees who need to submit an ROE are those who receive a paper check to a foreign address. Previously, the legal representatives for all incapacitated retirees were required to submit an ROE twice each year.

If you’re retired from the Guard or Reserve but not yet at the age to receive retired pay, we have important news for you. Gray Area Retirees now have a new way to stay connected and informed between the time they stop drilling and when they receive retired pay. It’s a new kind of myPay account that helps you keep your contact information current so that you can stay on top of your future retired pay. Click here for the Retiree Newsletter article or click here to find out how to log on.

We have helpful tools and info for you: a Form Wizard to help you fill out the DD 2788 form easily and correctly, a special How-To Checklist, and an online upload tool on DFAS. mil.

mil.

Check them out on the School Certifications webpage.

We are working to simplify the process of verifying continuing eligibility for Survivor Benefit Plan annuitants. The newest change reduces the number of annuitants who need to submit a Report of Existence (ROE). Now, the only annuitants who need to submit an ROE are those who receive a paper check to a foreign address. Previously, the legal representatives for all incapacitated annuitants were required to submit an ROE twice each year.

There is a new overview and a downloadable PDF fact sheet of the eligibility verification requirements for annuitants on our “Manage Your SBP Annuity” webpage. We hope this information will help our customers better understand their role in keeping their annuity accounts current.

Retired & Annuitant Pay is rolling out new, helpful Status Notifications to keep you in the loop as forms or documents you submit move through the retired pay or annuitant pay processing cycles. The Status Notifications will be sent primarily via SmartDoc email, so make sure you have an up-to-date email in your myPay profile so you can receive them.

The Status Notifications will be sent primarily via SmartDoc email, so make sure you have an up-to-date email in your myPay profile so you can receive them.

Please contact your TRICARE regional contract. DFAS cannot set up these allotments. They must be set up by TRICARE through the regional contractors. Please note: only Retirees can set up allotments from their pay. Allotments cannot be paid from SBP or SSIA annuity pay.

The information to set up allotments through the regional contractors is as follows:

TRICARE East

Humana Military

1-800-444-5445

Allotments can be set up online or via phone. For more information on setting up allotments, visit https://www.humanamilitary.com/selectfees or call 1-800-444-5445.

TRICARE West

Health Net

1-844-866-9378

Allotments can be setup online, via telephone self-service, or by paper application. For more instructions on setting up allotments, visit https://www.hnfs.com/content/hnfs/home/tw/bene/enroll/allotment.html or call 1-844-866-9378.

For more instructions on setting up allotments, visit https://www.hnfs.com/content/hnfs/home/tw/bene/enroll/allotment.html or call 1-844-866-9378.

TRICARE Overseas

International SOS

For Country Specific Toll-Free Numbers, visit: http://www.tricare-overseas.com/contact-us

Please contact your country-specific number via phone for more information about setting up your allotment.

We have new tools and information to assist you with the SF 1174 for claiming the retiree’s Arrears of Pay. We can now deposit an Arrears of Pay (AOP) payment directly to an eligible claimant’s bank account instead of mailing a check. And we have an online upload option that will provide you with status notifications. Please see the How to Claim Arrears of Pay Using the 1174 page for details.

We have new tools and information to assist you with the DD Form 2656-7 for starting a Survivor Benefit Plan Annuity. We have a Form Wizard to help fill out the form correctly and easily. And we have an online upload option that will provide you with status notifications. Please see the Start an SBP Annuity page for details.

We have a Form Wizard to help fill out the form correctly and easily. And we have an online upload option that will provide you with status notifications. Please see the Start an SBP Annuity page for details.

Please see our new webpage for current typical processing time frames: How Long Does It Take?

As part of our commitment to continually improving our customer service, R&A Pay is expanding the use of emailed SmartDocs as a way to communicate about changes to your account and actions that may be needed. Email notifications will speed up the time it takes to notify you about your account. If you don’t yet have an email address in myPay, please add one now so you can receive these email notifications.

A treasury mandate requires us to pay our customers electronically. Most military retirees and annuitants getting paper checks need to set up direct deposit. Start direct deposit now.

Most military retirees and annuitants getting paper checks need to set up direct deposit. Start direct deposit now.

Direct Express® Debit Card Program provides members who do not have a bank account an alternative to payment by EFT.

