Net debt is a liquidity metric used to determine how well a company can pay all of its debts if they were due immediately. Net debt shows how much debt a company has on its balance sheet compared to its liquid assets.

Net debt shows how much cash would remain if all debts were paid off and if a company has enough liquidity to meet its debt obligations.

To determine the financial stability of a business, analyst and investors will look at the net debt using the following formula and calculation.

Net Debt = STD + LTD − CCE where: STD = Debt that is due in 12 months or less and can include short-term bank loans, accounts payable, and lease LTD = Long-term debt is debt that with a maturity date longer than one year and include bonds, lease payments, CCE = Cash and liquid instruments that can be Cash equivalents are liquid investments with a maturity of 90 days or less and include certificates of deposit, Treasury bills, and \begin{aligned} &\text{Net Debt} = \text{STD} + \text{LTD} - \text{CCE}\\ &\textbf{where:}\\ &\begin{aligned} \text{STD} = &\text{ Debt that is due in 12 months or less}\\ &\text{ and can include short-term bank}\\ &\text{ loans, accounts payable, and lease}\\ &\text{ payments}\end{aligned}\\ &\begin{aligned} \text{LTD} = &\text{ Long-term debt is debt that with a}\\ &\text{ maturity date longer than one year}\\ &\text{ and include bonds, lease payments,}\\ &\text{ term loans, small and notes payable}\end{aligned}\\ &\begin{aligned} \text{CCE} = &\text{ Cash and liquid instruments that can be}\\ &\text{ easily converted to cash. }\end{aligned}\\ &\text{Cash equivalents are liquid investments with a}\\ &\text{maturity of 90 days or less and include}\\ &\text{certificates of deposit, Treasury bills, and}\\ &\text{commercial paper} \end{aligned} Net Debt=STD+LTD−CCEwhere:STD= Debt that is due in 12 months or less and can include short-term bank loans, accounts payable, and leaseLTD= Long-term debt is debt that with a maturity date longer than one year and include bonds, lease payments,CCE= Cash and liquid instruments that can beCash equivalents are liquid investments with amaturity of 90 days or less and includecertificates of deposit, Treasury bills, and

}\end{aligned}\\ &\text{Cash equivalents are liquid investments with a}\\ &\text{maturity of 90 days or less and include}\\ &\text{certificates of deposit, Treasury bills, and}\\ &\text{commercial paper} \end{aligned} Net Debt=STD+LTD−CCEwhere:STD= Debt that is due in 12 months or less and can include short-term bank loans, accounts payable, and leaseLTD= Long-term debt is debt that with a maturity date longer than one year and include bonds, lease payments,CCE= Cash and liquid instruments that can beCash equivalents are liquid investments with amaturity of 90 days or less and includecertificates of deposit, Treasury bills, and

The net debt figure is used as an indication of a business's ability to pay off all of its debts if they became due simultaneously on the date of calculation, using only its available cash and highly liquid assets called cash equivalents.

Net debt helps to determine whether a company is overleveraged or has too much debt given its liquid assets. A negative net debt implies that the company possesses more cash and cash equivalents than its financial obligations and is hence more financially stable.

A negative net debt means a company has little debt and more cash, while a company with a positive net debt means it has more debt on its balance sheet than liquid assets. However, since it's common for companies to have more debt than cash, investors must compare the net debt of a company with other companies in the same industry.

Net debt is in part, calculated by determining the company's total debt. Total debt includes long-term liabilities, such as mortgages and other loans that do not mature for several years, as well as short-term obligations, including loan payments, credit cards, and accounts payable balances.

The net debt calculation also requires figuring out a company's total cash. Unlike the debt figure, the total cash includes cash and highly liquid assets. Cash and cash equivalents would include items such as checking and savings account balances, stocks, and some marketable securities. However, it's important to note that many companies may not include marketable securities as cash equivalents since it depends on the investment vehicle and whether it's liquid enough to be converted within 90 days.

Unlike the debt figure, the total cash includes cash and highly liquid assets. Cash and cash equivalents would include items such as checking and savings account balances, stocks, and some marketable securities. However, it's important to note that many companies may not include marketable securities as cash equivalents since it depends on the investment vehicle and whether it's liquid enough to be converted within 90 days.

