Retirement Read Time: 4 min

In a recent survey, 70% of current workers stated they plan to work for pay after retiring.1

And that possibility raises an interesting question: how will working affect Social Security benefits?

The answer to that question requires an understanding of three key concepts: full retirement age, the earnings test, and taxable benefits.

Most workers don't face an "official" retirement date, according to the Social Security Administration. The Social Security program allows workers to start receiving benefits as soon as they reach age 62 – or to put off receiving benefits up until age 70. 2

"Full retirement age" is the age at which individuals become eligible to receive 100% of their Social Security benefits. Individuals born in 1960 or later can receive 100% of their benefits at age 67.

Starting Social Security benefits before reaching full retirement age brings into play the earnings test.

If a working individual starts receiving Social Security payments before full retirement age, the Social Security Administration will deduct $1 in benefits for each $2 that person earns above an annual limit. In 2022, the income limit is $19,560.2

During the year in which a worker reaches full retirement age, Social Security benefit reduction falls to $1 in benefits for every $3 in earnings. For 2022, the limit is $51,960 before the month the worker reaches full retirement age.2

For example, let's assume a worker begins receiving Social Security benefits during the year he or she reaches full retirement age. In that year, before the month the worker reaches full retirement age, the worker earns $65,000. The Social Security benefit would be reduced as follows:

| Earnings above annual limit | $65,000 – $51,960 = 13,040 |

One-third excess | $13,040 ÷ 3 = $4,347 |

In this case, the worker's annual Social Security benefit would have been reduced by $4,347 because they are continuing to work.

Once you reach full retirement age, Social Security benefits will not be reduced no matter how much you earn. However, Social Security benefits are taxable.

For example, say you file a joint return, and you and your spouse are past the full retirement age. In the joint return, you report a combined income of between $32,000 and $44,000. You may have to pay income tax on as much as 50% of your benefits. If your combined income is more than $44,000, as much as 85% of your benefits may be subject to income taxes.2

There are many factors to consider when evaluating Social Security benefits. Understanding how working may affect total benefits can help you put together a strategy that allows you to make the most of all your retirement income sources – including Social Security.

1. EBRI.org, 2022

2. SSA.gov, 2022

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright FMG Suite.

It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright FMG Suite.

Share |

Is Social Security taxable? For most Americans, it is. That is, a majority of those who receive Social Security benefits pay income tax on up to half or even 85% of that money because their combined income from Social Security and other sources pushes them above the very low thresholds for taxes to kick in.

But there are three strategies you can use—place some retirement income in Roth IRAs, withdraw taxable income before retiring, or purchase an annuity, to limit the amount of tax you pay on Social Security benefits.

Social Security payments have been subject to taxation above certain income limits since 1983. No inflation adjustments have been made to those limits since then, so most people who receive Social Security benefits and have other sources of income pay some taxes on the benefits.

No inflation adjustments have been made to those limits since then, so most people who receive Social Security benefits and have other sources of income pay some taxes on the benefits.

However, regardless of income, no taxpayer has all their Social Security benefits taxed. The top level is 85% of the total benefit. Here’s how the Internal Revenue Service (IRS) calculates how much is taxable:

The amount you owe depends on precisely where that number lands in the federal income tax tables.

The amount you owe depends on precisely where that number lands in the federal income tax tables.Combined Income = Adjusted Gross Income + Nontaxable Interest + Half of Your Social Security Benefits

The key to reducing taxes on your Social Security benefit is to reduce the amount of taxable income you have when you retire, but not to reduce your total income.

Benefits will be subject to tax if you file a federal tax return as an individual and your combined gross income from all sources is as follows:

The IRS has a worksheet that can be used to calculate your total income taxes due if you receive Social Security benefits. When you complete this exercise in arithmetic, you will find that your taxable income has increased by up to 50% of the amount you received from Social Security if your gross income exceeds $25,000 for an individual or $32,000 for a couple. The taxed percentage rises to 85% of your Social Security payment if your combined income exceeds $34,000 for an individual or $44,000 for a couple.

The taxed percentage rises to 85% of your Social Security payment if your combined income exceeds $34,000 for an individual or $44,000 for a couple.