Pay Verification / Proof of Income

Survivor Benefit Plan Information

Get My 1099R

Correct My 1099R

Change My Arrears of Pay Beneficiary

Start or Change Direct Deposit

Change My Address

Manage My Allotments

Start International Direct Deposit

Report a Retiree's Death

Report an SBP Annuitant's Death

The most convenient way to manage your retirement account is through myPay, our online account management system.

myPay Login Instructions:

If you've never logged into myPay

If you forgot your login ID

If you forgot your password

Page updated Oct 21 2022

According to the law, a military man who has retired receives a monthly allowance from the state.

Svetlana Fateeva

dealt with military pensions

Author profile

Military people retire not by age, but by seniority or disability, if they received it in the service. And their relatives - in connection with the loss of a breadwinner. The pension is assigned to military personnel who served in the internal affairs bodies, employees of the Russian Guard, the Ministry of Emergency Situations, the Ministry of Internal Affairs, the FSB, the FSIN. They can receive it when they leave military service. If a military man left the service and got a job as a civilian, then the right to an insurance pension will also appear.

The amount of the pension depends on the position and rank of the military, length of service and allowances. In the article I will tell you how to apply for a military pension, how it is calculated and what are the allowances.

Military pensions are described by laws that contain more than a hundred pages. In this article, I gave a constructor: what payments make up a military pension. For convenience, there are links to articles of the law in the margins, so if you want to know in detail, you can go there and read. Each particular case of calculating a pension has its own subtleties that will affect its size. Therefore, in order to accurately calculate your pension, it is better to consult with the pension authority of the law enforcement agency in which you served.

In this article, I gave a constructor: what payments make up a military pension. For convenience, there are links to articles of the law in the margins, so if you want to know in detail, you can go there and read. Each particular case of calculating a pension has its own subtleties that will affect its size. Therefore, in order to accurately calculate your pension, it is better to consult with the pension authority of the law enforcement agency in which you served.

When a soldier reaches a certain level of service, he is awarded a service pension.

Conditions for granting a pension. By law, a seniority pension is due to the military if:

Art. 13 of the law on pensions for persons who have completed military service

13 of the law on pensions for persons who have completed military service

According to military experience. Military experience, for example, includes:

st. 18 of the law on pensions for persons who have completed military service

Officers and military commanders are credited with up to 5 years of study before entering the service. One year of study will be equal to 6 months of service. For example, if a military man studied for 5 years, he will be credited with 2.5 years of service.

One year of study will be equal to 6 months of service. For example, if a military man studied for 5 years, he will be credited with 2.5 years of service.

Service in special conditions is included in the length of service on a preferential basis. This means that periods of service will be included in the length of service in longer periods than the calendar period. For example, for service in countries that fought hostilities, a month is counted as two.

Decree of the Government of the Russian Federation of September 22, 1993 No. 941 - on preferential calculation

Special conditions also include, for example, service in the regions of the Far North, in positions associated with increased danger to life and health.

When the pension will be granted. A military man submits documents for a seniority pension - and they are checked. The pension will be assigned within 10 days from the day of dismissal - but not earlier than the day before which the monetary allowance was paid upon dismissal. If you delay in applying for a pension, it will be assigned retroactively from the day when the right to it arose. You can receive payments up to 12 months before the day of application.

If you delay in applying for a pension, it will be assigned retroactively from the day when the right to it arose. You can receive payments up to 12 months before the day of application.

Art. 53 of the law on pensions for persons who have completed military service

The amount of pension for service depends on several factors:

For military personnel with 20 years of service, the pension will be 50% of the monetary allowance. For each next year of service, 3% will be added, but in total the percentage of monetary allowance cannot be more than 85%.

Art. 14 of the law on pensions for persons who have completed military service

For example, a military man has served 20 years. His monetary allowance is 42,000 R. The pension will be set at 50% of the monetary allowance - 21,000 R, but due to the reduction factor on hand, the military will receive less - I will talk about this in detail in another section. For each next year, 3% is added: for 21 years of service - 53%, for 22 years - 56%, etc., but not more than 85% of the allowance.

For each next year, 3% is added: for 21 years of service - 53%, for 22 years - 56%, etc., but not more than 85% of the allowance.

For military personnel with 12.5 years of service with a total length of service of 25 years, the pension will also be 50% of the monetary allowance, and only 1% will be added for each subsequent year of service. Theoretically, the military with such length of service can receive 100% of the monetary allowance, but only for 75 years of service.

The monthly payment, , which is indexed annually, is entitled to participants and disabled veterans of the Great Patriotic War and combat veterans. The maximum payment amount is 3088 R per month in addition to the pension. In 2022, taking into account indexation, the amount of payment for participants in the Great Patriotic War is 4746.29 R, for disabled veterans of the Great Patriotic War - 6328.41 R, for combat veterans - 3481.85 R.

