Key takeaways

Longer life expectancies mean your retirement savings may need to last 20 years or more.

Investments such as annuities, real estate investment trusts (REITs) and income-producing equities can offer additional retirement income beyond Social Security, a pension, savings and other investments.

The average life expectancy for a person who reaches age 65 in the U.S. is roughly 85 years.1 And that’s just the average.

About one out of every three 65-year-olds today will live past age 90, and about one out of seven will live past age 95.2 If you plan on retiring in your 60s, as many people do, you still need to make your retirement savings last almost 30 years.

That’s a lot of pressure to place on a traditional retirement account.

Social Security retirement benefits will replace only about 40% of your pre-retirement earnings. You'll need to supplement your benefits with a pension, savings or investments.

Social Security retirement benefits, intended more for lower wage earners, will replace only about 40% of your pre-retirement earnings; for a retiree who earned $100,000 a year, Social Security will only replace 33% of their pre-retirement earnings. You'll need to supplement your benefits with a pension (if available), savings or investments. Retirees seek part-time employment for all kinds of reasons, including the financial and mental benefits of staying active and involved in their communities. Still, it’s important to have a plan in place for generating additional income during your retirement.

Here are five common retirement investment options to help you generate income.

Income annuities

Income annuitiesAn income annuity is a contract between you and an insurance company where you pay a sum of money and that money is dispersed back to you through regular payments. Annuities can help you set up a guaranteed income stream for a certain period of time or for the rest of your life.

You pay a specific amount to an insurance company with the understanding that the money will be distributed to you at a later date. While the money is with the insurance company, it has the potential to accrue on a tax-deferred basis. When you start taking disbursements, you can choose a consistent income stream or account for rises in the cost of living to match inflation. You can also choose to have this income be paid through your own lifespan or through the lifespan of you and another person (e.g., your spouse).

Annuities may provide safety, long-term growth and income for a portion of your retirement assets. Retirees often use annuities to supplement the guaranteed sources of income to offset the expenses that don’t go away. Since they provide income guarantees, they're often used as insurance against outliving your retirement savings.

Since they provide income guarantees, they're often used as insurance against outliving your retirement savings.

Some annuities have liquidity features that state you or your heirs will receive the full amount of the investment back.

Total return investment approach

Total return investment approachA total return approach provides income from your investment portfolio in the form of interest, dividends, and capital gains. This type of portfolio invests in a balanced and diverse mix of stock and bond funds.

In this context, “total” return means spending a portion of the average annual rate of returns — income and appreciation — over a longer period (10-20 years), rather than focusing on specific annual return rates or just using portfolio income. The aim is that this total return meets or exceeds your withdrawal rate.

“This is a way to build a retirement portfolio to meet the needs of people preparing for a retirement that could last 20 to 30 years or longer,” says Rob Haworth, senior investment strategy director at U.S. Bank. “It might offer a way to generate a superior total return compared to other investment approaches traditionally pursued in retirement.”

Related to withdrawal rate, a total return approach follows a “systematic withdrawal” strategy, in which a certain percentage of your investment is taken as a distribution each year. The distribution amount generally ranges between 3 and 5% of the total value of the portfolio.

The distribution amount generally ranges between 3 and 5% of the total value of the portfolio.

Real estate is often attractive to retirees to generate income. While you can directly own and manage rental properties, a more practical option for most is to invest in REITs. This investment vehicle is somewhat comparable to a comingled fund; however, rather than owning securities, it invests in income-generating real estate.

Publicly-traded REITs are listed on major stock exchanges, so you can buy and sell this type of REIT as easily as you can trade stocks. Prices fluctuate on a daily basis. “This price fluctuation is a consideration for investors, because it isn’t just the underlying value of the assets held in the REIT that affects the price,” says Haworth. “What you pay for a REIT or the price you receive when you sell a REIT may be affected by outside factors that impact the broader investment environment.”

