Adding an ATV or four-wheeler to your vehicle collection is a surefire way to get the most fun out of your free time in the summer or on weekends.

And if you've always wanted an off-roader but haven't felt that you could afford it, we have good news!

Financing your new ATV is a quick way to get you on the road, and because it's similar to financing cars or trucks, you're probably already more familiar with the process than you might think. Below, you'll find out everything you need to know about how to finance an ATV, from ATV loan rates to typical ATV financing terms and more.

At the Credit Union of Southern California (CU SoCal), we’ve provided low-interest loans to Southern Californians for over sixty years, and even if your credit history isn’t perfect, we can still help you buy the ATV or four-wheelr of your dreams.

Give us a call today at 866.287.6225 for a no-obligation consultation and get all the answers you need.

Get Started on Your ATV Loan!

Like loans you may have taken out for your education, your car, or your home, recreational vehicle loans work in much the same way.

Essentially, a financial lending institution will finance your ATV purchase, which you will pay back over time with interest. Because an ATV or four-wheeler is not considered a necessity, you might find the terms of your loan to differ slightly from auto loans you may have used in the past.

How much an ATV or four-wheeler loan will cost you, in the long run, will be determined by a few things:

e., how long you will be paying off the loan)

e., how long you will be paying off the loan)Because there are a few factors to consider, it's wise to shop around and evaluate your options when looking for 4-wheeler financing. Remember, just because an offer has a low interest rate doesn't mean it will be the best offer overall. You should also consider the length of the loan, known as the loan term, and your desired monthly payments.

At CU SoCal, we pride ourselves on offering our Members the best possible terms and interest rates. To ensure there are no unwanted surprises, check out our loan calculator that will help you figure out the ideal terms for your desired loan. And don't forget – if you need hands-on assistance, you can always call CU SoCal for an obligation-free consultation.

If you're wondering how to finance an ATV, you might already know what you're looking for. But if you're not quite at the point that you've chosen your perfect ATV, you might have a few questions about which is the best vehicle for you. A typical ATV, short for All-Terrain Vehicle, can also be referred to as a four-wheeler or quad. It is designed for only a single rider.

A typical ATV, short for All-Terrain Vehicle, can also be referred to as a four-wheeler or quad. It is designed for only a single rider.

Conversely, a UTV, or Utility Task Vehicle, is often larger and provides space for two people riding next to each other, which gives it the alternative name of a "side by side" or SXS.

At CU SoCal, we know how important it is for our Members to get the best financing assistance possible.

And for those wondering just how do ATV loans work, we have compiled a step-by-step financing guide to help you get offroad on four wheels. We'll discuss everything you need to know about how to finance an ATV, ATV loan rates, preapproval, and more.

Before even beginning to shop for a four-wheeler, you should check your credit score first. Knowing your credit score will help you determine if you're ready to go ahead and start shopping or if you need to take some time to improve your score.

If you have excellent credit, you're all set and can proceed to step two! However, if you aren't in the best financial shape, there are ways to improve your credit score so that you can qualify for a loan with better terms.

Additionally, CU SoCal’s Credit Builder Loan can help you get back on track if you need further assistance.

Once you’re happy with your credit score, you can start creating your budget. To begin, you'll have a few factors to consider:

When you're creating a budget to see how much you can borrow to purchase your quad or ATV, make sure you consider the total cost of ownership. In other words, don't forget to account for insurance, fuel, and accessories when creating your budget.

In other words, don't forget to account for insurance, fuel, and accessories when creating your budget.

Now that you know what your budget is looking like, you should start saving for a down payment.

The typical cost of an ATV is between $5,000 and $15,000, and the regular down payment is usually around 10-20%. Depending on the price of your vehicle, you're most likely looking at down payment between $500 and $3,000.

Now for the fun part – finding your perfect ATV, four-wheeler, quad, or side-by-side!

If you aren't sure what exactly you're looking for, it's time to do some online research. Several websites are dedicated to reviewing ATVs and other recreational vehicles, so a quick Google search should give you all the information you need to compare different makes and models.

When comparison shopping, you'll want to take into account availability, specs, and price. Taking a look at dealerships near you will give you a good idea of what's available in your area and the price range for those specific vehicles. Many dealerships have knowledgeable staff that can help you make an educated decision.

After choosing your ATV, it's time to start shopping different lenders. There are several options that you'll come across, but the primary lenders are banks, dealerships, online lenders, and credit unions like CU SoCal. We'll talk more about each of these in more detail later on.