For example, say you were an individual taxpayer who received the average amount of Social Security: about $18,000. You also had $20,000 in “other” income. Add the two together, and you have a gross income of about $38,000. However, your combined income is computed as only $29,000 (other income plus half of your Social Security benefits). That’s within the $25,000–$34,000 range for a tax of 50% of your benefits So, half of the difference between that income and the $25k threshold is your taxable amount: ($28,000 - 25,000 = $3,000; $3,000/2 = $1,500). The calculation can become more complicated for taxpayers with different forms of income.

For couples who file a joint return, your benefits will be taxable if you and your spouse have a combined income as follows:

For example, say you are a semi-retired couple filing jointly and have a combined Social Security benefit of $26,000. You also had $30,000 in combined “other” income. Add the two together, and you have a gross income of $56,000. Your combined income for Social Security is $43,000 (other income plus half of your Social Security benefits). This combined income falls in the $32,000–$44,000 range, meaning that half the difference between the income and the threshold is computed at 50% to get your amount taxable: ($43,000-32,000 = $11,000; $11,000/2 = $5,500).

This being the IRS, the straightforward example above may not apply to you. The IRS’s Interactive Tax Assistant (ITA) will lead you through the possible complications and calculate what part of your income is taxable. IRS Notice 703 describes the tax rules for benefits.

These programs follow the same general rules as the Social Security program for retirees, except for Supplemental Security Income (SSI).

If you don’t have Social Security benefits but collect spousal Social Security benefits based on your marital partner’s benefits, the rules are the same as for all other Social Security recipients. If your income is above $25,000, then you will owe taxes on up to 50% of the benefit amount. The percentage rises to 85% if your income is above $34,000.

Survivor benefits paid to children are rarely taxed because few children have other income that reaches the taxable ranges. The parents or guardians who receive the benefits on behalf of the children do not have to report them as part of their income.

Social Security disability benefits follow the same rules on taxation as the Social Security retiree program. Benefits are taxable if the recipient’s gross income is above a certain level. The current threshold is $25,000 for an individual and $32,000 for a couple filing jointly.

SSI is not Social Security; it’s a needs-based program for people who are blind, disabled, or age 65 and older. SSI benefits are not taxable.

SSI benefits are not taxable.

You should get a Social Security Benefit Statement (Form SSA-1099) each January detailing your benefits during the previous tax year. You can use it to determine whether you owe federal income tax on your benefits. The information is available online if you enroll on the Social Security website.

If you owe taxes on your Social Security benefits, you can make quarterly estimated tax payments to the IRS or have federal taxes withheld from your payouts before you receive them.

Eleven states tax Social Security benefits in some cases. Check with your state tax agency if you live in one of these states—Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, Rhode Island, Utah, Vermont, or West Virginia. As with the federal tax, how these agencies tax Social Security varies by income and other criteria.

The average monthly Social Security retirement benefit is $1,688. 35 That’s $20,266.20 a year.