REITS often focus on specific types of properties (i.e., residential real estate, office properties, warehouse/industrial space, etc. ) and derive income from rents paid by tenants of the owned properties. Most REITs are classified as equity REITS and are focused on generating steady income from rental properties. There may be some capital appreciation potential if properties are sold. Mortgage REITS generate income through loans to other real estate owners and operators. Hybrid REITs combine both strategies.

) and derive income from rents paid by tenants of the owned properties. Most REITs are classified as equity REITS and are focused on generating steady income from rental properties. There may be some capital appreciation potential if properties are sold. Mortgage REITS generate income through loans to other real estate owners and operators. Hybrid REITs combine both strategies.

A non-traded REIT is a form of real estate investment that allows you to invest in a professionally managed portfolio of commercial real estate. This is a non-liquid asset that investors generally hold for the term of the trust until it is liquidated by the management team. As such, it is different from publicly-traded REITs, which can be bought and sold on public markets.

A non-traded REIT portfolio might include vacation properties, apartment buildings, hotels, data centers, healthcare facilities, office buildings, retail centers, self-storage, warehouses and timberland. Other potential investments might also include infrastructure, such as cell towers, energy pipelines and fiber cables. Most non-traded REITs focus on a single type of property.

Other potential investments might also include infrastructure, such as cell towers, energy pipelines and fiber cables. Most non-traded REITs focus on a single type of property.

These portfolios are actively managed by professionals who charge a fee for their services. A REIT manager typically appoints a property manager to oversee day-to-day operations of the real estate properties owned by the REIT. The managers collect rent from the properties and pay expenses, then distribute any income as dividends to investors.

“Non-traded REITS are not affected by day-to-day price volatility as is the case with publicly-traded REITs,” says Haworth. He cautions that in periods of economic distress, non-traded REITs can experience some challenges. “Because difficult circumstances that are unfavorable to the real estate market in general can arise at times, investors need to look at this as a long-term investment.”

While people primarily invest in stocks to generate capital appreciation in a portfolio, some equities generate income in the form of dividends. Publicly-traded companies frequently share their profits with shareholders by paying dividends. Not all stocks pay dividends, and of those that do, certain stocks tend to pay higher dividends than others.

Not all stocks pay dividends, and of those that do, certain stocks tend to pay higher dividends than others.

“Stock dividends became much more attractive when we experienced an extremely low interest rate environment in the bond market,” says Haworth. “It can be an effective way to diversify your income stream and generate competitive yields.”

Stock dividends are typically paid on a quarterly basis. At times, companies may pay a “special dividend” due to unusual circumstances, but those are uncommon and not something you should count on. Unlike most bonds, however, stock dividends can vary with each period that payouts are made. You need to be prepared for a degree of uncertainty with dividend payouts.

If your primary focus is to invest in a stock for income, it’s important to review its dividend-paying history. Stocks with a reliable history of consistent or steadily increasing dividend payouts are likely to be the most attractive to consider for this purpose.

The investment options you select in retirement should take into account your timeline and risk tolerance level. A financial professional can help you better understand these options and determine if one or more are appropriate for your retirement income strategy. The more you understand your options and overall financial picture, the better equipped you’ll be to head into (or continue in) your retirement years with confidence.

Learn how we can help you plan your retirement income strategy.

Retirement

Investing

Share:

How you withdraw funds from your investment accounts should align with your goals and needs. Here are three withdrawal strategies—and other factors—to consider.

Continue reading

From your home and rental properties to REITS and mortgage-backed securities, here are few things to consider as you explore real estate investment opportunities.

Continue reading

Find an advisor or banker

Disclosures

Start of disclosure content

Footnote

Return to content, Footnote

https://www. cdc.gov/nchs/data/hus/2019/004-508.pdf

cdc.gov/nchs/data/hus/2019/004-508.pdf

https://www.ssa.gov/pubs/EN-05-10529.pdf

Start of disclosure content

Investment and insurance products and services including annuities are:

Not a deposit ● Not FDIC insured ● May lose value ● Not bank guaranteed ● Not insured by any federal government agency.