When shopping for lenders, you should compare their offers regarding loan terms and interest rates. You should also check out whether there are any fees or penalties that could affect you.

With all of your well-researched information in hand, including your budget, the item cost, and your chosen lender, it's time to get preapproved.

To do this, your lending institution will have a look at your financial situation, including your credit report and verifications of debt and income. Then, they'll decide how much money they are willing to loan you under those circumstances, along with their terms and interest.

If you've followed the previous steps, your credit score should be in good shape, and you should know exactly how much you'll need for your ATV financing. Thorough preparation will likely lead to a successful loan, so you're almost done!

With your preapproval, you will likely be given the terms under which the loan will be provided, including interest rates and terms. Typical ATV financing terms are between three and six years with a fixed annual percentage rate (APR).

With CU SoCal's loan calculator, you can modify the loan amount, down payment, monthly payment, interest rate, and term so you can calculate your monthly payments on your new ATV.

In step four, we talked about comparison shopping for ATVs, quads, four-wheelers, and UTVs based on their specs, reviews, and prices. Now it's time to take a more personal look at the vehicle to see if it's suited for your particular needs. While many ATVs are used recreationally for fun on the weekends, heftier UTVs can haul small trailers if needed for work. Other things to think about are whether you'll be riding solo most of the time, if you're looking to get into racing, or if you'll be taking it out onto unusual terrain, like sand dunes.

For the final step, all you have to do is make the purchase! Now is the time that you will see the ownership cost of the item, including insurance, safety gear, and any applicable licensing. However, since you've budgeted and considered your long-term financial situation, you will already be prepared for this.

As with simple auto loans, there are various ways to get a loan for your ATV purchase. ATV loan rates will vary from institution to institution, so it is wise to do some research if you want the best 4-wheeler financing. Here are the most common places to get ATV loans.

Banks are generally one of the first places people consider to ask for a loan, and for good reason. They usually have highly competitive interest rates on loans, and since many people already have a bank account, seeking a loan from the same institution makes sense. Add in online banking and ease of checking finances, and it certainly makes sense in some cases to use a bank.

However, banks are also much more strict with their policies and have very high credit standards. A low credit score could mean a quick refusal. They also tend to have higher fees on loans.

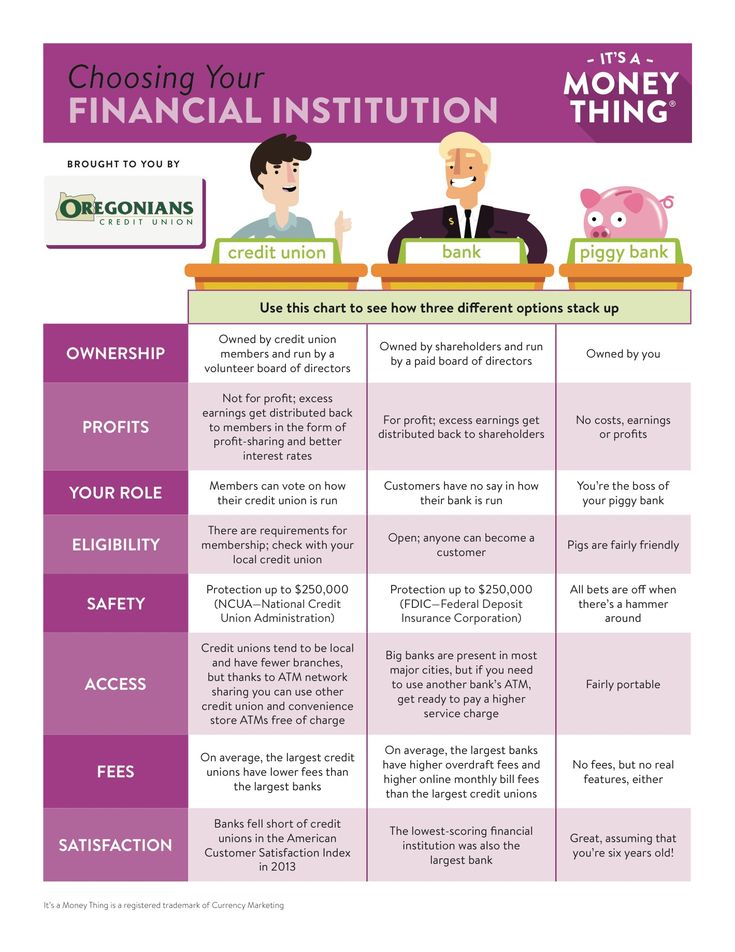

Unlike a bank, credit unions are owned by their Members and are not for-profit institutions. Because of this, they can offer much lower interest rates on recreational vehicle loans than a typical bank. Plus, credit unions are usually much smaller than banks, so you'll get more attentive service and personalized help with your loan application.