35 That’s $20,266.20 a year.

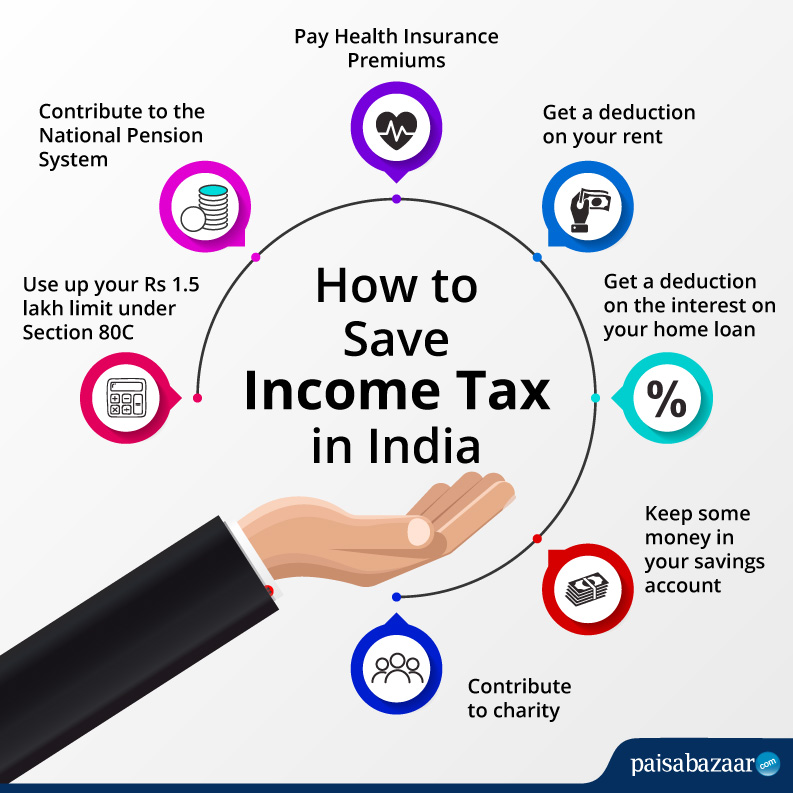

The simplest way to keep your Social Security benefits free from income tax is to keep your total combined income below the thresholds to pay tax. However, this may not be a realistic goal for everyone, so there are three ways to limit the taxes that you owe.

Contributions to a Roth IRA or Roth 401(k) are made with after-tax dollars. This means they’re not subject to taxation when the funds are withdrawn. Thus, the distributions from your Roth IRA are tax-free, provided that they’re taken after you turn 59½ and have had the account for five or more years. As a result, the Roth payout won’t affect your taxable income calculation and won’t increase the tax you owe on your Social Security benefits. Distributions taken from a traditional IRA or traditional 401(k) plan, on the other hand, are taxable.

The Roth advantage makes it wise to consider a mix of regular and Roth retirement accounts well before retirement age. The blend will give you greater flexibility to manage the withdrawals from each account and minimize the taxes you owe on your Social Security benefits. A similar effect can be achieved by managing your withdrawals from conventional savings, money market accounts, or tax-sheltered accounts.

Another way to minimize your taxable income when drawing Social Security is to maximize, or at least increase, your taxable income in the years before you begin to receive benefits.

You could be in your peak earning years between ages 59½ and retirement age. Take a chunk of money out of your retirement account and pay the taxes on it. Then, you can use it later without pushing up your taxable income.

This means you could withdraw funds a little early—or “take distributions,” in tax jargon—from your tax-sheltered retirement accounts, such as IRAs and 401(k)s. You can make penalty-free distributions after age 59½. This means you avoid being dinged for making these withdrawals too early, but you must still pay income tax on the amount you withdraw.

You can make penalty-free distributions after age 59½. This means you avoid being dinged for making these withdrawals too early, but you must still pay income tax on the amount you withdraw.

Since the withdrawals are taxable (unless they’re from a Roth account), they must be planned carefully with an eye on the other taxes you will pay that year. The goal is to pay less tax by making more withdrawals during this pre–Social Security period than you would after you begin to draw benefits. That requires considering the total tax bite from withdrawals, Social Security benefits, and other sources.

Be mindful, too, that you’re required to take RMDs from your 401(k) or traditional IRA after a certain age. As of 2023, you must start taking distributions starting in the year you turn 73 for those born between 1951 and 1959, and age 75 for those born after 1960.

This strategy has another benefit: By using these distributions to boost your income when you’re retired or nearing retirement, you might be able to delay applying for Social Security benefits, which will increase the size of the payments.

A qualified longevity annuity contract (QLAC) is a deferred annuity funded with an investment from a qualified retirement plan or an IRA. QLACs provide monthly payments for life and are shielded from stock market downturns. As long as the annuity complies with IRS requirements, it is exempt from the RMD rules until payouts begin after the specified annuity starting date.

By limiting distributions—and thus taxable income—during retirement, QLACs can help minimize the tax bite taken from your Social Security benefits. Under the current rules, an individual can spend 25% or $135,000 (whichever is less) of a retirement savings account or an IRA to buy a QLAC with a single premium. The longer an individual lives, the longer the QLAC pays out.

QLAC income can be deferred until age 85. A spouse or someone else can be a joint annuitant, meaning that both named individuals are covered regardless of how long they live.

Remember that a QLAC shouldn’t be bought only to minimize taxes on Social Security benefits. Retirement annuities have advantages and disadvantages that should be weighed carefully, preferably with help from a retirement advisor.

Retirement annuities have advantages and disadvantages that should be weighed carefully, preferably with help from a retirement advisor.