U.S. Wealth Management – U.S. Bank | U.S. Bancorp Investments is the marketing logo for U.S. Bank and its affiliate U.S. Bancorp Investments.

Start of disclosure content

U.S. Bank, U.S. Bancorp Investments and their representatives do not provide tax or legal advice. Each individual's tax and financial situation is unique. You should consult your tax and/or legal advisor for advice and information concerning your particular situation.

You should consult your tax and/or legal advisor for advice and information concerning your particular situation.

This information represents the opinion of U.S. Bank and U.S. Bancorp Investments and is designed to be educational and informative. The views are subject to change at any time based on market or other conditions and are current as of the date indicated on the materials. This is not intended to be a forecast of future events or guarantee of future results. It is not intended to provide recommendations and/or specific advice concerning retirement accounts or investment planning. It is not intended to be construed as an offering of securities or recommendation to invest. Not for use as a primary basis of investment decisions. Not to be construed to meet the needs of any particular investor. Not a representation or solicitation or an offer to sell/buy any security. Investors should consult with their investment professional for advice concerning their particular situation.

Start of disclosure content

For U.S. Bank:

Equal Housing Lender. Deposit products are offered by U.S. Bank National Association. Member FDIC. Mortgage, Home Equity and Credit products are offered by U.S. Bank National Association. Loan approval is subject to credit approval and program guidelines. Not all loan programs are available in all states for all loan amounts. Interest rates and program terms are subject to change without notice.

U.S. Bank is not responsible for and does not guarantee the products, services or performance of U.S. Bancorp Investments, Inc.

U.S. Bank does not offer insurance products. Insurance products are available through our affiliate U.S. Bancorp Investments.

Start of disclosure content

For U.S. Bancorp Investments:

Investment and insurance products and services including annuities are available through U.S. Bancorp Investments, the marketing name for U.S. Bancorp Investments, Inc., member FINRA and SIPC, an investment adviser and a brokerage subsidiary of U. S. Bancorp and affiliate of U.S. Bank.

S. Bancorp and affiliate of U.S. Bank.

U.S. Bancorp Investments is registered with the Securities and Exchange Commission as both a broker-dealer and an investment adviser. To understand how brokerage and investment advisory services and fees differ, the Client Relationship Summary and Regulation Best Interest Disclosure are available for you to review.

Insurance products are available through various affiliated non-bank insurance agencies, which are U.S. Bancorp subsidiaries. Products may not be available in all states. CA Insurance License #0E24641.

Pursuant to the Securities Exchange Act of 1934, U.S. Bancorp Investments must provide clients with certain financial information. The U.S. Bancorp Investments Statement of Financial Condition is available for you to review, print and download.

The Financial Industry Regulatory Authority (FINRA) Rule 2267 provides for BrokerCheck to allow investors to learn about the professional background, business practices, and conduct of FINRA member firms or their brokers. To request such information, contact FINRA toll-free at 1-800‐289‐9999 or via https://brokercheck.finra.org. An investor brochure describing BrokerCheck is also available through FINRA.

To request such information, contact FINRA toll-free at 1-800‐289‐9999 or via https://brokercheck.finra.org. An investor brochure describing BrokerCheck is also available through FINRA.

U.S. Bancorp Investments Order Processing Information.

Municipal Securities Education and Protection– U.S. Bancorp Investments is registered with the U.S. Securities and Exchange Commission and the Municipal Securities Rulemaking Board (MSRB). An investor brochure that describes the protections that may be provided to you by the MSRB rules and how to file a complaint with an appropriate regulatory authority is available to you on the MSRB website at www.msrb.org.

