Physician on FIRE has partnered with CardRatings for our coverage of credit card products. Physician on FIRE and CardRatings may receive a commission from card issuers. Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

How much money does a doctor need to retire and enjoy a typical “doctor retirement”?

Short answer: It depends.

Better answer: The number will vary from person to person depending on a wide variety of circumstances, but that shouldn’t stop us from coming up with an estimate for you.

Truthfully, the number doesn’t actually vary based on profession alone. A doctor has no inherently different retirement needs than anyone else. At the same time, it’s hard not to notice the fact that most doctors and other high-income individuals tend to spend more money than the average person, and thus will need more money to retire.

The variables that actually matter include current lifestyle, which influences your desired or anticipated spending in retirement, anticipated length of retirement, time to retirement, risk tolerance, ability or willingness to earn income in the future, and passive income streams including pensions and social security.

A number I’ve seen several times, including in this forum thread at the Student Doctor Network and another on the White Coat Investor Forum is $10 Million. I once had the $10 Million Dream myself.

$10 Million is a lot of money. Few physicians will ever be able to claim a net worth of $10 Million, let alone retirement savings of $10 Million. The vast majority of physicians will retire eventually with less than half of that.

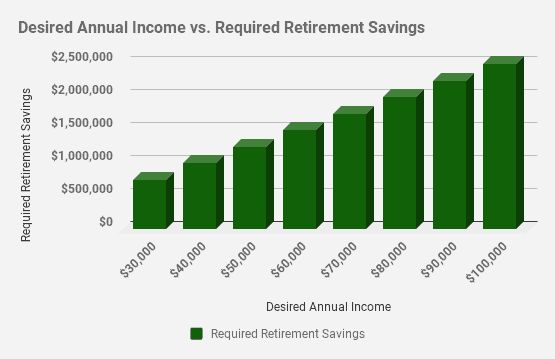

True, some physicians will need that much or more, but don’t assume because you heard that number somewhere that you’ll never be able to retire. Thousands of people retire every day with less than one million dollars in retirement assets, and many physicians can retire quite comfortably with retirement assets in a range of $2 Million to $5 Million in today’s dollars.

Thousands of people retire every day with less than one million dollars in retirement assets, and many physicians can retire quite comfortably with retirement assets in a range of $2 Million to $5 Million in today’s dollars.

What’s your number? Let’s examine the variables to come up with our best guesstimate.

What does your life look like today? What creature comforts have become customary? How much do you spend in a year? Are you determined to maintain your current lifestyle indefinitely or do you expect some current expenses to go away?

A good starting point is to track your spending. When I tracked mine for a few years, I used Personal Capital; others find You Need a Budget more useful. It’s difficult to come up with a target number if you have no idea how much money leaves your household each year.

When I first realized that I was financially independent, I wasn’t tracking our spending closely. However, I was keen on earning travel rewards in points and miles, so everything that could be paid by plastic was charged to

one rewards credit card or another.

However, I was keen on earning travel rewards in points and miles, so everything that could be paid by plastic was charged to

one rewards credit card or another.

Taking our average credit card bill and adding in the few checks that we wrote for property tax and piano lessons gave me an estimate of about $75,000 in annual spending.

The first twelve months of detailed expense tracking showed me that we spent $72,000 (without a mortgage — that was already paid off). You don’t necessarily need to track every dollar spent to get a decent idea of your annual spending. Spend a couple hours with your credit card and bank statements, and you should be able to come up with a good enough estimate.

Some cash back credit cards can offer substantial rewards with no annual fee. With its flat rewards rate of 1.5% on most purchases, and 3% back on restaurants and drugstore purchases, a household spending $72,000 on the Chase Freedom Unlimited

card could earn back $1,080 or more by the end of the year.

Pair it with a Sapphire Preferred card for at least $1,350 towards travel based on that spending, with an additional $1,250 in travel money after receiving the 100,000 point welcome bonus after a $4,000 spend in the first 3 months. That’s at least $2,600 in free travel the first year!

If you are keen on retiring early, or at least having the ability to do so, decide if there are line items that you could live without. Perhaps you could do your own lawn or pool maintenance. Cleaning services can also be optional.

Some crazy people (like me) live without cable or dish television. When you’ve pondered these ideas and perhaps come up with a few of your own, you’re ready to move to the next step.

Once you’ve determined about how much your household spends right now and what expenditures you could live without if necessary, you can estimate what your future spending needs might be.

Retirement life will not be the same. Any kids may be grown and out of the house. You may choose to downsize your home or move to a lower cost of living area. You’ll be able to drop disability and term life insurance.

Some expenses in retirement will go down or disappear completely, including the cost of commuting, professional clothing, and you will no longer be contributing to retirement accounts. I don’t consider doing so to be “spending,” but a substantial portion of my paychecks go there, so it’s worth mentioning.

Bear in mind that other costs can rise in retirement, including travel costs, gifts, education of yourself or family, and perhaps gifts as your kids have kids or you choose to be more charitable.

The elephant in the room is the cost of healthcare. People are budgeting anywhere from $5,000 to $50,000 a year for healthcare coverage. Strategies to keep expenses in check may include having taxable income low enough to qualify for a subsidy, purchasing a short-term or catastrophic plan when available penalty-free in 2019, joining a healthcare sharing ministry, or even obtaining citizenship in a foreign country.

I’m tentatively budgeting about $20,000 a year for healthcare expenses for our family of four, a quarter of our anticipated retirement expenses, but the true number may actually quite a bit higher or lower.

We’re going to need to know the year, and preferably the month, in which you plan to die. Cause of death is optional, but if you’d like to venture a guess, we’re all ears.

You don’t know? Well, then we’re going to have to consult an actuarial table, consider your habits, health, and family history, and make a wild guess.