Add up your gross income for the year, including Social Security. If you have little or no income besides your Social Security, you won’t owe taxes on it. However, if you’re an individual filer with at least $25,000 in gross income, including Social Security for the year, then up to 50% of your Social Security benefits may be taxable. For a couple filing jointly, the minimum is $32,000. If your gross income is $34,000 or more (or a couple’s income is $44,000 or more), then up to 85% may be taxable.

If you file as an individual, your Social Security is not taxable if your total income for the year is below $25,000. Half of it is taxable if your income is in the $25,000–$34,000 range. If your income is higher, up to 85% of your benefits may be taxable.

If you and your spouse file jointly, you’ll owe taxes on half of your benefits if your joint income is in the $32,000–$44,000 range. If your income exceeds that, then up to 85% is taxable.

Thirty-eight states do not impose taxes on Social Security benefits. The other 12 tax some recipients under some circumstances.

Yes, but you can minimize the amount you owe each year by making wise moves before and after you retire. Consider investing some of your retirement savings in a Roth account to shield your withdrawals from income tax. Take out some retirement money after you’re 59½, but before you retire to pay for expected taxes on your Social Security before you begin receiving benefit payments. You might also talk to a financial planner about a retirement annuity.

Social Security is taxable based on your total income, not age; however, the taxable amount varies from zero to 85% depending on your total income.

Most advice on Social Security benefits focuses on when you should start taking benefits. The short answer is to wait until you’re age 70 to maximize the amount that you get. Still, another consideration is how to prevent your Social Security benefits from taking a big tax bite out of your overall retirement income. The answer is to plan well in advance to minimize your overall tax burden during your retirement years.

Work

Updated 02/13/2023

Students, pensioners, housewives, as well as employees - many people earn extra money in the so-called "mini jobs". In this chapter, we will explain what a "Minijob" is and what should be paid attention to those who have such a job.

Listen

A minijob is a minimum wage job where you can't earn more than 520 euros per month. Or they are employed for a short period of time - a few weeks or months. Thus, Minijob can be of two types:

Or they are employed for a short period of time - a few weeks or months. Thus, Minijob can be of two types:

It is possible to work on a minimum wage both in enterprises and in private households. Many Minijobs can be found in gastronomy, retail or crafts. In private households on a minimum employment basis, one can work as a janitor (cleaning lady), housekeeper (helper) or looking after children.

In private households on a minimum employment basis, one can work as a janitor (cleaning lady), housekeeper (helper) or looking after children.

Minimum wage workers have the same rights as other wage earners. Therefore, you too are entitled to the statutory minimum wage or vacation. You can learn more about the rights of employees in the chapters "Rights of employees" and "Employment contract".

Yes. Persons with minimum employment are exempted from social contributions. This means that you do not have to pay insurance premiums in case of disability or loss of employment. You can also avoid paying pension contributions. To do this, you need to submit an appropriate application to the employer. Otherwise, part of your earnings will be deducted to the pension fund. Your income will decrease slightly, but you will be eligible for (small) pension benefits and be able to retire earlier. For more information on pensions, see the chapter "Pensions in Germany".

Please note: every person living in Germany must have health insurance. Including persons with minimum employment. Since your employment does not include mandatory social security contributions, you must be insured otherwise. For example, through family or student health insurance. If this is not possible, you will have to make the recurring payments yourself. More information about health insurance in Germany in the chapter "Health insurance in Germany".

Including persons with minimum employment. Since your employment does not include mandatory social security contributions, you must be insured otherwise. For example, through family or student health insurance. If this is not possible, you will have to make the recurring payments yourself. More information about health insurance in Germany in the chapter "Health insurance in Germany".

You have to pay taxes even if you work for a Minijob.

In the case of a "mini-job" where you cannot earn more than a certain statutory amount, the so-called lump-sum taxation is generally chosen. Your employer will pay a lump sum tax of 2% of your monthly earnings for you. At this point, your tax obligations are considered fulfilled.

In the case of short-term employment , there are two options: 25% lump-sum taxation (plus solidarity tax surcharge (Solidaritätszuschlag) and church tax if you pay it) or individual taxation with a tax card (Lohnsteuerkarte). As a rule, the second option is more profitable: in this case, you are exempt from paying taxes if you earn less than the tax-free minimum (Grundfreibetrag). More information on taxes can be found in the chapters "The German Tax System" and "Tax Declaration".

As a rule, the second option is more profitable: in this case, you are exempt from paying taxes if you earn less than the tax-free minimum (Grundfreibetrag). More information on taxes can be found in the chapters "The German Tax System" and "Tax Declaration".