While the net debt figure is a great place to start, a prudent investor must also investigate the company's debt level in more detail. Important factors to consider are the actual debt figures—both short-term and long-term—and what percentage of the total debt needs to be paid off within the coming year.

Debt management is important for companies because if managed properly they should have access to additional funding if needed. For many companies, taking on new debt financing is vital to their long-growth strategy since the proceeds might be used to fund an expansion project, or to repay or refinance older or more expensive debt.

A company might be in financial distress if it has too much debt, but also the maturity of the debt is important to monitor. If the majority of the company's debts are short term, meaning the obligations must be repaid within 12 months, the company must generate enough revenue and have enough liquid assets to cover the upcoming debt maturities. Investors should consider whether the business could afford to cover its short-term debts if the company's sales decreased significantly.

On the other hand, if the company's current revenue stream is only keeping up with paying its short-term debts and isn't able to adequately pay down long-term debt, it's only a matter of time before the company will face hardship or will need an injection of cash or financing. Since companies use debt differently and in many forms, it's best to compare a company's net debt to other companies within the same industry and of comparable size.

Company A has the following financial information listed on its balance sheet. Companies will typically break down whether the debt is short-term or long-term.

Companies will typically break down whether the debt is short-term or long-term.

To calculate net debt, we must first total all debt and total all cash and cash equivalents. Next, we subtract the total cash or liquid assets from the total debt amount.

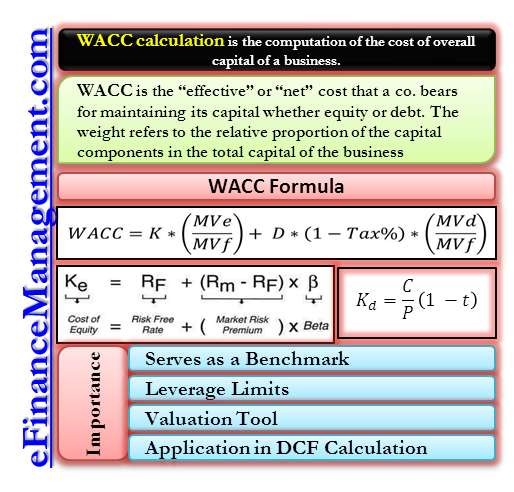

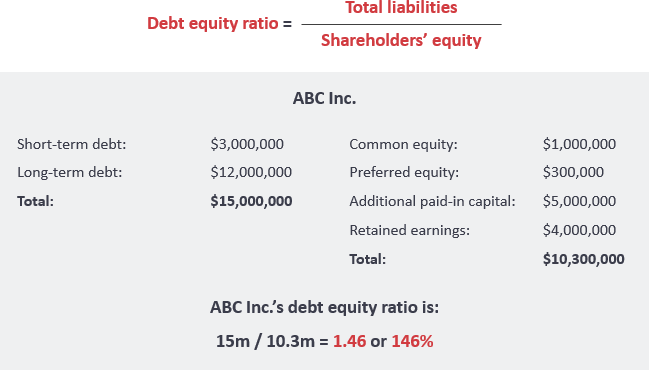

The debt-to-equity (D/E) ratio is a leverage ratio, which shows how much of a company's financing or capital structure is made up of debt versus issuing shares of equity. The debt-to-equity ratio is calculated by dividing a company’s total liabilities by its shareholders' equity and is used to determine if a company is using too much or too little debt or equity to finance its growth.

Net debt takes it to another level by measuring how much total debt is on the balance sheet after factoring in cash and cash equivalents. Net debt is a liquidity metric while debt-to-equity is a leverage ratio.

Although it's typically perceived that companies with negative net debt are better able to withstand economic downtrends and deteriorating macroeconomic conditions, too little debt might be a warning sign. If a company is not investing in its long-term growth as a result of the lack of debt, it might struggle against competitors that are investing in its long-term growth.

For example, oil and gas companies are capital intensive meaning they must invest in large fixed assets, which include property, plant, and equipment. As a result, companies in the industry typically have significant portions of long-term debt to finance their oil rigs and drilling equipment.

An oil company should have a positive net debt figure, but investors must compare the company's net debt with other oil companies in the same industry. It doesn't make sense to compare the net debt of an oil and gas company with the net debt of a consulting company with few if any fixed assets. As a result, net debt is not a good financial metric when comparing companies of different industries since the companies might have vastly different borrowing needs and capital structures.