It’s best to have a positive outlook and assume you’re going to live a long, healthy life. Not only does that attitude tend to be a self-fulfilling prophecy, but it’s also better to have your money outlast last you as opposed to you outliving your money.

I like to use estimates of living to 85 to 100 years of age. If you retire at 55, expect to be retired for 30 to 45 years. Retiring at 70? Expect another 15 to 30 years. Retiring exceptionally early at 43 as I did? Plan to fund the next 42 to 58 years!

Retiring at 70? Expect another 15 to 30 years. Retiring exceptionally early at 43 as I did? Plan to fund the next 42 to 58 years!

Why does it matter? Studies on withdrawal rates, including William Bengen’s study and the Trinity study, looked at retirement horizons of 30 years. Early Retirement Now’s extensive series looks at timeframes up to 60 years. The longer the retirement, the more variability you can expect to see in possible outcomes, and the more damaging particularly poor returns early in retirement can be.

If you’re looking at a retirement of 30 years or less, I think it’s reasonable to plan on initially spending 4% of your retirement assets and increasing your budget with inflation to maintain your current lifestyle thereafter.

A longer retirement may require a lower initial withdrawal rate or plans to either increase income or decrease spending if needed. And don’t ignore Social Security; it will be there in some form or another.

hawaii’s green sand beach

If you plan to retire within the next five years, you can probably get by with less than a $10 Million dollar nest egg. Probably a lot less. But if you’re a medical student today, and you plan to retire in 35 to 40 years, $10 Million may not be enough.

The obvious reason is inflation, which has averaged roughly 3% in the United States over many years. For the last decade or more, it was lower than that, but early in my lifetime, inflation ran rampant at a double-digit pace, and inflation seems to be ramping back up in 2021.

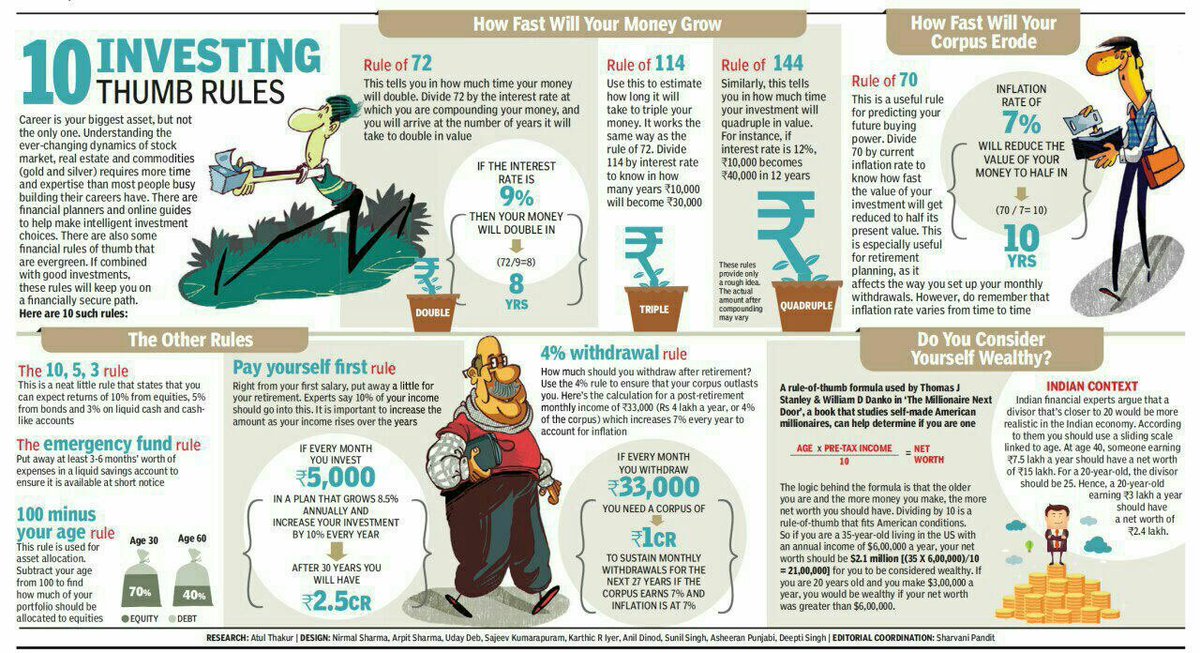

You can use the Rule of 72 (how long it takes money to double) to roughly determine how inflation could affect your target number.

With inflation of 2% (about where it is now), you will need twice as much money in 36 years as you do now in today’s dollars. If you want $3 Million in today’s dollars, you’ll want $6 million in 36 years if you expect inflation to remain low at about 2%.

Using the more typical 3% inflation, it will only take 24 years for your purchasing power to drop by half. If $5 Million in today’s dollars is your requirement, expect to accumulate $10 million to retire in 24 years.

What if inflation is above average in your working years? With 4% inflation, you’ll need twice as much in 18 years, and four times as much money to have the same purchasing power 36 years from now.

We hardly notice inflation from year to year, but your grandmother might remember when a candy bar went for a nickel and gasoline was pumped by the friendly attendant for 25 cents a gallon.

Please note that I am not referring to your preference for more risky investments like stocks or safer investments like short-term bonds. The risk tolerance I am talking about is how important is it to be extremely safe from running out of money by maintaining a steady lifestyle throughout retirement.

If your risk tolerance is low, you’ll sleep best with a nearly 100% chance of having your money last a lifetime. You’re willing to give up potentially larger returns for lower volatility. If this sounds like you, you’re probably better off with an initial withdrawal rate of 3 to 3.33%. This requires a nest egg totaling 30 to 33 times your anticipated annual spending in retirement.

If your risk tolerance is high, you could be happy with a projected success rate of greater than 50%. You probably have the ability to cut back on expenses or start earning an income if your portfolio sustains substantial damage in the early years of retirement.