Art. 23.1 of the Federal Law "On Veterans"

Increased military pension receive disabled people. How much it has increased is calculated as a percentage of the social pension. The amount of the social pension depends on the category of disabled citizens.

How much it has increased is calculated as a percentage of the social pension. The amount of the social pension depends on the category of disabled citizens.

Art. 16 of the law on pensions for persons who have completed military service

p. 1, art. 18 of the Federal Law "On state pension provision in the Russian Federation"

For example, a disabled person of the first group is entitled to a social pension of 11,212.36 R. If he was injured in military service, the pension will be increased three times:

11,212 R × 300% \u003d 33 636 R

| Disability group | For military personnel injured on duty | For military personnel with a disease, industrial injury, as well as for participants in the Great Patriotic War | For those awarded with the badge "Inhabitant of besieged Leningrad" |

|---|---|---|---|

| First | 300% | 250% | 200% |

| Second | 250% | 200% | 150% |

| Third | 175% | 150% | 100% |

The first disability group

for military injuries in the service of

300%

for the military with illness, labor injury, as well as for participants of the Second World War

250%

for the awarded the sign “Resident of the Blockade Leningrad City Leningrad »

200%

Second disability group

For the military who injured in the service of

250%

for the military with illness, labor injury, as well as for the participants of the Second World War

200%

for a resident of the Blockade Leningrad sign

9000,150%The third group of disability

For the military who were injured in the service

175%

0002 For those awarded with the sign "Inhabitant of besieged Leningrad"

100%

Disability pension is awarded regardless of the length of service. It is required if the military received a disability during the service or within three months after the dismissal. Disability must be the result of an illness or injury that the military received in the service.

It is required if the military received a disability during the service or within three months after the dismissal. Disability must be the result of an illness or injury that the military received in the service.

p. 2 art. 8 of the Federal Law "On State Pension Provision in the Russian Federation"

Disability is established by a medical and social examination or a military medical commission of the military district where the service takes place.

The amount of the pension depends on the disability group and the reasons for the disability. For conscripts, it is calculated as a percentage of the social pension.

Art. 15 Federal Law "On state pension provision in the Russian Federation"

| Disability group | Amount of pension due to military injury | Amount of pension due to illness received during service |

|---|---|---|

| First | 300% | 250% |

| Second | 250% | 200% |

| Third | 175% | 150% |

The first disability group

Due to the military injury

300%

Pension size due to the disease received during the service of

250% 9000%

The second disability group 9000 9000 9000 due to war injury

250%

The size of the pension due to the disease obtained during the service of

200%

Third disability group

Pension size due to military injury

175%

Pension size due received during service

150%

For example, for disabled people of the second group, the social pension is 5606. 15 R. For military personnel with a disability of the second group received due to a military injury, the pension will be calculated as follows:

15 R. For military personnel with a disability of the second group received due to a military injury, the pension will be calculated as follows:

5606 Р × 250% = 14 015 Р

For officers, ensigns, midshipmen and contractors, employees of law enforcement agencies, the disability pension is calculated as a percentage of the monetary allowance.

Art. 22 laws on pensions for persons who have completed military service

| Disability group | Amount of pension due to military injury | Amount of pension due to illness received during service |

|---|---|---|

| First | 85% | 75% |

| Second | 85% | 75% |

| Third | 50% | 40% |

The first disability group

The size of the pension due to military trauma

85%

Pension size due to the disease received during the service of

75%

The second disability group

Pension size due to military trauma

85%

Pension size due to the disease obtained during the service

75%

Third disability group

Pension size due to military trauma

9000 50 50 %The amount of the pension due to an illness received during service

40%

For example, a contractor receives a monetary allowance of 25,000 R. If he receives a disability of the second group due to a military injury, his disability pension will be calculated as follows:

If he receives a disability of the second group due to a military injury, his disability pension will be calculated as follows:

25,000 R × 85% = 21,250 R

Disability is established for a certain period, which is indicated in the certificate of the medical and social examination. When the deadline has passed, the military must undergo a re-examination to confirm the disability.

If the military misses the deadline, the payment of the disability pension may be suspended. If this happened for a good reason, for example, if the state of health worsened, then after re-examination, the pensioner will receive payments for the entire overdue period. If there was no good reason, the pension will continue to be paid when the pensioner confirms the disability.