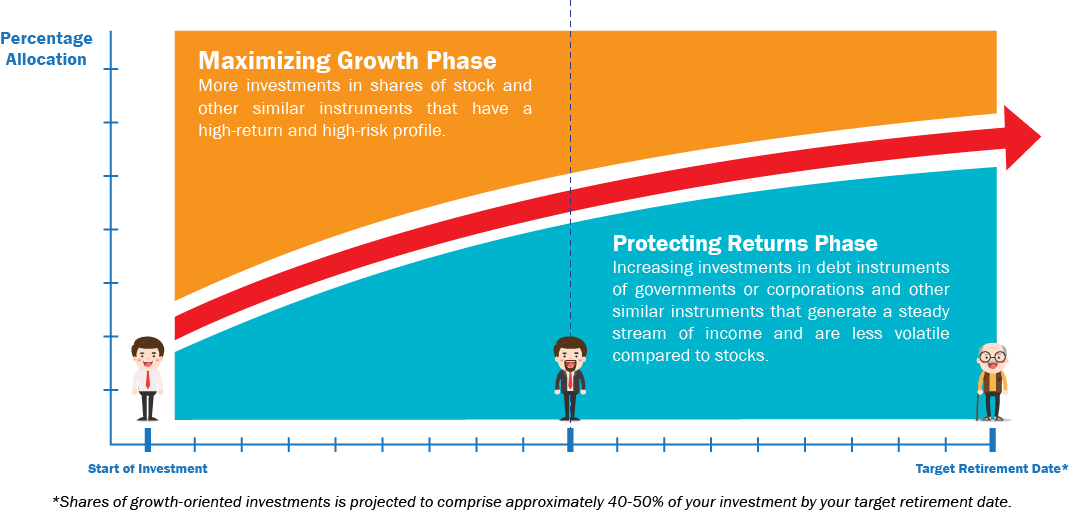

When you're young and just starting out, you can take more risk with the investments you've earmarked for retirement. After all, if you start in your 20s, you've got more than 40 years to grow your nest egg, and it's easier to weather the ups and downs of the market.

But as you approach your nonworking years, it's crucial to make sure you've got a clear plan for how you can afford to live on a fixed income as well as an understanding of where and how your cash is invested.

"The closer you get to retirement, the less risk you should take and more attention you should pay to what options qualify as less risky," says Ivory Johnson, certified financial planner and founder of Delancey Wealth Management.

Select spoke with financial experts to get their best advice on where you should put your money if retirement is right around the corner. Here are some low-risk options to consider:

While some of your money should be in the stock market, it's also good to have more on hand in a savings account that's easily accessible.

"When entering retirement, it's important to have an appropriate amount of cash available for short-term expenses and contingencies," says Gregory DePalma, CFP and director of advisory services at Empower (formerly Personal Capital).

A good rule of thumb is to have about three to six months worth of expenses in accessible reserves split between your checking and savings, says Shon Anderson, CFP at Anderson Financial Strategies. Keep one to two months of expenses in your checking, and two to four months of expenses in your savings.

As your lifestyle may change in retirement, make sure you're allocating enough into savings to match your new monthly expenses. Perhaps you downsized so your costs are lower or, on the other hand, your expenses could be higher if you have more medical bills or you've moved to a new city.

With a high-yield savings account, you can earn more interest than you would in a traditional savings, plus your money is FDIC-insured for up to $250,000 per account type per bank.

The Marcus by Goldman Sachs High Yield Online Savings offers an above-average APY, no fees whatsoever and easy mobile access. It's the most straightforward savings account to use when all you want to do is grow your money with zero conditions attached.

Learn More

Goldman Sachs Bank USA is a Member FDIC.

3.75%

None to open; $1 to earn interest

None

At this time, there is no limit to the number of withdrawals or transfers you can make from your online savings account.

None

N/A

No

No

Terms apply.

Another option is the American Express® High Yield Savings Account that also has a higher-than-average annual percentage yield and no fees, plus it allows savers up to nine free withdrawals or transfers per month (an increase from the traditional six).

Learn More

American Express National Bank is a Member FDIC.

3.50% APY as of 2/16/2023

Minimum balance to open is $0

$0

Up to 9 free withdrawals or transfers per statement cycle *The 6/statement cycle withdrawal limit is waived during the coronavirus outbreak under Regulation D

$0

$0

No

No

Terms apply.