Someone with a higher risk tolerance (and / or shorter retirement) could be good to go with an initial withdrawal rate of 4% or even 5%, requiring 20 to 25 years of annual expenses. FIRECalc is a great calculator to help determine the likelihood of your money lasting and visualizing the possible outcomes of your portfolio at various withdrawal rates.

You can plug in any numbers you like, and FIRECalc will give you all possible results looking at historical data. Starting with $2,000,000 and an initial withdrawal of $100,000 (5%) and increasing with inflation, you could end up as far as $11 Million in the hole, or have as much as $29 Million at the end of 50 years, with 48 of the 97 possibilities showing a positive balance at the end. The average ending position is $1.85 Million.

Your expenses can be covered by any combination of withdrawals from your nest egg, income from a pension or social security, or passive income from sources like ownership in rental properties, crowdfunded real estate, breweries, blogs, or other sources.

In the last few years, I’ve made quite a few real estate investments to increase my passive income in a very tax-efficient manner.

If your expenses are completely covered by steady and permanent income sources, any nest egg you’ve built up is pure gravy. With pensions becoming less common, and social security unlikely to cover 100% of your desired spending level, such a setup is most likely to come from ownership in small business and physical real estate.

With pensions becoming less common, and social security unlikely to cover 100% of your desired spending level, such a setup is most likely to come from ownership in small business and physical real estate.

Most retirees will have a portion of their expenses covered by a steady income source. Early retirees tend to ignore the contribution of social security, but for the more traditional retiree, it may very well cover a portion of your annual spending, and that can lower your required nest egg substantially.

For example, if Social Security pays a couple $35,000 a year, and they live on $70,000 a year, then they only need a multiple of the remaining $35,000 to pay for what Social Security doesn’t cover. With a 3.33% withdrawal rate, that would equal 30 x $35,000 or a $1.05 Million dollar nest egg to give the couple a very good likelihood of their money lasting the rest of their lives if they start taking Social Security at retirement.

You can make a similar calculation by determining how much will be covered by pensions or passive income streams. The less steady or guaranteed those income streams are, the less certain you can be about the viability, and the more you should plan on saving.

The less steady or guaranteed those income streams are, the less certain you can be about the viability, and the more you should plan on saving.

When it comes to the future, there’s no such thing as a sure thing, but the research on withdrawal rates is impressively thorough, and the bar of 3% to 4% per year is based on a very unfavorable set of circumstances.

In fact, based on data analyzed my Michael Kitces, a 5% or 6% rule would have worked in many prior years to make your money last 30 years or more. The median outcome, using an initial 4% withdrawal rate (and increasing withdrawals with inflation), is to have about 2.8 times as much money after 30 years compared to what you started with.

Is the very worst possible scenario factored in? Not exactly, but if we experience something far worse than the Great Recession or Great Depression, paper money or your Vanguard balance might not mean much, anyway.

Related: Who Are the Physicians Who Retire Early?

To come up with a ballpark figure, use your current rate of spending to guesstimate your future retirement spending needs, accounting for inflation, of course. Reduce your requirement by the value of future income streams.

Reduce your requirement by the value of future income streams.

Determine a safe withdrawal rate that will make you comfortable. I recommend a number in the 3% to 3.5% range (requiring about 28 to 33 years worth of expenses) if some of these apply to you:

You could use an initial withdrawal rate of 4% to 5% (requiring 20 to 25 years of expenses) if you meet some of these criteria:

You should now have all the information you need to have a rough estimate of your financial independence target — the amount you should aim for to retire without much worry.

Simply multiply how much money you’ll need for your anticipated retirement expenses by a number in the range of 20 to 33 after accounting for any portion covered by truly passive income.

You’ve got your number! Now, let’s see what you can do to get there.

A generous welcome bonus of 60,000 points & Peloton membership credits onthe Chase Sapphire Preferred & premium card perks with the Chase Sapphire Reserve!

60,000 Points good for $750 in travel or more with a $4,000 spend in 3 months

The Chase Sapphire Preferred is an excellent first (or only) rewards card. $50 annual hotel credit for bookings via the Chase UR tavel portal & 5x points for all travel via the portal. 3x points on dining, 2x on other travel. Flexible rewards good for cash, travel, or transfer to travel partners, great travel protection & new Peloton, Lyft & DoorDash perks! $95 Annual Fee

80,000 Points with a $4,000 spend in 3 months

The Chase Sapphire Reserve offers great travel perks including Priority Pass lounge access, a credit for Global Entry or TSA Pre✓ and a $300 annual travel credit. When using Chase Ultimate Rewards travel portal, get 10x points on hotels and car rental & 5x points on flights. 3x points on other travel & dining. Elevated Peloton, Lyft and DoorDash benefits. $550 Annual Fee

When using Chase Ultimate Rewards travel portal, get 10x points on hotels and car rental & 5x points on flights. 3x points on other travel & dining. Elevated Peloton, Lyft and DoorDash benefits. $550 Annual Fee

What’s your number? At what age do you think you could achieve it?

Do you anticipate retiring then or will you continue to work to leave a legacy, for the benefit or charity, or simply because you love your job?

Physician on FIRE has partnered with CardRatings for our coverage of credit card products. Physician on FIRE and CardRatings may receive a commission from card issuers.

Some doctors are excellent accumulators of wealth. Once you have your accumulation plan in place, it might be time to consider some cultivated issues in retirement planning for doctors. And what is the average net worth of physicians at Retirement? Doctors are a heterogeneous lot; this much is true. However, those who wear the white coat face some common issues in retirement. Let’s review the epidemiology of doctor retirement and net worth and then go over some common problems in retirement planning for doctors. Once you are done here, check out The Retirement Checklist for Physicians.