To take advantage of the low interest rates and personal service, you usually have to be a Member. With CU SoCal, joining is simple, so you can start enjoying the benefits of a credit union whenever you're ready. CU SoCal has a fully secure website and mobile app so you can stay up to date on your loan payments.

In the last few years, online lenders have become more and more ubiquitous in the financial world. Their strictly online presence means they've invested a lot into making a streamlined and intuitive user interface, which means their sites are easy to use for virtually any memeber.

That might not sound like a lot, but the ease of use means you can keep a better eye on what you owe on your loan. Users can also easily compare online lenders to see which one would be best for them.

For non-internet-savvy users, getting a loan from an online lender may not be the best idea, especially if they struggle to navigate or read websites.

Whether for cars or recreational vehicles, dealerships will often offer unique credit cards or special types of loans for items they sell.

There are several benefits to getting a dealership loan. Dealerships usually offer more options to customers with bad credit, so if your score isn't where you want it to be, you might be ok. It is also more convenient to accept a loan from the dealer since you are already there. Additionally, some lenders have exclusive partnerships with dealers, so you might be presented with more lenders than you would have otherwise.

The disadvantages of getting a loan with a dealership depend on the dealership itself and the ATV loan rates they offer.

Manufacturers often create exclusive relation-ships with financial institutions to create incentives that bring in more customers. These incentives could include extremely attractive benefits like 0% financing for the first year. Many ATV makers are linked up with a "captive lender" that offers a manufacturer loan, making this a viable option for ATV shoppers.

Along with different institutions from which to seek out a loan, there are also other types of ATV loan options that you can choose from. Here are the most common types.

RV loans are a dedicated type of loan specifically for purchasing recreational vehicles – from motorcycles, to boats, to your new ATV. You can get this kind of loan from banks, credit unions, and occasionally online lenders. Some lenders offer 3-6 months of no payments or reduced APR on RV loans.

You can get this kind of loan from banks, credit unions, and occasionally online lenders. Some lenders offer 3-6 months of no payments or reduced APR on RV loans.

As for disadvantages, there are quite a few with RV loans. Qualifying for a loan in the first place can be tricky, even more so than an auto loan. Keep in mind that the loan will also be secured by the vehicle itself as collateral.

That means if you stop making payments, the lender can repossess the ATV or UTV.

If you already have a credit card, you might be wondering if you can simply use it to buy your chosen ATV. The short answer is yes, and there are even some advantages to doing so.

If you have or qualify for a credit card that offers zero interest for the first year, you could pay off the ATV without added costs.

Don't forget, though, that credit cards don't enforce any payment over the monthly minimum. This might sound like a good thing, but unless you're making higher monthly payments, it could take you years to pay off the ATV.

Retailer financing is similar to getting a dealership or manufacturer loan. Essentially, what this means is that instead of applying for a separate loan elsewhere, you can take care of the loan directly at the point of sale and take advantage of manufacturer-subsidized loans.

Do keep in mind, though, that the most significant benefit of 0% APR for the first six months or year does end, and when it does, the interest rate will jump up to a much higher number than other types of loans.

Also, with retailer financing, your new ATV becomes the default collateral for the loan, so if you can't make payments, the retailer can repossess the vehicle.

At CU SoCal, we are big fans of the Southern California lifestyle – and that means always being on the go and having outdoor adventures year-round.

Whether you're looking for a four-wheeler or a side-by-side, we have you covered. With a loan from CU SoCal, you'll get up to 100% financing and a fixed interest rate, so there are no surprises to keep you from getting your ATV.

All of our terms are flexible and applicable to new and used vehicles. We don't ask for any application fees from our Members, so you can be sure that every penny will go toward getting the recreational vehicle of your dreams.

Please give us a call today at 866.287.6225 to schedule a no-obligation consultation with one of our vehicle loan representatives.

Get Started on Your ATV Loan!