It doesn't make sense to compare the net debt of an oil and gas company with the net debt of a consulting company with few if any fixed assets. As a result, net debt is not a good financial metric when comparing companies of different industries since the companies might have vastly different borrowing needs and capital structures.

Gross debt is the nominal value of all of the debts and similar obligations a company has on its balance sheet. If the difference between net debt and gross debt is large, it indicates a large cash balance along with significant debt, which could be a red flag. Net debt removes cash and cash equivalents from the amount of debt, which is useful when calculating enterprise value (EV) or when a company seeks to make an acquisition. This is because a company is not interested in spending cash to acquire cash. Rather, the net debt will give a better estimate of the takeover value.

To calculate net debt using Microsoft Excel, find the following information on the company's balance sheet: total short-term liabilities; total long-term liabilities; and total current assets. Enter these three items into cells A1 through A3, respectively. In cell A4, enter the formula "=A1+A2−A3" to compute net debt.

Enter these three items into cells A1 through A3, respectively. In cell A4, enter the formula "=A1+A2−A3" to compute net debt.

Net debt per capita is a country-level metric that looks at a nation's total sovereign debt and divides it by the population size. It is used to understand how much debt a country has in proportion to its population allowing for between-country comparisons in understanding a country's relative solvency.

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors' opinions or evaluations.

Getty

In a mythical American past, families took out one 30-year mortgage, worked at one company for 30 years while paying off the mortgage and sailed off into retirement free of debt.

Today, the reality is that the dream of retiring debt free is fading, and debt among older Americans is soaring. The percentage of households headed by someone aged 65 and older who held any debt increased to 61% in 2016 from 38% in 1989, according to the Federal Reserve—while real average debt increased to $86,797 from $29,918 (in 2016 dollars).

The percentage of households headed by someone aged 65 and older who held any debt increased to 61% in 2016 from 38% in 1989, according to the Federal Reserve—while real average debt increased to $86,797 from $29,918 (in 2016 dollars).

While it’s always been fashionable to advise old people to pay off their debts before retirement, for many people it’s just not realistic. And at the same time, paying down debt while in retirement can be extremely challenging, thanks to the vagaries of a fixed income.

Cost-of-living increases for Social Security have hovered around 2% for many years, so it’s not hard to see how cruel the math of a 19% credit card APR or even 8% student loan interest rate can be for retirees.

Here’s the truth: There are no easy answers when it comes to paying down debt in retirement. Let’s look at the upsides and some of the downsides of nine strategies that might help, depending on your particular circumstances.

It’s essential to stop racking up debt when you stop working. That might sound obvious, but it’s not always so clear for some retirees, says Paul Miller, a New York-based CPA.

That might sound obvious, but it’s not always so clear for some retirees, says Paul Miller, a New York-based CPA.

“Many people think that when they retire, their expenses go down, but they tend to increase,” says Miller, owner of Miller & Company, LLP. Retirees want to do things that cost money, like travel. Some people buy a dream retirement home, when they should be downsizing, Miller says.

When you’re on a fixed income in retirement, take extra care not to add more debt. That’s especially true of high-interest debt, like credit card debt. If you hope to get free of what you owe, that means living well within your means so you have resources to pay down existing debt while eschewing more.

Some people end up in retirement and realize they haven’t saved nearly enough, then make rash decisions in an effort to make up for lost time. That can be catastrophic, Miller warns.

“People become day traders. They do things outside their normal personality… and they jeopardize their retirement,” Miller warns. He’s seen plenty of cases where one spouse doesn’t tell the other about these risky steps until things really go south. “And most often, it’s irreparable at that point,” he says.

He’s seen plenty of cases where one spouse doesn’t tell the other about these risky steps until things really go south. “And most often, it’s irreparable at that point,” he says.

If you haven’t saved enough for retirement, look for ways to maximize your available retirement funds. That could mean working longer to delay taking Social Security, which offers you larger monthly payments the longer you defer it, or…

Though it might seem obvious, establishing a new income stream is really the best answer for many who do not have enough retirement savings. Part-time work—as a consultant, as a gig worker, at a coffee shop—might not be your dream retirement scenario, but it’s really the least-bad choice of all the other options to deal with debt in retirement.