Once you have your accumulation plan in place, it might be time to consider some cultivated issues in retirement planning for doctors. And what is the average net worth of physicians at Retirement? Doctors are a heterogeneous lot; this much is true. However, those who wear the white coat face some common issues in retirement. Let’s review the epidemiology of doctor retirement and net worth and then go over some common problems in retirement planning for doctors. Once you are done here, check out The Retirement Checklist for Physicians.

Figure 1 (Doctor Retirement by Age)

Source Figure 1 shows doctor retirement by age. Surprisingly, 58% of doctors retire after the age of 65! However, in the US general population, women retire at age 60-62 and men 62-64. Do doctors retire later on average because of the late start we get after a decade of training?

What does a metanalysis say as to why doctors retire? According to this study, doctors do indeed retire later than average. Reasons to quit early include: low job satisfaction, medicolegal issues, health concerns, and financial troubles. Reasons to delay retirement include career satisfaction, institutional flexibility, feeling responsible for patients, economic reasons, and a lack of interest outside of medicine. Finances show up on both sides—retire early and delay retirement. What are these financial concerns? Net worth is one of them.

Reasons to quit early include: low job satisfaction, medicolegal issues, health concerns, and financial troubles. Reasons to delay retirement include career satisfaction, institutional flexibility, feeling responsible for patients, economic reasons, and a lack of interest outside of medicine. Finances show up on both sides—retire early and delay retirement. What are these financial concerns? Net worth is one of them.

Let’s look at Doctors’ average net worth by age.

Figure 2 (Doctor Net Worth by Age)

Maybe you’ve seen the data in Figure 2 before. While you can easily retire with less than $5M, especially when you are traditional retirement age, look at the purple bar (net worth> $5M) increase with age. It goes from 3% up to 22%. So, about 1 in 5 doctors over 70 have a net worth greater than $5M. As I said, moderately depressing. Retirement planning for doctors should be easy given the high incomes during their career. However, the $1-5M percentage doesn’t change much with age. Sadly, 25% of doctors older than 65 never have a nest egg larger than $1M. For a more detailed analysis, let’s dive into the Medscape Physician Net Worth 2020 data.

However, the $1-5M percentage doesn’t change much with age. Sadly, 25% of doctors older than 65 never have a nest egg larger than $1M. For a more detailed analysis, let’s dive into the Medscape Physician Net Worth 2020 data.

First stop for you: check out the Salary Explorer to see how you compare to your peers. Do you make the same as others in your area with the same expertise? Interesting, yes? I took a pay cut when I started my specialty after being a hospitalist again, so at least for us internal medicine docs, it is interesting to note who earns less than the hospitalists. There probably is a fellowship for hospitalists by now, but in my days, that fellowship was servitude through residency. It looks like endocrine and ID make less than hospitalists—a negative return for fellowship. Let’s move on.

The Young Physicians Compensation Report 2020 is always interesting. This is a subset analysis for physicians less than 40 vs. those of us who are past our prime. Above, you can see how much young vs. “old” physicians earn—PCPs on the Left, Specialists on the Right. A funny story, someone asked me how long it took me to make a complicated diagnosis that had challenged the primary team. I said, “15 minutes and 15 years.” I’m not sure where you all fall on the experience vs. recent education spectrum, but you can see the difference in a small community hospital. I am one of the older folks, and I practice medicine by scanning a patient’s aura and knowing the diagnosis, then looking for details to support my conclusion. Of course, you then look for dangerous and/or common things that must not be missed. What do recent autopsy studies say about how often the diagnosis is incorrect by clinician age? I wound if that study has been done by age. That is a rare digression from finance into diagnostic acumen via the “aura scanner” you get with age. It took 15 minutes and 15 years to figure that one out.

This is a subset analysis for physicians less than 40 vs. those of us who are past our prime. Above, you can see how much young vs. “old” physicians earn—PCPs on the Left, Specialists on the Right. A funny story, someone asked me how long it took me to make a complicated diagnosis that had challenged the primary team. I said, “15 minutes and 15 years.” I’m not sure where you all fall on the experience vs. recent education spectrum, but you can see the difference in a small community hospital. I am one of the older folks, and I practice medicine by scanning a patient’s aura and knowing the diagnosis, then looking for details to support my conclusion. Of course, you then look for dangerous and/or common things that must not be missed. What do recent autopsy studies say about how often the diagnosis is incorrect by clinician age? I wound if that study has been done by age. That is a rare digression from finance into diagnostic acumen via the “aura scanner” you get with age. It took 15 minutes and 15 years to figure that one out. A fundamental question: Would you choose medicine again? I thought it surprising that 76% said yes, which didn’t change depending on age.

A fundamental question: Would you choose medicine again? I thought it surprising that 76% said yes, which didn’t change depending on age.

And on to the Physician Net Worth Report 2020. Let’s take a look at high-net-worth physicians. See this report from 2019 and 2020 (if there is a paywall from the link, google the words, and you should be able to see the advertisement-filled slide show). Interestingly, this was the wealth and debt report in 2019 and the debt and net worth report in 2020. So wealth was demoted and changed to net worth this year. Debt was promoted. Hmm. Anyway, let’s dig in!

Somewhere between 1 and 19% of your colleagues are worth more than $5M depending on your specialty. I am disappointed in these numbers, but I have been year after year. Some specialties are lower than they should be, too, depending on income.

Conversely, 20-50% of your colleges have made almost no progress in building a nest egg. This may be because they are young, but check out a few of your favorites and see the difference between the top and the bottom specialties.

This may be because they are young, but check out a few of your favorites and see the difference between the top and the bottom specialties.