Anyone who’s ridden an all-terrain vehicle (ATV) knows that there’s nothing like tearing through trails on a quad. But if you don’t the cash to buy a new 4X4 lying around, you’re going to need some financing.

ATV loans can run from 0% APR to over 25% APR. Since ATVs are often less expensive than other larger vehicles, you typically don’t have to make a down payment, so APR is the main cost you should be concerned with.

Since ATVs are often less expensive than other larger vehicles, you typically don’t have to make a down payment, so APR is the main cost you should be concerned with.

The easiest way to compare the cost of an ATV loan is to look at the APR, which is the interest and fees expressed as a percentage. Here’s how some of the top brands compare in June 2019:

| Yamaha | 15.99% – 23.99% plus offer |

| Polaris | 0% promotional APR for the first six months, 16.24% – 25.24% after |

| Honda | Starting at 0.99% |

| Very Good | 740–850 | 2%–11% |

| Good | 670–739 | 12%–15% |

| Fair | 580–669 | 15%–28% |

| Poor | 0–579 | 29%+ |

Lower credit can also affect which loan terms you qualify for. Generally, you’ll need to have at least good credit to qualify for longer terms. Other factors like your debt-to-income ratio can also factor into your rate.

Generally, you’ll need to have at least good credit to qualify for longer terms. Other factors like your debt-to-income ratio can also factor into your rate.

Fair and poor credit applicants can sometimes find long-term options, but with high interest rates that can make the loan incredibly expensive if you don’t pay it off early.

1 - 3 of 3

1 - 6 of 6

Got a vehicle in mind? Use this calculator to figure out how much your monthly repayment will cost with different loan terms and rates.

Eligibility can vary, depending on the lender and type of vehicle you’re interested in. However, you typically need to meet the following requirements to qualify:

The minimum age to take out a loan is 18 in most states. It’s 19 in Nebraska and Alabama, 21 in Mississippi.

The minimum age to take out a loan is 18 in most states. It’s 19 in Nebraska and Alabama, 21 in Mississippi.You can generally find ATV financing options for all credit score ranges. However, you’ll generally get a better deal if your credit score is above 670 — what most lenders consider to be “good credit.” You’ll have even more options if your score is 740 or higher.

Getting financing directly from your ATV dealer or manufacturer is a popular way to pay for a new vehicle. Here, you’re required to use your vehicle as collateral.

Some dealers offer financing directly from the manufacturer, which allows them to offer promotions like rebates or 0% interest for the first six months or a year on credit cards — often strategies for moving some of the less-popular models.

Many dealers offer financing through a third-party lender — like a bank or credit union. These can sometimes be less costly than manufacturer financing, but you might have a difficult time qualifying for a competitive loan if you don’t have excellent credit.

Some offer “buy here pay here” options for bad-credit borrowers, which don’t involve a credit check but can come with higher rates and hidden fees or unnecessary add-ons.

Don’t want to risk losing your vehicle? Taking out an unsecured personal loan is another option. You can apply for these online or through your local bank or credit union. Online lenders tend to get you your funds faster and don’t have strict credit requirements like many banks.

Some lenders have restrictions on how you can use your funds, though many don’t have any policies about recreational vehicles. Like with dealership financing, you’ll need good or excellent credit and a steady income to get approved for the most competitive rates and higher amounts.

Like with dealership financing, you’ll need good or excellent credit and a steady income to get approved for the most competitive rates and higher amounts.

Some personal loan providers like Capital One and USAA also offer ATV financing, which works more like borrowing from a dealership. Here, you’ll need to know the make and model of your vehicle, as well as the estimated cost. These loans tend to be secured.

Before you buy a new ATV, consider whether you want a new or used vehicle. Both come with benefits and drawbacks.

New ATVs can be more expensive, but don’t require as much upkeep in the beginning. They can come with lower APRs when you finance, and you don’t risk having hidden damaged parts that could set you back. However, you could end up having to pay for major repairs on an already-expensive vehicle if it gets totaled.

Used ATVs are generally much cheaper. Rather than paying thousands of dollars, it’s possible to find used ATVs for less than $300. While rates might be higher, you’ll still end up paying less — or you might not even need to get a loan to cover the upfront cost.

Rather than paying thousands of dollars, it’s possible to find used ATVs for less than $300. While rates might be higher, you’ll still end up paying less — or you might not even need to get a loan to cover the upfront cost.