American Express National Bank is a Member FDIC.

After safeguarding some cash in savings, look to low-risk investments that allow you to preserve capital while also earning a bit more than you would in a savings account. Short-term bonds are a good option because they aren't influenced as much by future volatility.

The challenge with low-risk investments is that rising inflation can eat away at their value over time. To counter this, you should consider putting your money in Treasury Inflation-Protected Securities, or TIPS. These are government bonds that mirror the rise and fall of inflation. Not only are they a safe investment, but they help you diversify your future retirement income.

TIPS bonds pay interest twice a year at a fixed rate, and they are issued in 5-, 10- and 30-year maturities, so you can choose which best matches your timeline to retirement. At maturity, investors are paid the adjusted principal or original principal, whichever is greater.

As retirement creeps closer and closer, one of the best thing you can do with some of your money is to put it somewhere safe and accessible. High-yield savings accounts and short-term bonds allow your cash to grow with low risk, plus TIPS help to hedge rising inflation.

Ideally, soon-to-be retirees should work with a financial advisor to review their individual savings and investment plans to make sure they're on track for all their goals.

Interest rate and APY are subject to change at any time without notice before and after an American Express® High Yield Savings Account is opened.

Editorial Note: Opinions, analyses, reviews or recommendations expressed in this article are those of the Select editorial staff’s alone, and have not been reviewed, approved or otherwise endorsed by any third party.

What to do if you want to secure a decent old age in advance, and whether it is worth investing for those who have crossed the fifth decade, Valery Yemelyanov, an analyst at Freedom Finance Investment Company, will tell

You can easily find dozens of blogs on Runet with stories about how people managed to "retire" at 35 or at least a few years ahead of schedule. In confirmation, they post data on their portfolios, present figures on the growth of securities and dividends received, and give advice to beginners. Often, their numbers look very plausible, and this inspires other people to take up long-term investments in earnest.

In confirmation, they post data on their portfolios, present figures on the growth of securities and dividends received, and give advice to beginners. Often, their numbers look very plausible, and this inspires other people to take up long-term investments in earnest.

If you were born after 1985 and have an average salary in Moscow (about ₽100 thousand per month), then you have a good chance of retiring as a dollar millionaire. The numbers speak for themselves: by investing in index funds at $300 over 30 years, you will receive exactly one million, of which dividends and share gains will bring more than $900 thousand. that the US market is growing at an average of 12% per year, including dividends. The same amount can be obtained on a regular calculator that calculates income on a bank deposit with regular replenishment.

www.adv.rbc.ru

And if you start at the age of 25 and invest up to 70% of your income (whatever it is) into your future pension, then in about seven to ten years the rent will equal your current earnings and you can quit without losing income. Actually, this is the popular strategy of young rentiers, not burdened with families, cars, dachas: to squeeze the maximum out of their career in order to retire at the age of not much older than 30.

Actually, this is the popular strategy of young rentiers, not burdened with families, cars, dachas: to squeeze the maximum out of their career in order to retire at the age of not much older than 30.

Photo: szefei / Shutterstock

The tactics of retired millennials are entirely based on the ideas of passive investment management. This is a classic of portfolio theory, tested by at least two generations of Americans born in the 1950s and 1960s. They were the first in the world to retire with assets in individual accounts of the IRA type (a prototype of the Russian IIA).

With this approach, you need to lay on investments for at least ten years, that is, do not sell securities for the entire period and continue to buy them until the retirement date comes.

The main secret of creating personal capital is quite simple: invest constantly from every income received. The recommended norm in international practice is 10% of your earnings. And it should be money that you won't need until your retirement. In other words, you will have to save separately for the "airbag" in the bank.

The recommended norm in international practice is 10% of your earnings. And it should be money that you won't need until your retirement. In other words, you will have to save separately for the "airbag" in the bank.

Pension assets should be separated from rainy day money and invested primarily in shares. Only in this case will the effect of compound interest work. Neither deposits, nor real estate, nor bonds will give capital gains several times over.