This is interesting as well. More than 60% of physicians have a mortgage. Yet, amazingly, almost 40% have a car loan. Honestly, car loans? But since 25% have credit card debt, we need to remember that doctors are people too, and financial illiteracy knows no bounds. Only 11% had no expenses or debts.

So, who has the doctor’s McMansion? The glamour specialties have larger homes, and those poorly-paid specialties have smaller houses.

Who still owes a large amount on their McMansion? Again, pick your favorite specialties and see the difference in the size of the home and how many still have large mortgages.

Doximity releases a compensation report as well. Of interest here are metro areas with the highest and lowest compensation for physicians. There is only a 15% difference between the highest and lowest metro area, so location may not be a game-changer from the income perspective. However, it would be interesting to see these locations with income over the cost of living for the metro areas… There is also some interesting information on wage growth and the gender gap.

Of interest here are metro areas with the highest and lowest compensation for physicians. There is only a 15% difference between the highest and lowest metro area, so location may not be a game-changer from the income perspective. However, it would be interesting to see these locations with income over the cost of living for the metro areas… There is also some interesting information on wage growth and the gender gap.

In summary, voyeurism is always fun. It is nice for some of us to look in and see how little we are earning and how big other people’s homes are. But don’t forget, their mortgage is larger than yours. Only 10% of physicians have a net worth greater than $5M. While it is clear you don’t really “need” any particular number, the fact is that physicians make a lot of money. It is a shame if they make a lot of money and haven’t put away all that much.

So, on average, doctors retire later than the general population yet with more financial resources. Still, given doctors’ high incomes, it is depressing that so many of our colleagues are not better prepared for retirement. Financial concerns are cited as reasons to retire early and retire late. Let’s move on now. I assume anyone who is reading this is doing well for themselves. What are some issues that impact planning for doctors in their retirement?

Still, given doctors’ high incomes, it is depressing that so many of our colleagues are not better prepared for retirement. Financial concerns are cited as reasons to retire early and retire late. Let’s move on now. I assume anyone who is reading this is doing well for themselves. What are some issues that impact planning for doctors in their retirement?

Everyone needs to consider what they plan to do in retirement. Many doctors find more than a mere calling in medicine. Letting go of the title of “Doctor” is difficult. However, finding purpose in retirement is necessary to ensure health and sanity. I recently decided on my retirement date, and purpose is a huge concern. It will be interesting to see trends in doctor retirement in the next decade, given the industrialization of medicine and the loss of autonomy many doctors face. Encore careers are common for doctors. Remember that Parkinson’s law applies to retirement as well! When doing retirement planning for doctors, I focus on the financial aspects. But none of that matters without purpose!

But none of that matters without purpose!

From poor distribution options on Non-Governmental 457 plans to liquidating investments in practices, equipment, or real estate, many doctors will face liquidity events. A liquidity event happens when you must recognize a bolus of ordinary or capital gain income in one year. Of course, ideally, you would be able to take a better distribution option on your 457 or spread out your payout for your share of the practice or investment over two or more tax years. Some planning is possible if you are forced to “suffer” a liquidity event. Tax planning is essential that year, perhaps to reduce your other sources of income or find a way to take a significant tax deduction in the same year. Other possibilities include Oil and Gas, Opportunity Zone Investments, Real Estate depreciation through cost segregation, bonus depreciation, etc. None of these are great options, by the way—plan at least a year in advance with your CPA.

Many doctors have large 401k or 403b accounts and face huge future tax burdens as Required Minimum Distributions force out this deferred income. These 401k Millionaires have the opportunity to do some tax planning during the Tax Planning Window, which may include partial Roth conversions. Then, after you retire and before you start social security and RMDs, you have the chance to control your income. This Tax Planning Window is the most significant opportunity to own your future tax liability and should not be squandered.

These 401k Millionaires have the opportunity to do some tax planning during the Tax Planning Window, which may include partial Roth conversions. Then, after you retire and before you start social security and RMDs, you have the chance to control your income. This Tax Planning Window is the most significant opportunity to own your future tax liability and should not be squandered.

White Coat Investor not infrequently calls retirement planning issues “first world problems.” Given his gift for tax efficiency, while practicing and running a burgeoning business, I expect he will change his tune when he considers retirement and sees how much he will pay in taxes during his retirement! Taxes can be a doctor’s most significant expense while practicing and retiring. It pays to be tax efficient. After all, every dollar you save is another dollar you can send or give to heirs or charity. Aside from partial Roth conversions, there are other tax-efficient withdrawal strategies. These include:

These include:

Since the Tax Cut and Jobs Act, most have used the standard deduction and no longer get tax deductions for our charitable gifts. Not that a tax deduction is the only reason to give, but if you can find a way to give tax-efficiently, you can give more! If you have charitable intent, there are many considerations. These include:

Leaving a legacy is important as many doctors will have more money than time. The loss of the Stretch IRA has engendered some new retirement planning strategies. Unfortunately, none are as good as the Stretch IRA. Read about the new 10-year rule and your retirement accounts. Cascading beneficiaries, disclaimer planning, multi-generation spray trusts, Roth conversions, Life Insurance, and Charitable Remainder Trusts are all considerations when planning your legacy.

The loss of the Stretch IRA has engendered some new retirement planning strategies. Unfortunately, none are as good as the Stretch IRA. Read about the new 10-year rule and your retirement accounts. Cascading beneficiaries, disclaimer planning, multi-generation spray trusts, Roth conversions, Life Insurance, and Charitable Remainder Trusts are all considerations when planning your legacy.

