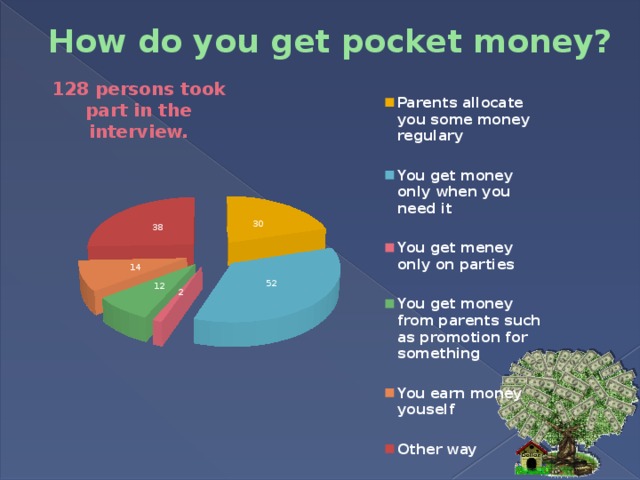

Learn more about our 4 key retirement metrics—a yearly savings rate, a savings factor, an income replacement rate, and a potentially sustainable withdrawal rate—and how they work together in the Viewpoints Special Report: Retirement roadmap.

close

View Larger Image

Who doesn't have a retirement dream? Yours may be as simple as sleeping late or riding your bike on a sunny afternoon, or as daring as jumping out of a plane at age 90. Living your retirement dream the way you want means saving now—and saving enough so you don't have to worry about money in retirement.

Our guideline: Aim to save at least 15% of your pre-tax income1 each year, which includes any employer match. That's assuming you save for retirement from age 25 to age 67. Together with other steps, that should help ensure you have enough income to maintain your current lifestyle in retirement.

How did we come up with 15%? First, we had to understand how much people generally spend in retirement. After analyzing enormous amounts of national spending data, we concluded that most people will need somewhere between 55% and 80% of their preretirement income to maintain their lifestyle in retirement.1

Not all of that money will need to come from your savings, however. Some will likely come from Social Security. So, we did the math and found that most people will need to generate about 45% of their retirement income (before taxes) from savings. Based on our estimates, saving 15% each year from age 25 to 67 should get you there. If you are lucky enough to have a pension, your target savings rate may be lower.

Some will likely come from Social Security. So, we did the math and found that most people will need to generate about 45% of their retirement income (before taxes) from savings. Based on our estimates, saving 15% each year from age 25 to 67 should get you there. If you are lucky enough to have a pension, your target savings rate may be lower.

Here's a hypothetical example. Consider Joanna, age 25, who earns $54,000 a year. We assume her income grows 1.5% a year (after inflation) to about $100,000 by the time she is 67 and ready to retire. To maintain her preretirement lifestyle throughout retirement, we estimate that about $45,000 each year (adjusted for inflation), or 45% of her $100,000 preretirement income, needs to come from her savings. (The remainder would come from Social Security.)

Consider Joanna, age 25, who earns $54,000 a year. We assume her income grows 1.5% a year (after inflation) to about $100,000 by the time she is 67 and ready to retire. To maintain her preretirement lifestyle throughout retirement, we estimate that about $45,000 each year (adjusted for inflation), or 45% of her $100,000 preretirement income, needs to come from her savings. (The remainder would come from Social Security.)

Because she takes advantage of her employer's 5% dollar-for-dollar match on her 401(k) contributions, she needs to save 10% of her income each year, starting with $5,400 this year, which gets her to 15% of her current income.

That depends, of course, on the choices you make before retirement—most importantly, when you start saving and when you retire. Any other income sources you may have, such as a pension, should also be considered.

Now that you know a savings rate to consider, here are some steps to think about that can help you get to it.

The single most important thing you can do is start saving early. The earlier you start, the more time you have for your investments to grow—and recover from the market's inevitable downturns.

If retirement is decades away, it may be hard to think or care about it. But when you are young is precisely the time to start saving for retirement. Even though it can be a challenge to save for the future, giving your savings those extra years to grow could make the struggle worth it—every little bit you can save helps.

Assumes no retirement savings balance before starting age. See footnote numbers 2 and 3 below for more information.

See footnote numbers 2 and 3 below for more information.