Yes. However, if your total earnings exceed 520 euros per month, or in the case of short-term employment, you work more than 3 months or 70 working days in a year, your employment will no longer be considered minimum employment. This means, for example, that you will have to pay mandatory social security contributions.

Yes. However, your employer must agree to this. If you work part-time on a Minijob in only one place, then you are not required to pay mandatory social security contributions from this part-time job. However, if you work part-time in several places at once, your income from the second and subsequent part-time jobs is added to the income that you receive from your main job. In this case, mandatory social security contributions are calculated on the basis of this total income.

There is no lower or upper limit for hours of operation. It is only important that your earnings do not exceed 520 euros per month, and the period of work in the case of short-term employment is not more than three months or 70 working days.

If you regularly earn more than 520 euros per month, your employment will not be considered minimum (Minijob), but medium (Midijob). In this case, you are required to pay social security contributions. For more information on the topic of average employment, see the What is a Midijob? section. If your earnings exceeded the limit unintentionally (for example, because you replaced a sick colleague) and this happened no more than three times a year, your employment is still considered minimal (Minijob).

Yes. However, if you apply for a minijob and receive benefits from a job center or unemployment benefit (Arbeitslosengeld I), there are a number of things to consider.

If you receive benefits from the Jobcenter:

If you don't, your benefits will be cut.

If you don't, your benefits will be cut. If you receive unemployment benefits (Arbeitslosengeld I):

If you earn from 520.01 to 1600 euros per month, you have an average employment (Midijob). Unlike the minimum, the average employment provides for the deduction of mandatory contributions to social insurance funds. These payments are, of course, less than for full-time employees. In doing so, you also acquire the right to pension benefits. For more information on pensions, see the chapter "Pensions in Germany".

Please note: If you work for Midijob in several places at once, your earnings are summed up. You are only entitled to benefits provided for medium-sized workers if your total earnings do not exceed 1,600 euros. If, while working for a Midijob, you also work part-time on a Minijob, then you are exempt from paying social security contributions from this part-time job. However, if you have a Minijob - a part-time job in several places at once, your income from the second and subsequent part-time jobs is added to the income received from the Midijob. If you collectively earn more than 1,600 euros in different places, you will no longer be eligible for Midijob benefits.

Jobs

How to look for a job in Germany? What documents do I need to submit and how is the interview going? In our chapter we will share[...]

Jobs

Laws and rights

Is it possible to have additional income in Germany in addition to the main job? What can you get reprimanded for? And what will happen if[...]

Job

Once you have found a job in Germany, do not rush to sign an employment contract. First, you should read it carefully. And what[...]

Project:

Supported by:

Author Peter Kuznetsov To read 12 min Published Updated

Content

Which pension fund is better to transfer? Is the pension subject to income tax? Such questions arise when a pensioner decides to take advantage of the personal income tax deductions provided for by tax legislation. After all, if a pensioner has no taxable income, then he has nothing to reimburse the tax from.

In accordance with paragraph 1.7 of Art. 208 of the Tax Code of the Russian Federation, pensions are recognized as income received from the sources of the Russian Federation on payments from Russian organizations or outside of it from a foreign company through a separate subdivision in the Russian Federation. And income is subject to taxation at a rate of 13% (clause 1, article 224 of the Tax Code of the Russian Federation).

To deal with the question of whether your pension is subject to personal income tax, you must consider the following:

It should be noted that pensions in the Russian Federation can be accumulated either in the state pension fund (including under agreements on voluntary insurance of the funded part of the pension), or non-state. The action of the state provision of pensions is regulated by the laws “On State Pension Provision” dated December 15, 2001 No. 166-FZ and “On Insurance Pensions” dated December 28, 2013 No. 400-FZ.

Non-state pension provision is made in accordance with the law "On non-state pension funds" dated 07.05.1998 No. 75-FZ.

Within the framework of the Tax Code of the Russian Federation, the procedure for taxation of pensions formed by transferring contributions to state or non-state funds has different specifics.

Thus, non-state pensions are subject to personal income tax.

Find out what the pension will be in the absence of work experience from this publication.

Income tax refund can be made by a pensioner in the following cases:

This article will tell you about the nuances of calculating a pension.