Since we have all seen the ravages of age, Long-Term Care Insurance is a difficulty in the back of our minds. While many retired doctors can self-fund long-term care needs, there is a shortage of insurance options if you want to transfer the risk of a sizeable Long-Term Care event. Traditional Long-Term Care Insurance suffers from issues of premium increases and future solvency. So-called hybrid LTC/Life Insurance policies are becoming more popular but have copious downsides. One point I cannot get the insurance industry to understand about these policies is that you are often better off NOT TO USE one once you have it. This is because medical expenses are a tax deduction above an AGI floor. You can withdraw pre-tax money tax-free if you have a significant enough deductible Long-Term Care event. So, if your goal is leaving money behind for your heirs, you are better off withdrawing pre-tax money tax-free to pay for healthcare costs and letting the tax-free death benefit of the policy go to your heirs. Or not having a hybrid policy in the first place! Long Term Care considerations are the most intractable problem in retirement planning today. They can have truly devastating costs, but insurance is priced to cover non-devastating events. Imagine how expensive home insurance would be if we all had small or moderate fires in our house, at least at some point in our lives! Insurance is best saved for risk pooling of catastrophic events, which is not how Long-Term Care insurance operates currently.

This is because medical expenses are a tax deduction above an AGI floor. You can withdraw pre-tax money tax-free if you have a significant enough deductible Long-Term Care event. So, if your goal is leaving money behind for your heirs, you are better off withdrawing pre-tax money tax-free to pay for healthcare costs and letting the tax-free death benefit of the policy go to your heirs. Or not having a hybrid policy in the first place! Long Term Care considerations are the most intractable problem in retirement planning today. They can have truly devastating costs, but insurance is priced to cover non-devastating events. Imagine how expensive home insurance would be if we all had small or moderate fires in our house, at least at some point in our lives! Insurance is best saved for risk pooling of catastrophic events, which is not how Long-Term Care insurance operates currently.

Social Security maximization should be something that all doctors are familiar with. If you have done well and have a reasonable life span, consider delaying social security to take advantage of delayed retirement credits. Perhaps, social security is the best longevity insurance out there, with inflation adjustment and a government-backed guarantee. Most doctors should assume that 85% of their social security will be included with their taxable income, as the brackets for taxation of social security are absurdly low and haven’t been inflation-adjusted since Regan.

If you have done well and have a reasonable life span, consider delaying social security to take advantage of delayed retirement credits. Perhaps, social security is the best longevity insurance out there, with inflation adjustment and a government-backed guarantee. Most doctors should assume that 85% of their social security will be included with their taxable income, as the brackets for taxation of social security are absurdly low and haven’t been inflation-adjusted since Regan.

This is, perhaps, the most exciting retirement planning puzzle. Many doctors have been suckered into bad investments or products by “financial advisors.” Unwinding these takes care, consideration, and patience. If you have an insurance salesman masquerading as a financial advisor, you might own expensive annuities or unnecessary permanent life insurance products. Unwinding these might involve liquidation and some “stupid tax.” There are other important considerations, though. If you need income in retirement from annuities, you may consider annuitizing the policy or using the Income Rider you have been paying for all these years. Or, you could 1035 into an Investment Only Variable Annuity depending on the goal of the funds. I’ve found that most folks who have been sold an annuity don’t understand “why” they own the annuity and what purpose it is supposed to serve in the future. With Permanent Life Insurance, you may consider a 1035 into a hybrid LTC policy if you want long-term care insurance. Understanding the indication for owning a Permanent Life Insurance policy is critical. If your financial advisor is a stock picker, then you might have individual stocks or crazy expensive mutual funds with a low basis. Unloading these will involve paying capital gains taxes. Many doctors will remain in the 18.8% capital gain tax bracket on future projections, so a decision must be made regarding the purpose of the money. If you plan to unwind it at some point due to the tax inefficiencies of the funds, earlier is better as it allows you to reset your basis and choose funds more in line with your goals and chosen asset allocation.

If you need income in retirement from annuities, you may consider annuitizing the policy or using the Income Rider you have been paying for all these years. Or, you could 1035 into an Investment Only Variable Annuity depending on the goal of the funds. I’ve found that most folks who have been sold an annuity don’t understand “why” they own the annuity and what purpose it is supposed to serve in the future. With Permanent Life Insurance, you may consider a 1035 into a hybrid LTC policy if you want long-term care insurance. Understanding the indication for owning a Permanent Life Insurance policy is critical. If your financial advisor is a stock picker, then you might have individual stocks or crazy expensive mutual funds with a low basis. Unloading these will involve paying capital gains taxes. Many doctors will remain in the 18.8% capital gain tax bracket on future projections, so a decision must be made regarding the purpose of the money. If you plan to unwind it at some point due to the tax inefficiencies of the funds, earlier is better as it allows you to reset your basis and choose funds more in line with your goals and chosen asset allocation. These low-basis bad investments are perfect for giving away if you have a donor-advised fund or bunch deductions.

These low-basis bad investments are perfect for giving away if you have a donor-advised fund or bunch deductions.

Retirement Planning seems backward after being in the accumulation mindset. Instead of growing your wealth, you need to consider spending some of it down! Additional pitfalls, retirement risks, and traps in retirement take some planning. Many of these issues uniquely affect doctors and other high-income professionals. A forward-facing 20-30-year tax plan is often helpful to see what your tax bracket “number” will be. For instance, if you know that RMDs will expose much of your retirement income to the 25% federal tax bracket in the future, use all your tax brackets below the 24% bracket now! A percent or two doesn’t seem like it would make much difference, but if you can rescue money from a pre-tax account and convert it into a Roth, all future growth is tax-free. The goal, of course, is not to perfectly predict how much you will be paying in taxes even five or ten years from now. Everything can and will change, and many assumptions will be wrong! The goal, instead, is to optimize the next 1-3 years, so you set yourself up in the best possible position to roll with the punches as they come, all while efficiently funding retirement.

Everything can and will change, and many assumptions will be wrong! The goal, instead, is to optimize the next 1-3 years, so you set yourself up in the best possible position to roll with the punches as they come, all while efficiently funding retirement.