Our 15% savings guideline assumes that a person retires at age 67, which is when most people will be eligible for full Social Security benefits. If you don't plan to work that long, you will likely need to save more than 15% a year. If you plan to work longer, all things being equal, your required saving rate could be lower.

The road to retirement is a journey, and there are steps you can take along the way to catch up. Here are 6 tips to get started:

Plus, that money can grow tax-free until you withdraw it in retirement, when it will be taxed as ordinary income. With Roth 401(k)s and IRAs, your contributions are after tax, but you can withdraw the money tax-free in retirement—assuming certain conditions are met.4

Plus, that money can grow tax-free until you withdraw it in retirement, when it will be taxed as ordinary income. With Roth 401(k)s and IRAs, your contributions are after tax, but you can withdraw the money tax-free in retirement—assuming certain conditions are met.4If you have a high deductible health plan (HDHP) eligible for a health savings account (HSA), consider contributing to an HSA to cover current and future health care expenses. HSA contributions are pre-tax and tax-deductible. Plus, when you use money saved in an HSA on qualified medical expenses now or in retirement, the withdrawals—of contributions and any investment returns—are tax-free. 5

Learn more on Fidelity. com: IRA contribution limits

com: IRA contribution limits

Read Viewpoints on Fidelity.com: Just 1% more can make a big difference

Aim to have a diversified mix of investments. At least once a year, take a look at your investments and make sure you have the right amount of stocks, bonds, and cash to stay on track to meet your long-term goals, risk tolerance, and time horizon.

Aim to have a diversified mix of investments. At least once a year, take a look at your investments and make sure you have the right amount of stocks, bonds, and cash to stay on track to meet your long-term goals, risk tolerance, and time horizon.To see how your age, savings, and income can influence your savings rate, try Fidelity's savings rate widget.

Keep your eye on your dreams. Do the best you can to get to at least 15%. Of course, it may not be possible to hit that target every year. You may have more pressing financial demands—children, parents, a leaky roof, a lost job, or other needs. But try not to forget about your future—make your retirement a priority too.

Do the best you can to get to at least 15%. Of course, it may not be possible to hit that target every year. You may have more pressing financial demands—children, parents, a leaky roof, a lost job, or other needs. But try not to forget about your future—make your retirement a priority too.

See if your savings are on target in the Planning & Guidance Center.

Take advantage of potential tax-deferred or tax-free growth.

Get 4 easy guidelines to help you reach your retirement goals.

Learn more about our 4 key retirement metrics—a yearly savings rate, a savings factor, an income replacement rate, and a potentially sustainable withdrawal rate—and how they work together in the Viewpoints Special Report: Retirement roadmap.

close

View Larger Image

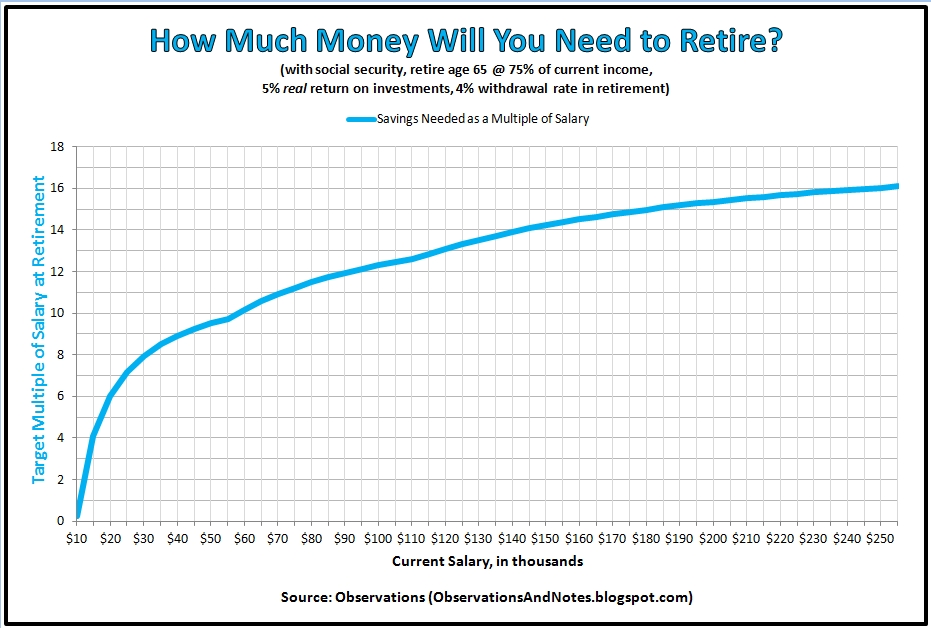

How much do you need to save for retirement? It's one of the most common questions people have. And no wonder. There are so many imponderables: When will you retire? How much will you spend in retirement? And for how long?