So let’s change that old axiom about paying off debt before retirement: Keep working, at least a little, when you have high-interest debt to pay.

An added benefit of stretching out your working life is you may be able to obtain health insurance to bridge the gap to Medicare age. You also give your existing retirement savings more time to compound and grow, which can help build your nest egg.

You also give your existing retirement savings more time to compound and grow, which can help build your nest egg.

Leveraging your retirement savings to pay off debt can be tempting, but it’s also risky and must be done with great care, even if you’ve hit 59 ½ and can do so penalty free.

First, consider that you lose not only the cash you withdraw from investments, but also potential future market gains. Say you live to 85 and pull out $20,000 at age 65 to pay off a car loan. You’ve just lost 20 years of investment growth. If someone had made that move 20 years ago, in 2001, they would have given up an extra $58,000 in their retirement account today (assuming the money would have been left in an S&P 500 index fund).

But that’s not even the only reason to avoid using retirement funds for debt pay off. Consider interest rates. With fixed-rate debt—like some mortgages, for example—the face value of your payment remains consistent, even as inflation rises. This means the longer your mortgage term, the less real value you’re paying for it.

This means the longer your mortgage term, the less real value you’re paying for it.

“There’s an incentive to keep the mortgage instead of committing other assets,” says Chris Chen, a certified financial planner (CFP) with Insight Financial Strategists.

In addition, you may cause unintended tax consequences for yourself. For starters, you could miss out on years of being able to deduct mortgage payments from your taxes. But you’ll also potentially incur a large tax bill if you’re taking money out of a traditional individual retirement account (IRA) or 401(k) account.

“Depending on the case, you could end up with 60 to 70 cents for every $1 withdrawn,” says Chen. “In this case, the retiree gives up an appreciating asset, pays taxes, in order to pay off a depreciating debt.”

Finally, if you’ve been paying off your debt for a while, keep in mind that you may not actually save that much in interest by paying your debt off now. If you are only a few years from paying off a loan, most of your payment goes towards principal, so the interest savings is minimal, Chen says.

If you own your home—or most of your home—consider scaling back on your house size and amenities, particularly if you are lucky enough to live in an area where housing prices have risen significantly.

Take that hard-earned equity and move into a smaller home that’s cheaper to maintain, and hopefully has more predictable repair costs and property taxes into the future. You may also choose to take your money and use it to buy a house in an area with a lower cost of living, if family circumstances allow.

“The problem is that a retiree may find it difficult to qualify for a mortgage. So, if there is equity in the house, that may well be the upper limit of a downsize,” Chen says.

Pooling some of your debts to get a lower interest rate can work in some special circumstances. This is especially true if you have untapped equity in your home and can use it for a low-interest home equity loan.

The trouble is this strategy includes all the risks of borrowing money to fix a spending problem. Depending on your particular situation, you may end up violating tip #2: Don’t try to fix mistakes with bigger mistakes.

Home equity loans or debt consolidation loans can make a lot of sense for a one-time surprise medical bills, for example. But if the underlying spending/income mismatch isn’t fixed, you’re just causing more debt headaches down the line.

Another way to tap home equity without incurring another monthly debt payment is a reverse mortgage. This tool can be used by people aged 62 and over to borrow against their home equity, and payments aren’t required until the borrower sells the house, moves or dies.

If you’re not ready to give up ownership in your home, you might consider a reverse mortgage home equity line of credit, which makes that money available if you need it in case of emergency. Reverse mortgages have a checkered past, but new regulations have cleaned up the industry, to a degree. Still, proceed with caution.

Still, proceed with caution.

“If their retirement plan is tight already, which is the case for many, a retiree can monetize their home by replacing their mortgage with a reverse mortgage,” says Chen. “The benefit is that they would free themselves from monthly payments without depleting their retirement assets.”

You might have value in a life insurance policy you don’t really need any longer, such as if your kids are finished with college. You can access the money in a cash value policy by taking a loan against it or even surrendering the policy.

This strategy can be expensive, however, with fees eating up as much as 30% of the settlement value. There can also be tricky tax complications, so proceed with care.

Note that you cannot pursue this strategy with term life policies, which are very popular because they are cheaper options. Getting cash value from life insurance only works with permanent life insurance such as whole life or universal life insurance.