Posted in Retirement and tagged Doctor Retirement, Retirement Planning for Doctors.

Elena Bibikova © Igor Samokhvalov/PG

Since the beginning of this year, the requirements for granting old-age insurance pensions have changed. Elena Bibikova, Deputy Chairman of the Federation Council Committee on Social Policy , told the press center of Parliamentary Newspaper what conditions must be met in order to retire on a well-deserved rest.0009 .

- Elena Vasilievna, the transitional period continues, associated with an increase in the retirement age, which gives the right to receive an insurance pension. What are the conditions for granting a pension this year?

What are the conditions for granting a pension this year?

- To assign an old-age pension, three conditions must be met: reaching retirement age, having an insurance period and the required number of pension coefficients. This year, women born in the second half of the year 19 can retire65 years old, and men born in the second half of 1960 - for them the retirement age is increased by 1.5 years. And they will be granted pensions in the first half of 2022. The next category is the year of birth of a woman in 1966 and the year of birth of a man in 1961, they will have an increase in age of three years. That is, women will be able to retire at 58, men at 63. And it will be in 2024.

Also, a prerequisite for the appointment of a pension is the presence of the necessary length of service. Starting from 2024, the total length of service required for granting a pension will be 15 years. This year there is still a transitional period and the required length of service is 13 years. I will clarify which periods are taken into account when determining the length of service.

I will clarify which periods are taken into account when determining the length of service.

Until 2002, these are all periods of work that are documented, for example, an entry in a work book or a certificate of work. Since 2002, confirmation of the very fact of work is not enough; after that, only those periods of labor activity for which insurance premiums were paid to the Pension Fund are included in the length of service for assigning a pension. In addition to the labor (insurance) experience, to determine the right to a pension, non-insurance periods are included, such as military service, time to care for a child up to 1.5 years old, time to care for the elderly, time to care for disabled people of group I, time when a person is not worked, but was in the employment service, and some other periods determined by law.

With regard to pension coefficients, this year they require 23.4 to assign a pension. You can determine whether you managed to collect them or not as follows: insurance premiums from the minimum wage amount to approximately one pension coefficient per year. That is, if a person receives a salary of three minimum wages and insurance premiums are transferred from this salary, then a person earns three coefficients per year. If he receives a high salary of 10 or more minimum wages, then 10 coefficients are charged for this year. It is better to check the exact number of coefficients collected in the Pension Fund.

That is, if a person receives a salary of three minimum wages and insurance premiums are transferred from this salary, then a person earns three coefficients per year. If he receives a high salary of 10 or more minimum wages, then 10 coefficients are charged for this year. It is better to check the exact number of coefficients collected in the Pension Fund.

- But there are still some categories of employees who are entitled to early retirement.

- Yes, there are categories of citizens for whom the conditions of retirement have not been changed during the pension reform. This applies to people who work in harmful and difficult working conditions and for whom the employer pays higher rates of insurance premiums.

List No. 1 includes particularly hazardous industries - for example, underground work, chemical production, work with radioactive substances.

List No. 2 includes professions with difficult working conditions. These are, in particular, subway drivers, bus drivers. For them, the conditions for retirement are preserved. According to the first list, men both retired and retire at 50, women at 45. At the same time, the required work experience for men is 20 years, of which at least 10 in hazardous work, for women - 15 years, at least 7.5 years in hazardous work. For the second list, the norm has been retained, according to which men, as before, retire at 55 years old, women at 50 years old, if they have 25/20 years of experience, respectively, men / women, of which at least half should work in hazardous and difficult conditions.

For them, the conditions for retirement are preserved. According to the first list, men both retired and retire at 50, women at 45. At the same time, the required work experience for men is 20 years, of which at least 10 in hazardous work, for women - 15 years, at least 7.5 years in hazardous work. For the second list, the norm has been retained, according to which men, as before, retire at 55 years old, women at 50 years old, if they have 25/20 years of experience, respectively, men / women, of which at least half should work in hazardous and difficult conditions.

© Kirill Zykov/AGN Moscow

The provisions on early retirement on so-called social grounds have been retained. This applies, for example, to women who have given birth and raised five or more children up to the age of eight. With 15 years of service, they can retire at 50. The same rule applies to one of the parents who raised a disabled child up to the age of eight.

Retirement benefits remained with doctors and teachers, but the conditions for this have changed somewhat. They can still retire regardless of age if they have 25 years of service in these positions. However, in 2022, the very appointment of a pension will be “pushed back” by four years from the date when they have worked for 25 years. In 2023, it will be plus five years.

They can still retire regardless of age if they have 25 years of service in these positions. However, in 2022, the very appointment of a pension will be “pushed back” by four years from the date when they have worked for 25 years. In 2023, it will be plus five years.

Also, since 2019, new preferential categories of pension recipients and those who are entitled to early retirement have appeared. First of all, these are men who have a long work experience of 42 years, and women who have worked for 37 years. They have the right to retire two years earlier than the generally established age, but not earlier than 60 and 55 years respectively. Also, since 2019, a benefit has been introduced for mothers with many children. If a woman has given birth and raised four or more children before the age of eight, the retirement age for her is reduced by four years from the generally established one, but not earlier than 55 years. For a woman who has given birth to three or more children, the retirement age is reduced by three years from the generally established one, but again, she will be able to take a well-deserved rest no earlier than at the age of 55. A prerequisite for this is the presence of at least 15 years of experience.

A prerequisite for this is the presence of at least 15 years of experience.

- What should I do if there is not enough work experience or coefficients to assign a pension?