Statistics speak in favor of those who invest themselves, without using trust management services or complex financial products. Professionals manage to consistently beat index funds for two to three years, sometimes up to five years, but in general all portfolios tend to average 10-12% per annum (in US dollars) with dividends.

In rubles, you can earn 5-6% more, that is, up to 18% per annum over a period of 10-20 years, but this is an imaginary increase, it will be eaten up by the devaluation and inflation of the ruble. Real profitability for all years of investment will not be higher than in foreign securities.

Real profitability for all years of investment will not be higher than in foreign securities.

Photo: Matej Kastelic / Shutterstock

The principles of building personal wealth for old age can be learned from the practice of so-called target-date funds. These are briefcases securities created for a specific retirement year. The titan of the American financial industry, Vanguard, has a whole collection of such funds for retirees in 2065, 2060, 2055, and so on up to those who are already retired.

The Vanguard Group is a large privately held independent investment company. Located in Valley Forge, Pennsylvania. Founded at 1975 by John Bogle. The company unites about 370 funds, including 180 American and 190 foreign funds, and it is owned by the investors of these funds.

In Russia, shares of such funds are not available to an unqualified investor, but nothing prevents them from copying their structure. They invest in other mutual funds. As a rule, they have five or six pieces in their composition, of which one is obligatory for the entire US stock market, one for the shares of all other countries, and two more for bonds , respectively, the American market and international. The peculiarity of target-date strategies is that they are on autopilot.

The peculiarity of target-date strategies is that they are on autopilot.

For Russia with a retirement age of 60-65 years, if you are about 50, there is an average of 15 years left to build capital. However, such a rental pension is individual, and it can always be pushed back if work allows. But, based on a period of 10–15 years, it is worth focusing on a model portfolio, where 65–70% is invested in stocks and 30–35% in bonds.

According to my calculations, this gives the potential for growth of up to 5% in dollars and up to 11% in rubles annually. By putting a tenth of your income into such a portfolio every month, you will have capital in 15 years equal to about four of your annual income, which will increase by 40% of your usual average income per month.

For a person with a salary of ₽100 thousand, who saves ₽10 thousand each, it looks like this. He started investing at the age of 50, increased his portfolio to ₽4.6 million by the age of 65 and receives about ₽40 thousand per month from it (half in dividends and coupons, half in value growth). Taking into account what the state will pay (₽20-30 thousand per month for a given salary), a rentier pensioner will have more than 60% of what he earned before retirement. This is quite worthy even by the standards of Western countries.

He started investing at the age of 50, increased his portfolio to ₽4.6 million by the age of 65 and receives about ₽40 thousand per month from it (half in dividends and coupons, half in value growth). Taking into account what the state will pay (₽20-30 thousand per month for a given salary), a rentier pensioner will have more than 60% of what he earned before retirement. This is quite worthy even by the standards of Western countries.

The point of view of the authors whose articles are published in the "Pro's Opinion" section may not coincide with the opinion of the editors.

A financial instrument used to raise capital. The main types of securities: shares (gives the owner the right of ownership), bonds (debt security) and their derivatives. More A debt security whose owner has the right to receive from the person who issued the bond its face value within a specified period. In addition, the bond implies the right of the owner to receive a percentage of its face value or other property rights. Bonds are the equivalent of a loan and are similar in principle to the lending process. Both governments and private companies can issue bonds. Investment is the investment of money to generate income or to preserve capital. There are financial investments (purchase of securities) and real ones (investments in industry, construction, and so on). In a broad sense, investments are divided into many subspecies: private or public, speculative or venture, and others. Read more

Bonds are the equivalent of a loan and are similar in principle to the lending process. Both governments and private companies can issue bonds. Investment is the investment of money to generate income or to preserve capital. There are financial investments (purchase of securities) and real ones (investments in industry, construction, and so on). In a broad sense, investments are divided into many subspecies: private or public, speculative or venture, and others. Read more

The stereotypical image of a “poor pensioner” does not involve talking about financial independence and investing. But in practice, many older Russians, despite modest incomes, have savings. And in retirement, for the first time, they find time to think about how to manage money. In this text, we will talk about the features of investing with retirement.