In certain situations, you can also get money for a policy via a life settlement transaction. This strategy is mainly suitable for older policyholders who are in bad health.

Transferring a credit card balance to a card with a lower rate—or a low intro rate—are two good ways to get out from under oppressive interest rates. But they come with one very large caveat: The tactic should really be a one-time tool.

Borrowing money to pay debts doesn’t solve the underlying problem. That’s why the best answer for older people with oppressive levels of debt is often…

It’s okay to waive the white flag: Bankruptcy laws exist for a reason. Many older Americans have a strong ethos to pay all their bills, and that’s a good thing. But when you can’t pay, you can’t pay. And the sooner you come to that realization, the better.

Many people make huge mistakes while spiraling out of control, taking out home loans or spending retirement money to pay down debt that could be discharged in bankruptcy.

Social Security and many retirement accounts are protected assets in bankruptcy. That can make many older Americans “judgement proof”—they have no assets for a credit card issuer to claim. That also means it can be worth negotiating debt relief from certain kinds of loans without declaring bankruptcy, says Gerri Detweiler, author of “Debt Collection Answers.”

“If you do need to negotiate down the balance and don’t care about your credit history, you could potentially settle debt for substantially less than you owe,” she says. “Doing so will hurt your credit score, but do you really need good credit history any more?”

Bankruptcy shouldn’t be the first resort, but it shouldn’t be the last resort, either. Just beware that it doesn’t solve all debt problems. Student loan debt generally cannot be discharged in bankruptcy, though Miller suggests that clients in big trouble convert student loans to credit card debt, then discharge that later through bankruptcy.

Detweiler recommends finding a bankruptcy attorney via the National Association of Consumer Bankruptcy Attorneys.

When it comes to paying debt in retirement, older Americans should prioritize their own needs when choosing their strategy, says Miller.

“A lot of people have this, ‘I want to leave this for my kids’ mentality,’” says Miller, who recommends that your first priority is to take care of your own finances.

If you’re retired and feeling overwhelmed by debt, pay for the services of a financial planner or CPA who can help you make a plan to clean up your financial life. Most importantly, follow their advice and stick to the plan.

Was this article helpful?

Rate this Article

★ ★ ★ ★ ★

Please rate the article

Please enter valid email address

CommentsWe'd love to hear from you, please enter your comments.

Invalid email address

Thank You for your feedback!

Something went wrong. Please try again later.

Information provided on Forbes Advisor is for educational purposes only. Your financial situation is unique and the products and services we review may not be right for your circumstances. We do not offer financial advice, advisory or brokerage services, nor do we recommend or advise individuals or to buy or sell particular stocks or securities. Performance information may have changed since the time of publication. Past performance is not indicative of future results.

Forbes Advisor adheres to strict editorial integrity standards. To the best of our knowledge, all content is accurate as of the date posted, though offers contained herein may no longer be available. The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners.

Bob Sullivan is a Peabody-award winning journalist and the author of five books, including New York Times Best-Sellers, Gotcha Capitalism and Stop Getting Ripped Off! He spent nearly two decades working at MSNBC. com and NBC News, and he still appears on TODAY, NBC Nightly News, and CNBC. He now writes The Red Tape Chronicles column at RedTape.Substack.com and hosts a podcast about the unintended consequences of technology.

com and NBC News, and he still appears on TODAY, NBC Nightly News, and CNBC. He now writes The Red Tape Chronicles column at RedTape.Substack.com and hosts a podcast about the unintended consequences of technology.

John Schmidt is the Assistant Assigning Editor for investing and retirement. Before joining Forbes Advisor, John was a senior writer at Acorns and editor at market research group Corporate Insight. His work has appeared in CNBC + Acorns’s Grow, MarketWatch and The Financial Diet.