- The first thing to start with is to verify your experience. It happens that some periods of labor activity are not entered in the work book, there are no other supporting documents, that is, a person knows that he worked somewhere, but this is not confirmed. It is necessary to request relevant documents from enterprises either directly or through the Pension Fund authorities. You also need to see if the time spent caring for a child is included in the insurance period. Let me remind you that it can be included in the experience not only for mom, but also for dad. That is, if the mother has enough experience without taking into account the time of caring for the child, then these periods can be credited to the father. To do this, you need to submit information about the children who are in the family to the Pension Fund authorities. There is an option to modify either the length of service or pension coefficients. If this option is not suitable, you can join the voluntary pension insurance system, in other words, acquire experience and coefficients by making contributions to the pension system. This must be done by writing a corresponding application either at the Pension Fund, or through the public services portal, or through the MFC. Details should be clarified with the Pension Fund.

There is an option to modify either the length of service or pension coefficients. If this option is not suitable, you can join the voluntary pension insurance system, in other words, acquire experience and coefficients by making contributions to the pension system. This must be done by writing a corresponding application either at the Pension Fund, or through the public services portal, or through the MFC. Details should be clarified with the Pension Fund.

If a person was unable to work due to his health condition, you can contact the doctors to determine the disability group. The last option, if a person has not worked all his life, there is no work experience, in this case, a social old-age pension should be expected. She will be appointed five years later than the generally established retirement age, and she is not paid during the period of work.

In medical law, in addition to regulating the relationship between doctors and patients, there are subsections that provide a medical worker with appropriate working conditions and social guarantees. These include the calculation of pensions for medical workers. To date, there are questions about the rules for calculating pensions, in connection with which we turned to the territorial pension fund. Our questions were answered by Lena Alexandrovna Nogovitsyna, Deputy Head of the Department for Establishing Pensions of the PFR Branch for the Republic of Sakha (Yakutia).

These include the calculation of pensions for medical workers. To date, there are questions about the rules for calculating pensions, in connection with which we turned to the territorial pension fund. Our questions were answered by Lena Alexandrovna Nogovitsyna, Deputy Head of the Department for Establishing Pensions of the PFR Branch for the Republic of Sakha (Yakutia).

Pension is a monthly cash payment in order to compensate persons for wages and other payments and remunerations lost by them in connection with the onset of incapacity for work due to old age or disability, and for disabled family members of wages and other payments and remunerations of the breadwinner lost due to with his death.

What is a preferential pension for medical workers?

For medical workers, a preferential retirement procedure is provided - early retirement and a preferential procedure for calculating the length of service. The right to early registration of a pension for health workers does not directly depend on the age and number of years of the total insurance experience, because. the right is determined only by the date of development of the length of service provided for by law. For medical workers in certain positions who have worked out a special work experience in harmful or difficult working conditions, as well as insurance experience, a pension can be assigned to them upon reaching a certain age, previously generally established.

the right is determined only by the date of development of the length of service provided for by law. For medical workers in certain positions who have worked out a special work experience in harmful or difficult working conditions, as well as insurance experience, a pension can be assigned to them upon reaching a certain age, previously generally established.

How are pension payments determined?

The main factors affecting the size of the pension are: salary, length of insurance period, age of applying for a pension, insurance premiums that the employer charges for each of his employees, as well as work or residence in the Far North or in areas equated to the Far North (the fixed payment, which is paid to pensions, is higher in these areas).

What should be the actual work experience of a health worker?

Medical work experience in accordance with paragraph 20, part 1 of article 30 of the Federal Law of December 28, 2013 No. 400-FZ “On insurance pensions” is: 25 years - in rural areas or urban-type settlements; 30 years - mixed experience (in cities, rural areas and urban settlements) or only in cities.

400-FZ “On insurance pensions” is: 25 years - in rural areas or urban-type settlements; 30 years - mixed experience (in cities, rural areas and urban settlements) or only in cities.

Has the retirement age changed for medical workers?

The medical worker does not have a pensionable age. At the same time, the minimum required medical experience for granting a pension does not increase and, depending on the specific profession, as before, ranges from 25 to 30 years.

At the same time, starting from 2019, the retirement of medical workers is determined taking into account the transition period for raising the retirement age. In accordance with it, the appointment of a pension for medical workers is gradually postponed from the moment the special experience is developed. At the same time, they can continue their labor activity after acquiring the required length of service or stop working. For example: if a rural doctor completed the required length of service in September 2021, then a pension will be assigned to him in accordance with the generally established transitional period for raising the retirement age - after 3 years, that is, in September 2024.

Conditions for early retirement of a healthcare worker?

A prerequisite is the acquisition of special experience of the required duration.

Is it better to retire based on seniority or age? Give, please, an example in which cases it is better and worse.

From 01.01.2002 the concept of "long service" pensions disappeared, these pensions are considered as early old-age pensions. Accordingly, the amount of a pension for citizens who have a long medical record of work in a certain position (length of service) is determined according to the general norms for calculating the amount of an old-age pension in accordance with Federal Law No. 400-FZ of December 28, 2013 “On Insurance Pensions”.

Do maternity leave and parental leave count as work experience?

Maternity leave is included both in the insurance period of a medical worker and in the special medical period, regardless of the period of granting the specified leave.

With regard to parental leave periods up to 1.5 (3 years), these leaves are included in the medical experience if they were granted to the employee before 10/06/1992.

What changes have occurred in the calculation of pensions and in what direction?

There have been no changes in the procedure for determining the amount of old-age pensions in the last 6 years.

What mistakes are made when calculating pensions?

The decision to assign a pension is made in strict accordance with the current pension legislation (Federal Law of December 28, 2013 No. 400-FZ "On insurance pensions"), errors are unacceptable.

How are conflicts resolved in case of disagreements with pension experience? Give a specific example.

If the applicant disagrees with the established amount of the pension, or with a refusal to assign an early old-age insurance pension to a medical worker, a citizen has the right to appeal the decision to a higher pension authority, or in court.