That's why we did extensive analysis to come up with age-based retirement savings factors that can help you plan—in spite of those uncertainties. These milestones are aspirational. You likely won't meet all of them. But they can serve as goalposts to help you make a plan to save enough to maintain your lifestyle in retirement.

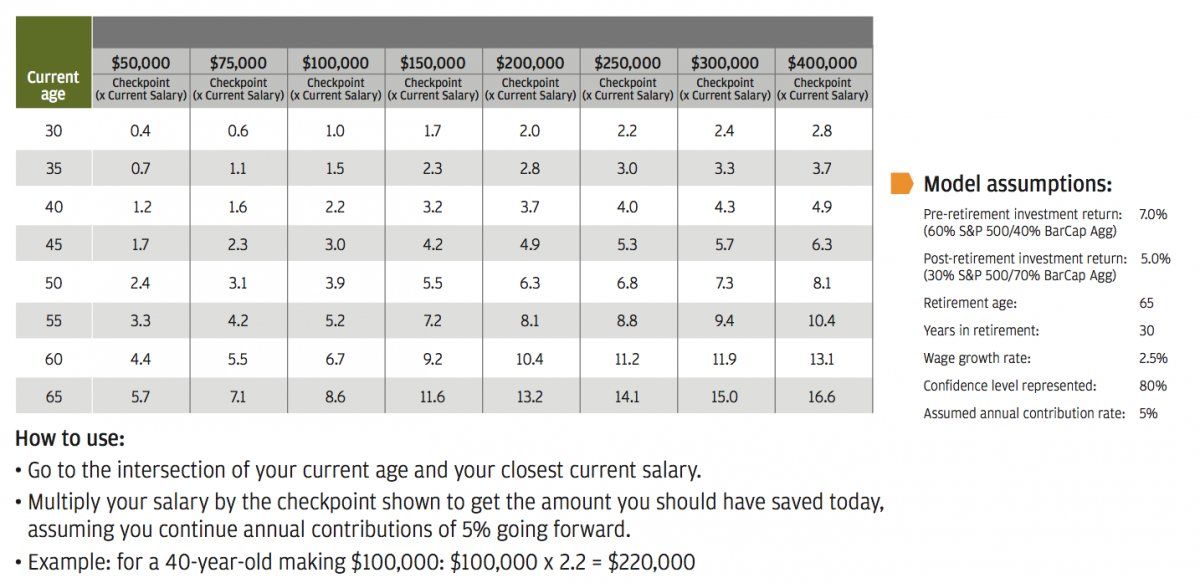

Our savings factors are based on the assumption that a person saves 15% of their income annually beginning at age 25 (which includes any employer match), invests more than 50% on average of their savings in stocks over their lifetime, retires at age 67, and plans to maintain their preretirement lifestyle in retirement (see footnote 1 for more details).

Based on those assumptions, we estimate that saving 10x (times) your preretirement income by age 67, together with other steps, should help ensure that you have enough income to maintain your current lifestyle in retirement. That 10x goal may seem ambitious. But you have many years to get there. To help you stay on track, we suggest these age-based milestones: Aim to save at least 1x your income by age 30, 3x by 40, 6x by 50, and 8x by 60. Your personal savings goal may be different based on various factors including 2 key ones described below. But these guidelines can provide a starting point to help your build your savings plan, and assess your progress.2,3

The age you plan to retire can have a big impact on the amount you need to save, and your milestones along the way. The longer you can postpone retirement, the lower your savings factor can be. That's because delaying gives your savings a longer time to grow, you'll have fewer years in retirement, and your Social Security benefit will be higher.

That's because delaying gives your savings a longer time to grow, you'll have fewer years in retirement, and your Social Security benefit will be higher.

Consider some hypothetical examples (see graphic). Max plans to delay retirement until age 70, so he will need to have saved 8x his final income to sustain his preretirement lifestyle. Amy wants to retire at age 67, so she will need to have saved 10x her preretirement income. John plans to retire at age 65, so he would need to have saved at least 12x his preretirement income.