This means that if you damage your vehicle, it’s less of a big deal. It could also be a good option for first-timers who don’t know how much they’re actually going to take it out. But there’s a chance you’ll need to replace some parts and spend some serious time in the garage.

Compare ATV loans

You can find a competitive deal by comparing these four main factors:

Most in-house ATV loans come with 36- to 60-month terms. Unsecured personal loans often come with a wider range of terms from 12 to 72 months.

A longer term can give you lower monthly repayments, but you’ll end up paying more in interest. A shorter term might save you on your total loan cost, but it’ll up your monthly repayments. To get the best of both worlds, use our calculator to find the shortest term length you can afford.

Many manufacturers only advertise the lowest possible rate on their websites, which only the most creditworthy borrowers can actually qualify for. But many manufacturers and online lenders allow you to apply to prequalify to get an estimate of the rates and loan amounts you can expect with no effect on your credit score.

Many manufacturers only advertise the lowest possible rate on their websites, which only the most creditworthy borrowers can actually qualify for. But many manufacturers and online lenders allow you to apply to prequalify to get an estimate of the rates and loan amounts you can expect with no effect on your credit score.Find an ATV loan

You can finance your ATV through a lender or manufacturer. Dealerships often offer a combination of lender and manufacturer financing with options that include:

Dealerships often offer a combination of lender and manufacturer financing with options that include:

Want to make sure your lender is legit? Watch out for these red flags when looking for ATV financing:

Check out how these top ATV brands compare.

| Yamaha | $2,099–$10,899 | Raptor, YFZ, Grizzly, Kodiak | Yamaha credit card |

| Textron | $2,999–$9,999 | Alterra, Mudpro | Installment loans through Sheffield Financial and Roadrunner Financial, Yard Card credit card |

| Polaris | $2,099–$27,499 | Polaris ACE, General, Ranger, RZR, Scrambler, Sportsman, Youth | Installment loans through Sheffield Financial, Synchrony Financial and Performance Finance; Polaris Visa Card credit card |

| Honda | $3,049–$16,699 | FourTrax, TRX, Pioneer | Term loans through Honda Financial Services, Honda Powersports credit card |

| Arctic Cat | $2,999–$12,999 | Alterra, 150, DVX, XT, Mudpro, 500, VLX, XC, TBX | Term loans through Sheffield Financial, Freedomroad Financial and Roadrunner Financial |

These quads are designed for fun. They’re faster, lighter and can absorb shock better than their counterparts. They’re also typically less expensive.

These quads are designed for fun. They’re faster, lighter and can absorb shock better than their counterparts. They’re also typically less expensive.Compare ATV financing

You can, but it won’t be cheap. That’s because lenders typically consider customers with bad credit to be high-risk borrowers. Some have credit cut-offs, meaning that you won’t be able to qualify. If you do qualify, expect a rate around 20% or higher.

Many dealerships for top manufacturers offer financing for lower-credit customers through Roadrunner Financial. These typically come with APRs ranging from 2.9% to 20.9% — competitive for that credit range — but require a down payment of up to 20%. Terms range between 6 and 72 months.

These typically come with APRs ranging from 2.9% to 20.9% — competitive for that credit range — but require a down payment of up to 20%. Terms range between 6 and 72 months.

If you’ve had trouble getting approved in the past, it might be tempting to go with a lender that promises no credit check. However, at best these can be highly expensive loans, and at worst, scams.

Between in-house financing and personal loans, you’ve got lots of options to choose from when it comes to paying for a new or used ATV. Dealership financing might be easier, but you have less options to explore — and you could find more competitive rates elsewhere.

Get started on your search by checking out our personal loans guide to learn more about how they work and compare lenders.

It’s possible. But rather than looking into no credit check loans, you might want to apply with a cosigner. Some in-house financing options like Roadrunner allow you to apply with a cosigner. You might also want to check out your cosigner-friendly personal loan options.

You might also want to check out your cosigner-friendly personal loan options.

You can. ATV wheels can set you back several hundred dollars a piece, which adds up. You can typically get financing either through the manufacturer or by taking out a personal loan.

MSRP stands for manufacturer’s suggested retail price. You probably saw MSRP when checking out models on a manufacturer’s site. It means that dealerships might charge a different price, though you can expect something in that ballpark.

It depends on your loan term. These can run anywhere from 12 to 72 months — or one to six years. With some lenders, you might be able to save on interest by paying off your loan early as long as there aren’t any prepayment penalties and you loan doesn’t come with precomputed interest.