Re-examination is not carried out if disability is established indefinitely, and also upon reaching 65 years for men, 60 years for women.

It happens that the state of health has changed. Then, at the personal request of the disabled person, his legal representative or in the medical direction, a re-examination is carried out. If the disability group is changed, the amount of the pension also changes.

If the disability group is changed, the amount of the pension also changes.

If a serviceman dies or goes missing, each disabled member of his family is assigned a survivor's pension. In this case, the pension is due:

st. 29 of the law on pensions for persons who have completed military service

The loss of a breadwinner is considered:

st. 28 of the law on pensions for persons who have completed military service

The amount of the pension depends on the cause of death of the breadwinner. If the military served under a contract, then a pension is given to each disabled family member as a percentage of the breadwinner's allowance. 50% of the military allowance will be assigned to the following categories of citizens:

st. 36 of the law on pensions for persons who have completed military service

If a soldier dies due to an illness received during the period of service, his family will be paid 40% of the military allowance.

If the military served on conscription, the pension will be calculated as a percentage of the social pension. It will be paid to each disabled family member in an amount that depends on the cause of death of the conscript:

item 4 of Art. 15 of the Federal Law "On state pension provision in the Russian Federation"

If family members lose their right to a pension, then payments will be reduced or stopped. For example, if the children of the deceased study full-time at a university, they are entitled to a pension up to 23 years. They will stop receiving their pension the next month after they turn 23.

If a military man, after being discharged from service, works as a civilian, he has the right to a second pension - an insurance one. At the same time, the work must be official - if the employer does not deduct pension contributions, there will be no right to an insurance pension.

About the second pension for military personnel

You can check how many contributions were paid to the Pension Fund of the Russian Federation in your personal account in the section "On the formed pension rights" or in the pension fund or MFC - you will need a passport and SNILS. You can register in the compulsory pension insurance system at the territorial pension fund or the MFC. You need to come there with a passport and fill out a questionnaire. You can also log in to the PFR website through the public services website if you are already registered there.

/guide/skolko-pensiya/

How to calculate the old-age pension

Click on the “Login” button in the upper right part of the screen After you are asked to log in through the public services website When you log in to public services, you will be asked to check whether your profile is filled out correctly . Change the details if required To receive a military pension and an insurance pension at the same time, you must meet the following requirements.

Age. Reaching the age of 61.5 years for men and 56.5 years for women, taking into account the length of service — for example, if a pensioner worked in the Far North or in difficult working conditions. Age is determined taking into account the transition period.

In Russia, there is a gradual increase in the retirement age. A transitional period has been introduced for these changes, which will be 10 years and end in 2028. As a result, the retirement age will be raised by 5 years and set at 60 for women and 65 for men. In the first half of 2022, the retirement age for women is 56.5 years, for men - 61.5 years. In the second half of 2022, only those who received this right earlier, but did not use it, will retire.

Annexes 5 and 6 to Law No. 350-FZ

Raising the retirement age

Civil service. The length of service for the insurance pension does not include periods of service in the army or work that are taken into account when calculating the military pension. In 2022, the minimum work experience is 13 years. It increases by 1 year each year until it reaches 15 years in 2024.

In 2022, the minimum work experience is 13 years. It increases by 1 year each year until it reaches 15 years in 2024.

Number of pension points. The minimum score in 2022 is 23.4. Their number will increase annually until 2025. By 2025, the minimum number of points will be 30. To check your points, you can contact the territorial pension fund with a passport and SNILS or in your personal account on the PFR website.

When you enter the compulsory pension insurance system, on the main page you can see how many pension points you haveThe formula for calculating the second pension is as follows:

Accumulated pension points × Value of one point

Calculate the amount of the second pension a point costs 107.36 R, the amount is indexed annually.

Usually a fixed payment is added to the insurance pension, but it is not paid to military pensioners.

What to do? 30.09.19

How to buy more pension points?

There are allowances for seniority and disability pensions. They are calculated as a percentage of the social pension.

They are calculated as a percentage of the social pension.

Art. 17 of the law on pensions for persons who have completed military service

When calculating a pension for the military, various payments are taken into account: allowances, increases and increases. These three terms are often confused, but they mean different things:

Do not confuse.

The allowance is due:

If one is disabled - 32%, two - 64%, three or more - 100%.

If one is disabled - 32%, two - 64%, three or more - 100%. For example, a disabled person of the first group will receive an allowance of 11,212 R - this is 100% of the social pension for this category.