Of course, you can't always choose when you retire—health and job availability may be out of your control. But one thing is clear: Working longer will make it easier to reach your savings goals.

See footnote at the end of the article for more information.

In other words, do you expect your expenses to go down when you retire? We call that a below average lifestyle. Or will you spend as much as you do now? That's average. If you expect your expenses will be more than they are now, that's above average.

Let's look at some hypothetical investors who are planning to retire at 67. Joe is planning to downsize and live frugally in retirement, so he expects his expenses to be lower. His savings factor might be closer to 8x than 10x. Elizabeth is planning to retire at age 67 and her goal is to maintain her lifestyle in retirement, so her savings factor is 10x. Sean sees retirement as an opportunity to travel extensively, so it may make sense for him to save more and plan for a higher level of retirement spending. His savings factor is 12x at age 67.

Joe is planning to downsize and live frugally in retirement, so he expects his expenses to be lower. His savings factor might be closer to 8x than 10x. Elizabeth is planning to retire at age 67 and her goal is to maintain her lifestyle in retirement, so her savings factor is 10x. Sean sees retirement as an opportunity to travel extensively, so it may make sense for him to save more and plan for a higher level of retirement spending. His savings factor is 12x at age 67.

Our simple widget lets you see the impact of these 2 variables—when you plan to retire and what kind of lifestyle you want to live in retirement—on how much you need to have saved when you do retire, and on all the intermediate milestones.

What if you're behind? If you're under age 40, the simple answer is to save more and invest for growth through a diversified investment mix. Of course, stocks come with more ups and downs than bonds or cash, so you need to be comfortable with those risks. If you're over 40, the answer may be a combination of increased savings, reduced spending, and working longer, if possible.

Of course, stocks come with more ups and downs than bonds or cash, so you need to be comfortable with those risks. If you're over 40, the answer may be a combination of increased savings, reduced spending, and working longer, if possible.

No matter what your age, focus on the goals ahead. Don't be discouraged if you aren't at your nearest milestone—there are ways to catch up to future milestones through planning and saving. The key is to take action, and the earlier the better.

See how small increases in contributions can add up over time.

Amount, account, and asset mix are important when saving for retirement.

years of experience.

Diana Shigapova

lawyer

In the second half of 2022 and in 2023, only those who received it earlier and for some reason did not use the right to retire will have the right to retire. From 2024, women will be able to retire at age 58, and men at age 63. nine0003

In 2028, the requirements will be tightened: men will retire at 65 and women at 60, while they will need to accumulate 30 pension points and 15 years of insurance experience. But if you meet a few more conditions, you can start receiving a pension earlier.

This is possible if they worked in harmful or difficult working conditions, served under a contract, gave birth to three or more children, or were fired at pre-retirement age. nine0003

nine0003

/prava-uchebnik/

Course: how to protect your rights at work

After years of service , for example, civil servants, military personnel, citizens and astronauts can retire flight test personnel.

Federal civil servants are officials who have entered into a service contract with the Russian Federation through federal authorities. nine0003

Art. 10 of the law "On the system of civil service of the Russian Federation"

They have a class rank, they wear a uniform, they receive a salary from the federal budget. The positions of federal civil servants are indicated in a special register.

The service pension for civil servants is not an early pension, but an additional one, in addition to the old-age pension. As a general rule, it cannot be obtained separately. But there is an exception. In order for federal government civil servants to be able to receive a retirement pension, regardless of whether there is an old-age pension, they must meet three conditions:

Clause 1.1 Art. 7 of the Law "On State Pension Provision in the Russian Federation"

Civil servants of the constituent entities of the Russian Federation and municipal employees can retire according to the length of service. The procedure for calculating the experience of municipal service is established by the regions.

Art. 25 of the law "On municipal service in the Russian Federation"

Military personnel are officers, sergeants, cadets, soldiers who serve in the Armed Forces of the Russian Federation, the National Guard, the FSB and other law enforcement agencies. For them, the superannuation pension replaces the old-age pension.

Art. 2 of the law "On the status of military personnel"

To receive a military pension, you must serve at least 20 calendar or grace years.