The Forbes Advisor editorial team is independent and objective. To help support our reporting work, and to continue our ability to provide this content for free to our readers, we receive compensation from the companies that advertise on the Forbes Advisor site. This compensation comes from two main sources. First, we provide paid placements to advertisers to present their offers. The compensation we receive for those placements affects how and where advertisers’ offers appear on the site. This site does not include all companies or products available within the market. Second, we also include links to advertisers’ offers in some of our articles; these “affiliate links” may generate income for our site when you click on them. The compensation we receive from advertisers does not influence the recommendations or advice our editorial team provides in our articles or otherwise impact any of the editorial content on Forbes Advisor. While we work hard to provide accurate and up to date information that we think you will find relevant, Forbes Advisor does not and cannot guarantee that any information provided is complete and makes no representations or warranties in connection thereto, nor to the accuracy or applicability thereof. Here is a list of our partners who offer products that we have affiliate links for.

This site does not include all companies or products available within the market. Second, we also include links to advertisers’ offers in some of our articles; these “affiliate links” may generate income for our site when you click on them. The compensation we receive from advertisers does not influence the recommendations or advice our editorial team provides in our articles or otherwise impact any of the editorial content on Forbes Advisor. While we work hard to provide accurate and up to date information that we think you will find relevant, Forbes Advisor does not and cannot guarantee that any information provided is complete and makes no representations or warranties in connection thereto, nor to the accuracy or applicability thereof. Here is a list of our partners who offer products that we have affiliate links for.

Are you sure you want to rest your choices?

Pension calculator

for Russian Railways employees

CORPORATE PENSION ASSIGNMENT

A corporate pension is granted if the following conditions are met simultaneously:

Reaching the retirement age in accordance with the legislation of the Russian Federation and the Regulations on NGOs for employees of Russian Railways, or the appointment of an early old-age insurance pension or a disability insurance pension

the period of payment of pension contributions (insurance period) must be at least 5 years (60 months) *, or 1 month (in case of disability)

dismissal from Russian Railways **

* If the insurance period at the date of dismissal was less than 60 months, then it can be increased by paying additional personal contributions.

** It is possible to assign and pay a corporate pension to a contributor without dismissal from the company in the event of his transfer at his request from a position belonging to the category "managers" to a lower-paid position belonging to the category "specialists", "employees" or "workers". ". nine0009

HOW IS THE CORPORATE PENSION CALCULATED?

The amount of the non-state pension is calculated from the total amount accumulated on the individual pension account during the period of participation in the corporate pension system. This amount, in turn, consists of several components. Firstly, these are the personal contributions of the participant and the contributions of the employer. Secondly, it is the investment income that the non-state pension fund accrues annually on the entire amount accumulated in the account. nine0010

DETAILS...

Thirdly, these are additional personal contributions that each participant-contributor of the corporate pension system can make. In addition, when assigning a corporate pension, the presence of industry awards is taken into account.

In addition, when assigning a corporate pension, the presence of industry awards is taken into account.

It should also be noted that when calculating the amount of a monthly non-state pension, an annual rate of return of 4% for the entire period of payment, that is, future income, is taken into account.

In addition, by decision of the Board of Directors, non-state pensions may be indexed. nine0010

You can make a preliminary calculation of the amount of your future pension by using the Pension Calculator service or by contacting the nearest branch of JSC NPF BLAGOSOSTOYANIE.

HIDE...

PENSION PERIOD

There are several options for paying a pension: life, urgent (for a specified period) and phased. The amount of the monthly payment will also depend on the chosen period: the smaller it is, the higher the amount of the monthly corporate pension. But it is important to understand that in the case of a fixed-term pension, payments will stop after the due date, but the need for additional income will remain. nine0010

nine0010

DETAILS...

Lifetime pension is the most popular payment option: the contributor will receive a corporate pension in addition to the state pension throughout his life.

In the case of choosing a fixed-term pension, the contributor himself chooses the period during which payments will be made, for example, 10 years.

Another option is the phased payment of pensions, “step by step”. It can be chosen by contributors who draw up an urgent pension with a payment period of at least 14 years for women and 10 years for men. In this case, the pension payment period is divided into two equal stages. During the first stage, the pension is paid in an increased amount - 160% of the calculated monthly amount of the lifelong non-state pension. And at the second stage, the amount of the payment will be determined based on the funds remaining in the pension account. nine0010

HIDE...

HOW TO REMAIN THE RIGHT TO A CORPORATE PENSION IF YOU HAVE LESS THAN 5 YEARS?

Employees who leave before they have completed 5 years of insurance coverage can make up for the missing period of service by paying additional personal pension contributions.

DETAILS...