Image Source: Shutterstock

Was this content helpful to you?

Thank you for your feedback!

Anna Serio is a lead editor at Finder, specializing in consumer and business lending. A trusted lending expert and former commercial loan officer, Anna's written more than 1,000 articles on Finder to help Americans strengthen their financial literacy. Her expertise and analysis on personal, student, business and car loans has been featured in Business Insider, CNBC and the Simple Dollar, and she was recognized as an expert contributor in finance by Best Company in 2020. Anna holds an MA in Near and Middle Eastern studies from the American University of Beirut and a BA in creative writing and Arabic from Macaulay Honors College at Hunter College, CUNY.

A trusted lending expert and former commercial loan officer, Anna's written more than 1,000 articles on Finder to help Americans strengthen their financial literacy. Her expertise and analysis on personal, student, business and car loans has been featured in Business Insider, CNBC and the Simple Dollar, and she was recognized as an expert contributor in finance by Best Company in 2020. Anna holds an MA in Near and Middle Eastern studies from the American University of Beirut and a BA in creative writing and Arabic from Macaulay Honors College at Hunter College, CUNY.

Autopay car loan review FedEx Employees Credit Association auto loans review

Gravity Lending review

Gravity Lending matches borrowers with lenders so you can get the best vehicle refinancing deal out there.

RefiJet review

RefiJet helps you save on your monthly car payment or interest with a few simple steps.

How to finance a Ram pickup

Get competitive rates on your next car loan when you finance this full-size pickup truck.

Vroom vs. Carvana

Both Vroom and Carvana offer loans for their used car inventories. But when it comes to transparency and loan terms, Carvana takes the cake.

Carvana vs. Carmax

Two used car dealerships with competitive rates and quick online financing.

☑ Save up to 40% of the contract value

☑ 10% discount on the purchase of CFMOTO from 3 units for commercial use

☑ Easier than leasing. More affordable than a loan

More affordable than a loan

We offer the most favorable conditions for the purchase of CFMOTO ATVs on the market.

This is more profitable than conventional leasing and easier than buying on credit.

Read the comparison table and draw your own conclusions.

| CFMOTO Business Program | Other leasing programs | Unsecured lending programs for legal entities. persons | |

|---|---|---|---|

| Application review | |||

| Minimum set of documents | ⭐️⭐️⭐️⭐️⭐️ | ⭐️⭐️⭐️ | ⭐️⭐️ |

| Application decision speed | ⭐️⭐️⭐️⭐️⭐️ | ⭐️⭐️⭐️ | ⭐️⭐️ |

| Application approval loyalty | ⭐️⭐️⭐️⭐️⭐️ | ⭐️⭐️⭐️ | ⭐️⭐️ |

| Registration of the transaction | |||

| Ease of transaction | ⭐️⭐️⭐️⭐️⭐️ | ⭐️⭐️⭐️ | ⭐️⭐️ |

| Accounting on the balance sheet of your company | NO | YES | YES |

| Ease of accounting | ⭐️⭐️⭐️⭐️⭐️ | ⭐️⭐️⭐️ | ⭐️⭐️ |

| Payment of additional expenses (OSAGO, taxes, registration costs, etc.) | NO | YES | YES |

| Redemption option for an individual | YES | HARD | HARD |

| Program conditions | |||

| Compulsory equipment insurance | NO | YES | NO |

| Additional services | |||

| Individual manager/contract support | ⭐️⭐️⭐️⭐️⭐️ | ⭐️⭐️⭐️ | ⭐️⭐️ |

You can do it through the form on our website or by phone +7(495) 127-01-50

We will contact you to confirm the application, clarify the models of equipment and your wishes for a complete set.

You send us the minimum package of documents to approve the transaction

We inform you about the agreement of the transaction and send you contracts for signing (signing by EDI is possible)

You pay an advance payment and sign documents

No additional expectations. You immediately pick up the equipment.

We register your equipment and send you the necessary documents and registration number

You use your equipment and don't forget to pay rent

We deregister your equipment and register it as your property (registration is possible both for a legal entity and for an individual)

Your name

Your e-mail

Your phone

What equipment would you like to lease?

Additional requests

Please leave this field empty.

The amount of the first payment is an advance from 30% to 60%

Required documents:

Download documents

Preliminary decision - in 15 minutes, final approval - within 24 hours.