The procedure for calculating length of service

Grace years are when length of service is counted not one to one, but, for example, a year for two. This is possible not only because of service in harsh climatic conditions, but also in certain positions. For example, in positions of the Airborne Forces, where you need to systematically jump with a parachute, a month is considered one and a half. nine0003

This is possible not only because of service in harsh climatic conditions, but also in certain positions. For example, in positions of the Airborne Forces, where you need to systematically jump with a parachute, a month is considered one and a half. nine0003

Astronaut citizens are:

Early retirement is due to men who have worked for 25 years in any of these positions, and to women who have worked in them for 20 years. At the same time, men must work in a flight test unit for at least 10 years, women - at least 7.5.

Art. 7.1 of the Law "On State Pension Provision in the Russian Federation"

Experience is calculated as two months. And if an astronaut is in space, then a month of stay there is considered as five months of work.

Regulations on the provision of pensions for cosmonauts in the Russian Federation

If cosmonauts, due to health reasons, can no longer work, then men can retire after 20 years of service, and women after 15.

If the cosmonaut died, his wife, children and parents of retirement age can receive a survivor's pension.

Citizens from among the employees of the flight test personnel are:

Regulations on the procedure for assigning and paying pensions for years of service to flight test personnel

They are granted a service pension only together with an old-age pension. You won't get it before the time.

Conditions for assigning pensions to citizens from among the employees of the flight test staff

The length of service for each category of employees is calculated differently. For example, for pilots, a year is considered two if they have been conducting flight tests all this time. nine0003

For example, for pilots, a year is considered two if they have been conducting flight tests all this time. nine0003

But in any case, for the right to a service pension, the total length of service for men must be 25 years, for women - 20 years.

If flight work had to be left for health reasons, then the right to a seniority pension will be with at least 20 years of service for men and at least 15 years for women.

By experience. You can go on an old-age pension 2 years earlier if you have a long work experience: for men - 42 years, for women - 37 years. At the same time, a man must be at least 60 years old, a woman - 55 years old. nine0003

para. 1.2 art. 8 of the Law "On Insurance Pensions"

When working in hazardous conditions (list No. 1). Men can retire at 50, women at 45 if they have worked in underground work, work with harmful working conditions and in hot shops from list No. 1.

| Work experience in hazardous conditions | General insurance record | |

|---|---|---|

| For men | 10 years | 20 years old |

| For women | 7 years and 6 months | 15 years old |

Work experience in harmful conditions

for men

10 years old

for women

7 years and 6 months

Total experience

20 years 20,0003

for women

15 years

If men and women have worked half or more of the length of service in harmful conditions, then each year of such work reduces the retirement age. nine0003

nine0003

| Length of service for a man | Men's retirement age | Experience for a woman | Woman's retirement age |

|---|---|---|---|

| 5 years | 55 years old | At least 3 years and 9 months | 52 years old |

| 6 years | 54 years old | 4 years | 51 years |

| 7 years | 53 years old | 5 years | 50 years old |

| 8 years | 52 years old | 6 years old | 49 years old |

| 9 years old | 51 | 7 years old | 48 years old |

| 10 years | 50 years old | 7 years and 6 months | 45 years old |

Retirement age for a man depending on work experience in hazardous conditions:

A woman's retirement age depending on the length of service in hazardous conditions:

When working in difficult conditions (list No. 2) men can retire at 55, women at 50. To do this, they must work in jobs with difficult working conditions from list No. 2.

| Experience in difficult conditions | General insurance record | |

|---|---|---|

| For men | 12 years and 6 months | 25 years old |

| For women | 10 years | 20 years old |

Work experience in difficult conditions

for men

12 years and 6 months

for women

10 years

Total experience

For men

25 years

For women

20 years

reduce the retirement age by one year.

| Length of service for a man | Male retirement age | Length of service for a woman | Woman's retirement age |

|---|---|---|---|

| At least 6 years and 3 months | 58 years old | At least 5 years | 53 years old |

| At least 7 years and 6 months | 57 years old | At least 6 years | 52 years old |

| At least 10 years | 56 years old | At least 8 years | 51 |

| 12 years and 6 months | 55 years old | 10 years | 50 years old |

Retirement age for a man depending on the length of service in hazardous conditions:

A woman's retirement age depending on the length of service in hazardous conditions:

When working in the Far North , men can retire at 60, women at 55. To do this, work experience in the regions of the Far North must be at least 15 years, and in areas equated to them - 20 years. The total experience for men should be 25 years, for women - 20 years. nine0003

There are different options for those who have worked in the north.

What to do? 06/24/20

How to pass a medical examination for work in the Far North?