Clause 2.1 Art. 18 Federal Law "On state pension provision in the Russian Federation"

There are other allowances: for long service, work with the state secret service, service in special conditions, etc. If a military man receives other income than a military pension, then allowances for dependents and disability are not paid.

Art. 2 of the Federal Law "On State Pensions in the Russian Federation"

Military pensions are increased for services to the country. For Heroes of the Soviet Union and the Russian Federation, holders of the Order of Glory of three degrees, the pension is increased by 100%, for Heroes of Labor - by 50%. The pension is increased by a multiple of the number of awards: for example, twice the Hero of the Russian Federation receives an additional 200% to the pension.

The pension is increased by a multiple of the number of awards: for example, twice the Hero of the Russian Federation receives an additional 200% to the pension.

Art. 45 of the law on pensions for persons who have completed military service

Champions of the Olympic, Paralympic and Deaflympics receive 50% of the pension. For awards with orders of Labor Glory of three degrees or "For Service to the Motherland in the Armed Forces of the USSR" - 15%.

The Deaflympics are games for people with hearing impairments

Social pension increases are received by:

All of them receive an increase of 32% in relation to the social pension. Those who served or worked during the Second World War for at least 6 months, as well as those who were unreasonably convicted and rehabilitated, receive an increase of 16%.

To calculate a military pension, you need to calculate the military allowance. To do this, you need to add salaries by position and rank with other payments. Then the allowance is multiplied by the reduction factor, the length of service and the district coefficient.

Law No. 460-FZ of December 11, 2018

After the pension is granted, the coefficient is increased by 2% annually until it reaches 100%. The state reserved the right to increase it by more than 2% if the inflation rate is high.

For WWII veterans, the reduction coefficient has been canceled since May 2019 - when calculating the pension for them, 100% of the monetary allowance is taken into account.

Monetary allowance consists of several parts:

st. 2 of the Federal Law on the monetary allowance of military personnel

Salaries by position

Salaries by rank

District coefficients. In some districts, coefficients for monetary allowance have been established. They are used if a pensioner lives in climatic, ecological and natural conditions that require additional costs - for example, in the Far North.

Amounts of district coefficients

A pension based on the district coefficient is received by military pensioners who:

st. 48 of the law on pensions for persons who have completed military service

The maximum value of the coefficient is 1.5. For example, in the Chukotka Autonomous Okrug, the coefficient is 2, but due to restrictions, it will be reduced to 1.5.

The length of service is calculated as follows: 50% is given for the first 20 years of service, and then 3% is added for each subsequent year. For example, after 21 years of service, the length of service will be 53%, after 22 years - 56%, etc.

As a result, the following formula is obtained:

(Position salary + Military rank salary + Other payments) × Reducing factor × Length of service × Regional coefficient = Military pension

An example of calculating pension for a lieutenant colonel in the position of battalion commander with a length of service of 22 years. By military rank, a lieutenant colonel is entitled to a salary of 12,480 R. He has the position of a battalion commander - for a position of 18th category, a salary of 24960 R. For 22 years of service, the lieutenant colonel will receive an allowance of 30% of the amount of salaries by position and rank:

By military rank, a lieutenant colonel is entitled to a salary of 12,480 R. He has the position of a battalion commander - for a position of 18th category, a salary of 24960 R. For 22 years of service, the lieutenant colonel will receive an allowance of 30% of the amount of salaries by position and rank:

(24 960 + 12 480) × 30% = 11 232 R

This is what pension our lieutenant colonel will receive from October 1, 2019 - with a decreasing coefficient of 73.68%:

(24,960 R + 12,480 R + 11,232 R) × 73.68% × 56% × 1 = 20,082 R

To receive a pension according to the length of service, , you need to submit documents to the pension authority of the law enforcement agency in which the military served: the Ministry of Defense, the Ministry of Internal Affairs, the Federal Penitentiary Service or the FSB. Documents can be submitted in person or sent by mail. You will need:

The application for the appointment of a pension

Order of the Ministry of Defense dated 05/23/1999 No. 225

Sample of the calculation of length of service

for a disability pension to this list will be added:

For the survivor's pension , the following will be added to the list:

Together with the application, documents are submitted to increase payments and allowances - for example, documents confirming the special conditions of military service.

To assign a second pension , an application is submitted to the territorial pension fund. Here's what to bring there:

Documents for a second pension

Sample application for granting a pensionPension departments in state structures are responsible for calculating and paying military pensions - for example, the pension department in the military registration and enlistment office at the place of registration. The payment of a pension does not depend on other income.