Is it possible to transfer the funded part of the pension? Yes, this is not prohibited and highly desirable, since by default the funded part will be transferred to the insurance part and, of course, no increase in profitability should be expected.

Where can I transfer the funded part of the pension? To any non-state pension fund (hereinafter - NPF). The future pensioner will only need to choose where it is better to transfer the funded part of the pension. It is highly desirable to opt for an NPF, which is part of the guarantee system and has several management companies.

How to transfer the funded part of the pension? Appropriate transfer applications must be submitted to the selected NPF and to the FIU.

All pensions received by pensioners are income. However, personal income tax is not taxed on state pensions, and only pensions paid by non-state funds are subject to taxation. Thus, if a non-working pensioner decides to use, for example, a property personal income tax deduction, then he will be able to do this if, before the right to deduction arose, he received taxable income or receives a non-state pension for the previous three years.

More information on the topic can be found in ConsultantPlus.

Trial free access to the system for 2 days.

A pension is a regular state payment in favor of a specific entity. The grounds for paying pension accruals can be different: for old age, for disability, for the loss of a breadwinner, and others.

When assigning any additional allowances, benefits, subsidies, all incomes of a person, including pension payments, are taken into account. Therefore, many pensioners are interested in the question of whether the pension is the income of an individual and whether it is subject to taxation.

From a legal point of view, a pension is a regular receipt of funds by a person. That is, such benefits are considered income. Although some people think that all income should be the result of some kind of activity. For example, he did a job, rendered a service, received well-deserved money. However, in order to receive pension accruals, there must be some reason - reaching a certain age, length of service, assignment of disability, loss of a breadwinner.

From the point of view of the tax authorities, pension funds are tax-free income . This is established by Article 217 of the Tax Code (second part). This article expressly states that state, insurance, funded pensions, as well as additional payments to them, are not subject to taxation, although they are considered direct income of individuals.

However, receiving a pension does not exempt pensioners from paying debts, debts, alimony, which can be written off from the funds by force. When assigning any benefits, for example, for children, for the poor, as well as when applying for subsidies and additional payments, the earnings of citizens, that is, the amount of pension accruals, are also taken into account.

Important! Non-state pension provision is subject to personal income tax, unlike state payments.

It should be noted that each type of pension provision has its own characteristics.

Old-age pension payments are treated as profit. Not having sufficient experience to receive an insurance pension, citizens become recipients of old-age benefits when they reach the legal age. Alimony deductions, as well as collections on accounts payable, are permissible from such accruals.

A person receiving an old-age pension can take out a loan, but with the additional condition of life insurance. Not every bank approves a loan for an elderly person.

A funded or insurance pension is also considered to be the income of individuals and is paid subject to reaching a certain age, as well as having worked out the length of service and pension points. The amount of these funds depends on the insurance premiums made.

This type of accrual is not subject to any taxes. However, when a debt is formed or by a court decision, it is lawful to withhold a part of the funds from the total amount of accruals.

This type of payment relates to profit and is due to military personnel, as well as law enforcement officers. To receive military payments, a certain length of service is required. This type of accrual can be paid along with other amounts.

The military pension is classified as a state type, therefore it is not taxed. If necessary, penalties may be imposed on military accruals . Military personnel and other citizens receiving military payments are exempt from certain types of taxes and have a number of preferences.

The money received by a disabled person is included in his income. According to the current legislation, the disability pension is not subject to taxation. Disability accruals are important when applying for benefits for the poor, as well as for obtaining other material assistance for the disabled and low-income citizens.

It is not uncommon for people with disabilities to ask lawyers for clarification if alimony and other debts are withheld from their salaries. By law, maintenance and other deductions from disability funds can be , however, the amount of penalties should not be more than half of the transfers.

At the legislative level, the pension for the loss of a breadwinner refers to the types of income of individuals. However, survivor benefits should not be taxed. At the same time, this type of accrual is taken into account when applying for any benefits, subsidies and benefits. Survivor benefit recipients are entitled to take out a loan if necessary.

Help! It should be noted that credit institutions are in no hurry to approve loans and mortgages to recipients of this type of profit.

State pension recipients, even without other income, can apply for a loan, since these payments are a type of profitable funds of individuals that are not taxed. Also, the amount of pension accruals is taken into account when applying for additional benefits, benefits, additional payments and subsidies.