Those who have worked in the regions of the Far North for at least 7 years and 6 months are assigned a pension with a decrease in age by 4 months for each full year of work in these regions.

A woman who has given birth to two or more children and has worked for more than 12 years in the regions of the Far North or at least 17 years in equivalent areas can retire at 50 years old. The total experience must be at least 20 years. nine0003

Those who permanently reside in the regions of the Far North and areas equivalent to them and have worked as reindeer herders, fishermen, and hunters can also retire early. Men - at 50 years old, women - at 45. For this, men must work for at least 25 years, women - 20 years.

In case of liquidation of an enterprise or reduction of personnel, if it is impossible to find another job, you can retire 2 years before retirement age. In 2022 for men - at 60 years old, for women - at 55 years old. The insurance period must be at least 25 years for men and 20 years for women. nine0003

Art. 32 of the Law "On Employment in the Russian Federation"

153-FZ "On Amendments to Certain Legislative Acts of the Russian Federation"

registered with the employment service. So what? 01/24/19 Unemployed pre-retirees can retire two years earlier Civil aviation workers can retire earlier. Flight personnel Beneficial work experience 25 years for men, 20 years for women Upon dismissal for health reasons: Total insurance experience It does not matter Pension age , regardless of the age of , Aircraft flight management of preferential work 12 years and 6 months - for men for men for men , 10 years for women Total insurance experience 25 years for men, 20 years for women Retirement age 55 years for men, 50 years for women Engineering and technical composition of aircraft service Preferential work experience 20 years-for men, 15 years-for women Total experience 25 years-for women, 20 years-for women Retirement age 55 years for men, 50 years for women Special services workers. Rescuers in professional emergency rescue services, units of the Ministry of Emergency Situations, participants in the liquidation of emergencies Beneficial work experience 15 years Total insurance experience does not matter retirement age 40 years or later than Workers and employees in places of imprisonment of preferential work 15 years, for men, for men, for men, for men, for men, for men. Total insurance record 25 years for men, 20 years for women Retirement age 55 years for men, 50 years for women 0025 Fire guard, fire and rescue services

Who else can retire early

Who from civil aviation can retire early

Work / profession Preferential work experience General insurance record Retirement age Aircrew 25 years for men, 20 years for women Not relevant Regardless of age When dismissed for health reasons:

20 years for men, 15 years for women Aircraft Flight Control 12 years and 6 months for men, 10 years for women 25 years for men, 20 years for women 55 years for men, 50 years for women Aircraft maintenance engineer 20 years for men, 15 years for women 25 years for men, 20 years for women 55 years for men, 50 years for women

20 years old - for men; 15 years - for women  Former employees of the Federal Penitentiary Service, the State Fire Service, rescuers of the Ministry of Emergency Situations can retire early. nine0003

Former employees of the Federal Penitentiary Service, the State Fire Service, rescuers of the Ministry of Emergency Situations can retire early. nine0003 Which of the special services can retire early

Work / profession Preferential work experience General insurance record Retirement age Rescuers in professional emergency rescue services, units of the Ministry of Emergency Situations, participants in emergency response 15 years old Not relevant 40 or later Workers and employees in places of deprivation of liberty 15 years for men, 10 years for women 25 years for men, 20 years for women 55 years for men, 50 years for women Fire, fire and emergency services 25 years old Not relevant 50 years old  10 years for women

10 years for women

Preferential experience

25 years

Total insurance experience

does not matter the retirement age

50 years

must work 25 years, must work 25 years, but they can take early retirement only after 4 years. From 2023, the retirement date will move 5 years.

For example, in 2022, the experience of a school teacher was 25 years. He cannot immediately apply for a pension - he will have to wait 4 years. The teacher will need to apply for a pension in 2026. nine0003

Medical workers must have worked for at least 25 years in rural areas and urban-type settlements, or at least 30 years in cities, or at least 30 years mixed in cities, rural areas and urban-type settlements. Then they will be able to retire earlier than the generally established age.

The list of positions that are eligible for early retirement includes nurses.

Like teachers, medical workers in 2022 will be able to apply for a pension not immediately after completing the required length of service, but after 4 years. From 2023, you will have to wait 5 years. nine0003

Artists of theaters or theater and entertainment organizations can also retire early in the same order as teachers and doctors - 4-5 years after the required work experience has been completed.