Lease-to-purchase agreement is concluded for a period of 12 to 36 months.

You don't have to worry about it. The equipment is registered by the lessor.

The lessor is the owner of the equipment until the lessee fulfills all obligations. After paying the redemption payment, the ownership of the equipment is transferred to the client.

December 22, 2014

12/22/14

3 minutes

7k

3 minutes

7 150

129

0

In the summer season, many fans of extreme recreation seriously think about buying an ATV. Off-road driving, fresh air and a great way to get away from the bustle of the city! However, most of those who want to purchase an ATV do not know the legal aspects of registering it with government agencies and obtaining the right to drive. This is what will be discussed below.

From a legal point of view, an ATV is a wheeled off-road motor vehicle.

ATVs are technically classified as motor vehicles. The list of all motor vehicles is indicated in Appendix No. 1 of Decree of the Government of the Russian Federation of September 10, 2009 No. 720.

To control this type of equipment, you need a certificate of a tractor driver (tractor driver) of category A1, which is expressly indicated in paragraphs. 3 4 Decrees of the Government of the Russian Federation dated 12.07.1999 N 796.

3 4 Decrees of the Government of the Russian Federation dated 12.07.1999 N 796.

To drive a quad bike you need:

The exam is taken by the Gostekhnadzor body, after writing an application, presenting a passport, a medical certificate, if you were trained at a driving school, you must present a document confirming the completion of training, a photo and a receipt for paying the state duty. The exam takes place at the place of registration of the candidate for obtaining the right to drive an ATV.

You got the right to drive an ATV! Perfect! Now you need to get the long-awaited ATV!

Decree of the Government of the Russian Federation of 12. 08.1994 N 938 obliges to register motor vehicles with a working volume of an internal combustion engine of more than 50 cubic meters. cm or a maximum motor power of more than 4 kW. That is, if your ATV has an engine with a power higher than the values indicated above, its registration is required.

08.1994 N 938 obliges to register motor vehicles with a working volume of an internal combustion engine of more than 50 cubic meters. cm or a maximum motor power of more than 4 kW. That is, if your ATV has an engine with a power higher than the values indicated above, its registration is required.

If, according to the technical documentation for your ATV, it is allowed to use it on public roads and its speed exceeds 50 km / h, then the ATV can be registered with the traffic police of the Ministry of Internal Affairs of the Russian Federation and Gostekhnadzor. And if your ATV cannot be used on public roads, then registration is carried out only in Gostekhnadzor.

After the purchase of an ATV, the law provides 10 days for its registration, which is carried out upon presentation of a document confirming the acquisition of ownership of the ATV (contract of sale, exchange, donation, certificate of inheritance, etc.), and the passport of the corresponding vehicle (ATV ).

Separately, it is worth mentioning OSAGO. Quad bikes can be issued either PTS (vehicle passport) or PSM (self-propelled vehicle passport). If your ATV is equipped with a PTS, then it can be used on public roads. If your ATV develops a speed of more than 20 km/h, then to register such an ATV you need an OSAGO policy. If your ATV has a PSM, then it cannot be operated on public roads and an OSAGO policy is not required.

As for technical inspection. If you are the owner of an ATV with a PTS, then in the first three years, including the year of manufacture, inspection is not required, you will receive OSAGO without hindrance. If the ATV is already from three to seven years old, then the inspection is carried out every 24 months. Without such an examination and a diagnostic card, you will not receive OSAGO. ATVs over seven years old should be inspected every 12 months. Simply put, ATVs with PTS are operated like ordinary motor vehicles and motorcycles, the procedure for carrying out all legal procedures is similar to that applied to ordinary cars.

If you have an ATV with PSM, then you need to obtain a certificate of technical inspection annually. With regard to ATVs, from the date of manufacture of which no more than one year has passed and which have not been in operation, the first technical inspection is carried out without checking the technical condition of the ATV, which is indicated in clause 5 of Decree of the Government of the Russian Federation of November 13, 2013 No. 1013 On technical inspection self-propelled machines and other types of equipment registered by the bodies exercising state supervision over their technical condition.

Now you are familiar with the main aspects of acquiring and driving an ATV, you can safely go towards extreme recreation. Good luck!

Author: Orest Matsala, lawyer at the European Legal Service

We publish only verified information

Article author

Antonova Marina Alexandrovna Lead Alimony Lawyer

Experience 11 years

Consultations 30000

Expert in alimony collection and family law.