Art. 56 of the law on pension provision for persons who have completed military service - the procedure and terms for paying a military pension

A military pension is received for the current month to an account with Sberbank or at a convenient branch of the Russian Post in person or by proxy. Payment terms are determined by agreement between the pension authority, the bank and the post office.

Military pension is withheld on the basis of court decisions. No more than 50% of the pension can be withheld.

Art. 62 of the law on pensions for persons who have completed military service

62 of the law on pensions for persons who have completed military service

Most often, alimony is withheld. They are kept from regular payments: from military and insurance pensions, from salaries and from business income. For one child - a quarter of the income, for two - a third, for three or more - half. At the same time, some payments are not taken into account when collecting alimony - for example, payments in connection with a military injury.

Federal Law "On Enforcement Proceedings"

The state annually indexes the cost of one point - in 2022, a point costs 107.36 R. In 2022, pensions for working pensioners will not be indexed. An indexed pension will be accrued to a pensioner only after dismissal.

From March 1, 2022, military pensions were indexed by 8.6% and recalculated from January 1, 2022.

Law No. 460-FZ dated December 11, 2018

And from October 1, 2022, the reduction coefficient will increase to 77. 41% of the monetary allowance.

41% of the monetary allowance.

Government Decree No. 1466 of December 1, 2018

Military pensions are paid to the card of the Mir national payment system.

Lack of cash flow in a bank account cannot be a reason for stopping the payment of a pension. The Constitutional Court of Russia came to this conclusion after examining the case of military pensioner Pavel Ponedelkov. The provisions of the Federal Law "On Labor Pensions in the Russian Federation" are recognized as not contradicting the Constitution of the Russian Federation, since they do not imply the suspension of payments even if transactions on an account or deposit are not made for six months in a row.

Ponedelkov's story is a clear illustration of how a man almost derailed his own life, but found the strength to rectify the situation. From 1982 to 1997, he served at the Baikonur Cosmodrome, then he was transferred to the reserve with a seniority pension, which he began to receive on a bank card. Then, as follows from the case file, the life of a retired military man "became a losing streak": the man got drunk and lost his passport, so from 2006 to 2016 he did not apply for a pension. And when he decided to return to a normal life, he restored his passport and wanted to buy housing with the money saved over 10 years - he was once evicted from a departmental apartment. But the Law "On pensions for persons who have served in the military, served in the internal affairs bodies, the State Fire Service, bodies for controlling the circulation of narcotic drugs and psychotropic substances, institutions and bodies of the penitentiary system, the troops of the National Guard of the Russian Federation, the enforcement agencies" has become an obstacle. performance of the Russian Federation, and their families". Article 58 states that "the amount of a pension accrued to a pensioner from among the persons specified in article 1 of this law, and members of their families, but not claimed by him in a timely manner, is paid for the past time, but not more than three years before applying for its receipt ". The military courts referred to this provision, justifying the refusal to pay the entire amount of the shortfall.

And when he decided to return to a normal life, he restored his passport and wanted to buy housing with the money saved over 10 years - he was once evicted from a departmental apartment. But the Law "On pensions for persons who have served in the military, served in the internal affairs bodies, the State Fire Service, bodies for controlling the circulation of narcotic drugs and psychotropic substances, institutions and bodies of the penitentiary system, the troops of the National Guard of the Russian Federation, the enforcement agencies" has become an obstacle. performance of the Russian Federation, and their families". Article 58 states that "the amount of a pension accrued to a pensioner from among the persons specified in article 1 of this law, and members of their families, but not claimed by him in a timely manner, is paid for the past time, but not more than three years before applying for its receipt ". The military courts referred to this provision, justifying the refusal to pay the entire amount of the shortfall.

- In the applicant's case, the courts applied the challenged norm in such a way that they recognized the applicant's failure to withdraw the pension transferred to his personal bank account as non-receipt of it, - the lawyers pointed out, - which violates common sense and a number of constitutional guarantees. The challenged norms, which allow the suspension and then termination of payments only on the grounds that a pensioner has been accumulating funds, violate the right to pension provision and the right to property.

When the pension is credited to the pensioner's personal bank account, it is already being received

The Constitutional Court of the Russian Federation was first of all reminded that Russia is a welfare state, and "any pensions assigned in connection with labor or other socially useful activities are earned, deserved by citizens by previous work, service, and the fulfillment of certain duties that are significant for society." Accordingly, pensions must be paid to citizens on time and in full, and in case of violation of the right to receive a pension, it must be restored in full.