List of professions and positions of employees of theaters and other theatrical and entertainment enterprises who are entitled to a retirement pension

Mothers of many children, who gave birth to three or more children and raised them up to 8 years old, can also count on an early pension. In this case, the woman’s insurance experience should be 15 years, and the pension coefficient should be from 30 points. nine0003

| Number of children | Retirement age |

|---|---|

| 3 | 57 years old |

| 4 | 56 years old |

| 5 or more | 50 years old |

Number of children

Retirement age

3

57 years

4

56 years

5 and more

50 years

Parents of disabled children can receive an early pension if the father's insurance record is at least 20 years and the mother's is 15 years. A pension can be issued either by a father at 55 or a mother at 50.

A pension can be issued either by a father at 55 or a mother at 50.

Disabled people and their guardians can also retire early.

/socstrah/

What benefits from the state are due to people with disabilities

| Type of disability | General insurance record | Retirement age |

|---|---|---|

| War trauma | 25 years for men, 20 years for women | 55 years for men, 50 years for women |

| By sight, with the first disability group | 15 years for men, 10 years for women | 50 years for men, 40 years for women |

| Lilliputians and disproportionate dwarfs | 20 years for men, 15 years for women | 45 years for men, 40 years for women |

Due to military trauma

Total insurance experience

25 years - for men, 20 years - for women

Pension age

55 years - for men, 50 years - for women

according to women vision, with the first group of disability

Total insurance experience

15 years - for men, 10 years - for women

Pension age

50 years - for men, 40 years - for women

Liliputs and imbalance of

Total experience

20 years - for men, 15 years for women

Retirement age

45 years for men, 40 years for women

Guardians can count on an early pension if they have raised disabled people since childhood. In their case, it happens like this: the retirement age decreases by a year for every 1.5 years of guardianship, but no more than 5 years in total. At the same time, men must have at least 20 years of insurance experience, and women - at least 15 years. nine0003

In their case, it happens like this: the retirement age decreases by a year for every 1.5 years of guardianship, but no more than 5 years in total. At the same time, men must have at least 20 years of insurance experience, and women - at least 15 years. nine0003

Who else. Early retirement is assigned to many more people - the list of positions and jobs is directly indicated in the law "On Insurance Pensions".

| Job/occupation | Length of service | General insurance record | Retirement age |

|---|---|---|---|

| Tractor drivers in agriculture, other sectors of the economy, drivers of construction, road and loading and unloading machines | 15 years old | 20 years old | 50 years - for women. This benefit is not available to men |

| Work in the textile industry with increased intensity and severity | 20 years old | Not relevant | 50 years - for women. This benefit is not available to men This benefit is not available to men |

| Workers of locomotive crews, workers in the organization of transportation and traffic safety in railway transport and the subway, truck drivers in mines, open pits, mines or ore quarries for the export of coal, shale, ore, rock | 12 years 6 months for men, 10 years for women | 25 years for men, 20 years for women | 55 years for men, 50 years for women |

| Work in expeditions, parties, detachments, at sites and in brigades on field geological exploration, prospecting, topographic and geodetic, geophysical, hydrographic, hydrological, forest management and survey work | 12 years 6 months for men, 10 years for women | nine0130 25 years for men, 20 years for women55 years for men, 50 years for women | |

| Workers, foremen in logging and rafting | 12 years 6 months for men, 10 years for women | 25 years for men, 20 years for women | 55 years for men, 50 years for women |

| Mechanics of complex crews at loading and unloading operations in ports | 20 years for men, 15 years for women | 25 years for men, 20 years for women | 55 years for men, 50 years for women |

| Work as a seafarer on ships of the sea, river fleet and fishing fleet | 12 years 6 months for men, 10 years for women | 25 years for men, 20 years for women | 55 years for men, 50 years for women |

| Drivers of buses, trolleybuses, trams on regular urban passenger routes | 20 years for men, 15 years for women | 25 years for men, 20 years for women | 55 years for men, 50 years for women |

| Work in underground and open pit mining in the extraction of coal, shale, ores and other minerals, in the construction of mines and mines | At least 25 years | Not relevant | Regardless of age |

| Longwall miners, tunnellers, jackhammers, mining machine operators | At least 20 years | Not relevant | Regardless of age |

| Work on ships of the sea fleet of the fishing industry for the extraction, processing of fish and seafood, acceptance of finished products in the fishery, on certain types of ships of the sea, river fleet and fleet of the fishing industry | 25 years for men, 20 years for women | Not relevant | Regardless of age |