Why would a retiree invest savings set aside for old age? Two main reasons: to ensure better safety of money, if the amount is already enough for all your future plans, or to increase capital through the return on investment, if the amount necessary for your goals for the second half of life is not yet in the account.

For many pensioners, the savings "lie on the book" (current account or deposit). It seems that the amount is growing, thanks to the interest dripping on it. But in reality, you can buy less every year with the accumulated money: prices grow faster than your money in the bank. Therefore, the first rule of savings is to choose instruments with a return higher than inflation.

You can navigate the official inflation rate - in June it was 6%. Interest on deposits in banks is on average slightly lower - 4-5%, new customers or those who spend a lot on the card of the same bank can count on an increased percentage. For comparison, dollar-denominated bonds of Russian companies (FXRU) brought in over the past year 9.1% yield in rubles. Of the exchange instruments, bonds are the least risky (coupon income is fixed and is a percentage of the face value).

It is worth remembering that in practice, prices for different goods grow unevenly, and with official inflation of 6%, the cost of your food basket or a trip to your relatives can grow by tens of percent in the same year. Therefore, it is important to analyze costs and adjust the strategy, taking into account the speed with which your savings are being eaten away.

Therefore, it is important to analyze costs and adjust the strategy, taking into account the speed with which your savings are being eaten away.

Savings are threatened not only by inflation, but also by specific risks associated with the currency and economy of the country where you live. In the event of a default, multi-year savings can “turn into a pumpkin” overnight. Diversifying your investments (distributing money between instruments that behave differently) will help protect against these risks. You can buy bonds not only of Russian, but also of American companies or the US Treasury, and in addition - gold, which protects against loss of money in both local and global economic crises. But the bank account does not imply such diversification. In addition, the bank itself can "burst" if we are talking about a scenario of a serious default of the country's economy - but a portfolio of bonds of international issuers and gold cannot "burst" overnight.

Retirees, like everyone else, may have dreams that require more money than they managed to save: to go on a trip, to have a wedding for their children, or to give their grandson a degree in a prestigious university, and finally, to leave behind a legacy. Investing in stocks can help get closer to their realization.

Investing in stocks can help get closer to their realization.

What money cannot be invested? An investor, regardless of age, needs to remember: it is worth investing only available funds, that is, accumulated savings, with the exception of the “airbag”, which is approximately 6 monthly budgets. You can not take loans to play on the stock exchange, save on food, medicines.

Shares are a riskier instrument than bonds, but also more profitable: in good times, an investor can receive tens of percent of profit per year. So, for example, the model portfolio "Comfortable old age", consisting of FXGD gold, FXRB bonds and shares of the FXRW world market in proportion to moderate risk for an investor of 55 years, has brought 15.2% per annum in the last 3 years. True, in moments of market downturns, the portfolio will also become cheaper, albeit for a while - this is the inevitable reality of participation in the incomes of the world economy.

The risk and depth of portfolio drawdowns, however, can be managed—again, through diversification. Investing in ETFs in broad market stocks, such as FXWO (share fund of the world's top companies), FXDM (share fund in developed countries, except for the United States), protects the investor from the risk of investing in the “wrong company”, perhaps typical for beginners.

ETFs do not select stocks based on someone's expectations or forecasts, but strictly follow the composition of the stock index - that is, within stock ETFs, there are always "winning" companies, those that cost the most. When a company leaves the index, it also leaves the fund, and another strong player takes its place. And since the fund contains shares of not one or two companies - but tens and hundreds - the elimination of one "loser" does not lead to the loss of all savings, as in the case of buying shares one at a time. You can create an individual portfolio with the parameters of profitability and maximum drawdown that the investor needs using the constructor on the FinEx website.