At the same time, the amount of each contribution must be at least twice the amount of the monthly financial assistance that the company pays to non-working pensioners with more than 30 years of experience in railway transport. The number of months during which the contributor pays additional contributions after leaving RZD will be included in the length of service. nine0010

HIDE...

INCREASED CORPORATE PENSION FOR WORKERS WITH INDUSTRY AWARDS

When assigning a non-state pension, the presence of industry awards is taken into account.

DETAILS...

10% increase in the amount of corporate pension for contributors awarded with the badge "For 30 years of excellent work in railway transport" "Honorary Railwayman", sign (badge) "Honorary Railwayman". nine0010

The size of the corporate pension is increased by 15% for contributors who have been awarded the badge “For 40 years of excellent work in railway transport”.

The size of the corporate pension is increased by 40% for contributors who were awarded the second badge “Honorary Railway Worker of JSC Russian Railways” or “Honorary Railway Worker” of the Russian Ministry of Transport during the period of work at JSC Russian Railways.

HIDE...

CORPORATE PENSION INDEX

The decision to increase payments to pensioners is made by the Board of Directors, based on financial indicators based on the results of operations over the past year. At the same time, the increase in payments for the least socially protected groups of pensioners is carried out regularly. nine0010

DETAILS...

For example, in 2018, the amount of payment to recipients who were assigned a non-state pension in 2017 due to the establishment of group I disability was increased by 70%, in 2016 it was decided to index by 15% pensions to recipients who, as of January 1, 2014, turned from 70 to 79 years old. In 2015, payments were increased for pensioners over the age of 70, as well as for the disabled, veterans of the Great Patriotic War and other categories of pensioners.

TAXATION OF NON-STATE PENSION

According to Russian tax legislation, at the stage of payment of a non-state pension, personal income tax is withheld. However, personal income tax is levied on the part of the funds paid to the pensioner, formed at the expense of the employer's contributions. No personal income tax is levied on the part of the pension formed at the expense of the employee's personal contributions.

USE THE FUND SERVICES. IT'S COMFORTABLE!

Control the status of your account using the "Personal Account" service. To gain access to your personal account, you must contact the personnel department or the nearest branch of the fund. nine0010

Connect the free service "SMS-informing", to receive important information about your future pension.

The Rostec Non-State Pension Fund (NPF Rostec), the core corporate operator of the Corporation's pension programs, has launched an updated website , which provides complete information about the benefits and conditions of participation in corporate pension programs, compulsory pension insurance, and also provides the opportunity to calculate the amount of a future pension on an interactive pension calculator based on the amount of contributions and the period of participation in the corporate program.

The development of customer services is one of the priority areas of activity for NPF Rostec. The fund's updated website makes it possible to provide the Corporation's employees with full access to information on managing pension savings through an intuitive interface. nine0010

“The Corporation has approved the Uniform Standards for the Implementation of Corporate Social Policy, which provide for the possibility of providing each employee with a wide range of social programs, taking into account individual needs and life situation. Non-state pension provision is one of the key elements of social support, the implementation of which was entrusted to NPF Rostec with methodological support from the HR Department. The corporate pension program is based on the principles of employee and employer co-financing and allows the employee to form pension capital, including through investment income. It should be noted that NPF shows one of the best returns on the pension asset management market. The corporate pension program also provides for the succession of pension contributions and tax benefits for both the employee and the employer. In 2023, work to promote the corporate pension program will continue, taking into account the financial capabilities of our organizations and their needs,” commented Yulia Tsvetkova, HR Director at Rostec. nine0010

The corporate pension program also provides for the succession of pension contributions and tax benefits for both the employee and the employer. In 2023, work to promote the corporate pension program will continue, taking into account the financial capabilities of our organizations and their needs,” commented Yulia Tsvetkova, HR Director at Rostec. nine0010

One of the important tools of the new online platform is an interactive pension calculator that will help calculate the future pension of an employee of the Corporation based on the amount of pension contributions and the period of his participation in the corporate pension program. For non-Rostec customers, the pension calculation is based on the period of validity of the individual pension contract.

The mobile version of the Rostec online platform is adapted to any screen resolution and is compatible with most popular devices. In the near future, the user's personal account will be available on the site. nine0010

NPF Rostec has been successfully operating in the pension services market for over 28 years.