Tractor drivers in agriculture, other sectors of the economy, drivers of construction, road and loading and unloading machines 9for women This benefit is not available to men

Work in the textile industry with increased intensity and heaviness of

Work experience

20 years

Total experience

does not matter

Pensions

50 years - for women. This benefit is not available to men

This benefit is not available to men

Workers of locomotive crews, workers in the organization of transportation and traffic safety in railway transport and subway, drivers of trucks in mines, open pits, in mines or ore quarries for the export of coal, slate, ore, work, rocks 6

12 years 6 months for men, 10 years for women

Total insurance experience

25 years for men, 20 years for women

Retirement age

55 years for men women

Work in expeditions, parties, detachments, in sites and in brigades at field exploration, search, topographic and geophysical, hydrographic, hydrological, forestry and survey work

Work experience

12 years 6 months-for men , 10 years for women

Total insurance experience

25 years for men, 20 years for women

Retirement age

55 years for men, 50 years for women

Workers, masters on logging and forestry

Work experience

12 months - for men, 10 years - for women

Total experience

25 years - for men, 20 years - for women

Retirement age

55 years - for men, 50 years - for women

Machine operators of integrated teams at loading and unloading operations in ports

Work experience

for women - 20 years -0003

Total insurance experience

25 years - for men, 20 years - for women

retirement age

55 years - for men, 50 years - for women

Work in the fluke, river fleet and river fleet and river vessels fishing fleet

Work experience

12 years 6 months for men, 10 years for women

Total insurance experience

25 years for men, 20 years for women

Retirement age 000355 years old - for men, 50 years old - for women

Drivers of buses, trolleybuses, trams on regular city passenger routes

Work experience

20 years - for men, 15 years - for women

Total insurance experience

25 for men, 20 for women

Retirement age

55 for men, 50 for women other minerals, in the construction of mines and mines

Work experience

at least 25 years

Total insurance experience

does not matter 9,0003

Pension age

, regardless of the age of

Mining workers, passers, slaughterers on chipped hammers, mining machine drivers.

Length of service

At least 20 years

Total insurance experience

Does not matter

Age of retirement

Regardless of age

Work on the vessels of the sea fleet of fish industry for mining, processing fish and seafood, receiving finished products in the fishing, on certain types of vessels of the sea, river fleet and fleet of fish industry

Work experience

25 years - for men, 20 years - for men, 20 years years for women

Total length of service

Does not matter

Retirement age

Regardless of age

To retire earlier, you need to earn the length of service necessary for the profession or work. It will include periods when a person worked, was on sick leave or cared for a child, but not more than 6 years.

Rules for calculating and confirming the insurance period

You should apply to the pension fund at the place of residence or to the MFC. You can apply at any time after you have accumulated the required experience.

You can apply at any time after you have accumulated the required experience.

To apply for a pension, you need to apply for its appointment. It is necessary to attach a passport, SNILS and a work book to it.

The Pension Fund of Russia has all the information about the length of service, since employers submit information about payments for their employees there every month. If the PFR suddenly did not have information about the length of service, then they can confirm it:

/npo/

How to get two pensions

All documents that confirm periods of work must have a number and date of issue. They should indicate the full name of the future pensioner, his date of birth, place of work, period of work, profession.

They should indicate the full name of the future pensioner, his date of birth, place of work, period of work, profession.

Sample application can be downloaded from the PFR website.

The application will be considered within 10 business days. The pension will be assigned from the day of applying for it, but not earlier than the day when the right to a pension appeared.

Until the day of application, a pension can be assigned if the application was made within 30 days from the date of dismissal. In this case, the pension will be assigned from the day following the day of dismissal from work.

/prava/pensiya/

Pensioners' rights by age

The Pension Fund may refuse to pay an early pension if there is not enough special service. Or if the applicant did not submit documents confirming the length of service, and the FIU does not have information that the applicant worked in such and such a place.

The formula for calculating pension payments in the general case is as follows:

Fixed payment + IPC × IPC cost.

The amount of fixed payments and the number of points are different for everyone. For example, in 2022, the generally established fixed payment is 6564.31 R, and for those who have worked in the Far North for 15 years, it is 9846.15 Р. It depends on the salary while working. For example, astronauts are paid 55% of their salary.