Pensioners can apply to any bank if they need a loan . However, it should be borne in mind that not all credit organizations approve loans to pensioners. When approving loans, bank employees look not only at the amount of accruals, but also at the age of the applicant, his state of health. Many banks will reject loan approval if the applicant does not want to take out life insurance. They are reluctant to approve loans to recipients of old-age, disability and survivors' pensions.

By law, bailiffs can impose a penalty on any income of a citizen if the person has a debt, a fine, maintenance obligations. An exception is the enrollment for the loss of a breadwinner. Bailiffs cannot impose a penalty or arrest on this type of savings.

In all other cases bailiffs can impose a penalty on pension payments if the pensioner has debts :

To impose a penalty or arrest, it is necessary to have a court decision and an executive document. Without the presence of any one document, the recovery will be considered illegal and illegal.

Attention! The amount of recovery cannot be more than 50% of the total amount of accruals. In addition, if the pension is the only source of income and its amount is less than one subsistence minimum, the recovery will be considered unlawful. In this case, the bailiff may seize movable or immovable property owned by the debtor.

When tax is withheld from pensions:

The current legislation classifies state pensions as personal income. According to the tax legislation, public funds are not taxed. However, the funds received may be subject to foreclosure or seizure of funds if the pensioner has outstanding debt or maintenance obligations. The amount of funds received is taken into account when applying for benefits, subsidies, additional payments, as well as when applying for loans and borrowings.

The fact that a person has a bank deposit can sometimes affect their receipt of Social Security benefits. What subsidies will be difficult to obtain if there is a large amount of interest received on a bank deposit? What happens if you try to hide the presence of a contribution from social security? We tell in our article.

Since most of the benefits are granted when there is insufficient income per family member, accounting for interest received on the deposit affects the calculation of average per capita income. And consequently, the income per family member may exceed the threshold at which social benefits are assigned.

Experts of "ConsultantPlus" told how the average per capita income is calculated. If you don't have access to K+, get it for free online on a trial basis.

Note that the appointment of benefits is not affected by the very fact of having a deposit in a bank, but by the income received in the form of bank interest.

What benefits can be lost if there is interest income on the deposit?

One such benefit is a utility bill subsidy. So, if the share of expenses for housing and communal services in the structure of average per capita income exceeds a certain level, such families are allocated a subsidy to partially compensate for expenses.

The share of housing and communal services can vary significantly by region. If in Moscow it is 3-10%, in St. Petersburg - 14%, then in the regions - about 22%.

Accounting for interest on the deposit when assigning this subsidy is provided for by Decrees of the Government of the Russian Federation dated 08.20.2003 No. 512 and dated 12.14.2005 No. 761. percent. If, taking into account this amount, the share of utility costs turns out to be less than the established level for the region, the subsidy will be refused.

The exact amount of interest that will affect the appointment of a subsidy cannot be named. This is only one component in the total income of a citizen. But if the amount is significant, with a high degree of probability the person will not be able to qualify for subsidizing housing and communal services.

Also, the interest on the deposit may affect the cash payment to labor veterans. The list of income for the purpose of this payment also includes bank interest (Government Decree No. 512 of August 20, 2003). In a number of regions, deposits are not taken into account by the decision of the relevant subject of the Russian Federation. But if the calculation is made according to federal income accounting rules, payments can be lost.

Interest on the deposit is also taken into account when assigning allowances for children aged three to seven and eight to sixteen years old. Government Decrees No. 384 dated March 31, 2020 and No. 1037 dated June 28, 2021 provide that these payments are due only to low-income families. The presence of income from the contribution can deprive the family of low-income status, and therefore the right to receive child benefits.

You can find out about all social support measures provided for low-income families (people living alone) in the ConsultantPlus system. Get a free online trial and go to the list.

It will not work to hide the presence of a bank deposit from the social security authorities. Since 2020, social security has been granted the right to receive information classified as tax secret from the tax service. This possibility is provided for in Art. 102 of the Tax Code of the Russian Federation and Law No. 68-FZ of March 26, 2020.

Also, banks have an obligation to report to the tax authorities data on interest accrued to individuals (Article 214.2 of the Tax Code of the Russian Federation).

Therefore, when applying for a benefit, social security will check information about an individual and their income. Concealment of information (not only information about interest, but also about other income) is fraught with: