(Updated August 2021)

Tire Agent understands how important it is to have quality tires on your vehicles. We also understand that sometimes it's hard to come up with the money to pay for a large purchase like four brand new tires, which causes some of our customers to sacrifice quality in order to finance cheap tires.

Because of the importance of buying quality tires that last a long time and get the best MPG and performance out of your vehicle, we offer several options for financing tire purchases, including ways to buy tires with bad credit histories.

We are always looking for the best ways to help our customers buy tires online, so check our finance page for the most up-to-date options we offer.

VIEW FINANCE OPTIONS NOW

Ultimate Guide to Buying Tires With Bad Credit, No CreditFinancing your tire purchase through Tire Agent is easy and secure and takes very little time because we give you an instant approval decision. You can apply for more than one payment plan if your first choice is denied, and this will not affect your credit score.

So, you may be wondering, “What are these payment plans?” Consumer goods companies are partnering with third party finance companies so their customers can finance their purchase at the time of checkout. To see the third-party finance companies that partner with Tire Agent, visit our finance page.

The process is straightforward and hassle free: First, find your tires by selecting the "Shop by Vehicle" option at the top of any page. Review the recommended tires and, when you are on any product page of the Tire Agent website, click the payment plan you want to apply for. Once you click to apply, an access code is sent to your mobile phone and you simply enter the code to confirm your identity, answer a few quick questions and just like that your request is processed!

Tire Payment Plan OptionsAt the time of purchase, we have two easy financing options for you to purchase your tires. PayPair is Tire Agents' exclusive proprietary tire financing platform that is suitable for all of our shoppers. For convenience, we also partnered with Affirm leading pay-as-you-go firm for users with prime credit that want to avoid financing fees if paid by a certain date.

PayPair is Tire Agents' exclusive proprietary tire financing platform that is suitable for all of our shoppers. For convenience, we also partnered with Affirm leading pay-as-you-go firm for users with prime credit that want to avoid financing fees if paid by a certain date.

For no-credit-needed tires, our PayPair program is suitable for customers who have no credit, low credit scores, or bad credit histories. PayPair offers one application for six tire payment plans. Options range from no money down to $49 down with payments up to 24 months. For details, visit our financing page to learn more.

AffirmTire payment plans with Affirm may or may not include interest and will affect your credit score. Affirm offers a variety of repayment terms — 3, 6 and 12 month plans and they don't penalize you if you pay it off early.

ViabillSome customers with bad credit or low credit scores might be offered an option to finance their tire purchases with ViaBill.

If you thought that “buy now, pay later” didn’t exist for people looking to buy tires with low credit scores, we hope you've learned that this is a myth! Purchasing new tires on credit just became possible and affordable due to flexible payment options that help people with low or no FICO credit score. Yes, that’s what we said — low or NO credit score buyers can be approved. Applying for these plans will not affect or harm your existing credit score, because only a soft credit check is performed, which is why you receive your decision instantly./cchistory-220377e5cf6e491689f9eace5cfe8132.jpg)

Welcome to the largest rim and tire financing store online – we offer a lease to own program for high quality cheap tires and rims (a great financing alternative), rim financing, and other payment options through our trusted partners, Snap Finance and PayPal Credit. You can also pay the retailer's cash price with credit card or debit cards as payment options at checkout. With our tire financing options, you have access to low payments with bad credit or no credit needed - so don't pay inflated retail prices somewhere else! Get your tires delivered in as little as 2-3 business days with our fast delivery, and we offer free shipping with every purchase!

We carry thousands of different tire packages and wheels in various sizes so that you can find the cheapest tires and wheels online and save money over the brick and mortar tire shop.

Fill out the easy application for Snap Finance's lease-to-own option with weekly or monthly payments, or select PayPal Credit to finance tires.

Our cheap tires and wheels ship fast and are usually delivered to your door in as little as 3-5 business days from when you place your order.

Once your order is delivered, just make your low monthly or weekly payments on your purchases and enjoy your brand new tires or wheels!

By using a financing option through PayLaterTires, you could save upfront cash and buy tires online instead of paying inflated retail prices. We have cheap tires for your car, truck, tractor, semi-truck, motorcycle, RV, or other vehicle even if you don't have good credit! Pre Qualify for brand new tires or wheels today and use our search vehicle tool to find the perfect tires for you! The application requires just a little personal information and takes only two minutes!

Snap Finance is a lease-to-own financing provider that empowers credit-challenged shoppers with a less than positive credit history with the buying power to get what they need now and pay over time without a loan from the bank. Snap Finance is accessible to people with all credit types. So even if you have a low credit score, or no credit score at all, we can help you without a credit check to buy wheels, rims, or new tires! Its application process is the best and it is so convenient and simple; you’ll get a decision in seconds - so apply online today! Learn more about how you can get instant approval with no credit needed and save money with us when you apply.

Snap Finance is accessible to people with all credit types. So even if you have a low credit score, or no credit score at all, we can help you without a credit check to buy wheels, rims, or new tires! Its application process is the best and it is so convenient and simple; you’ll get a decision in seconds - so apply online today! Learn more about how you can get instant approval with no credit needed and save money with us when you apply.

When you select the payment plan option through Pay Later Tires to purchase new tires or wheels, you save upfront cash and get the tire size you need for your car, truck, tractor, semi-truck, motorcycle, RV, or other vehicle on a payment plan that works for you! If you need help getting tires for your car right now, come learn about our approval process and see how you can get great tires on affordable monthly payment plans.

Our process is quick and easy, and you'll receive a decision on tire leasing or financing instantly. If you need help, our highly trained experts are standing by and love solving problems. You can also pay with a credit or debit card if you don't finance with PayPal! After you go through our approval process, you can start making purchases on your tires using a credit card, debit card, or automated payments through your bank account.

You can also pay with a credit or debit card if you don't finance with PayPal! After you go through our approval process, you can start making purchases on your tires using a credit card, debit card, or automated payments through your bank account.

Pay Later Tires is a convenient way to find cheap tires or wheels for your vehicle and pay for them using an affordable payment plan.

Pay Later Tires lets you shop from the convenience of your home or mobile device so you can find the best tire for your needs, no matter where you are!

When you apply for the lease to own program through at Snap Finance, we do not run a credit check or ask for personal references on you and there's no down payment required to start your lease agreement. Even if you have bad credit or no credit at all, you may still get approved! By paying your remaining lease payments on time you will be developing credit much like traditional financing though, or pay the early purchase options cost to save the most money.

Pay Later Tires carries thousands of high quality cheap tires and wheels from the top brands in the industry, so you can find the perfect set of tires for your car, truck, SUV, or another vehicle with affordable payments, no hidden fees, no initial payment required with our lease to own program, and free shipping.

When you apply for wheel and tire packages at Pay Later Tires, your information is safe and secure because we use 256-Bit SSL encryption to transmit information between our servers and your computer or mobile device.

If you're in the market for new wheels, rim and tire financing can help you get the set you want. By financing your purchase or using a lease-to-own option, you can spread out your payments and avoid putting a big dent in your wallet upfront. Here at Pay Later Tires, we offer a variety of rim and tire financing options to fit your budget.

We have partnerships with some of the leading lenders in the country, so we can offer you competitive rates and terms. Plus, our easy application process means you can get started on securing your dream set of wheels today!

You could be pre-approved with PayPal Credit to finance rims or finance cheap tires through our online tire shop, or use your existing credit card or debit card with PayPal when you checkout. There's no down payment required if you are approved for PayPal Credit, and for qualified buyers there's no interest on your purchase if you pay it off within 6 months.

If you don't want wheel and tire financing, you can checkout with Snap Finance and get up to $3000 for your rim and tire purchase. There's no credit needed to apply for a lease agreement and you can get your new rims and tires as soon as in 2-3 business days!

There's no initial payment required, so you just pay your remaining lease payments until the end of the tire lease or use one of the early purchase options to pay our retailer's cash price . Depending on how you are paid and the payment plan you choose, you could pay a monthly payment or weekly payment and have your payments come directly out of your bank account.

Depending on how you are paid and the payment plan you choose, you could pay a monthly payment or weekly payment and have your payments come directly out of your bank account.

This is a great financing alternative for people who don't have good credit but need affordable payments like there are with leasing costs. Just keep in mind, the early purchase options cost is the best way to save money on new tires or custom wheels.

Need new rims or tires but don't want to pay all at once? Apply for rim and tire financing with us today and get an instant decision on monthly payments. Once approved, sign your lease online and we'll ship your items as soon as the same day!

If you are looking for cheap tires that are also high quality, then you have come to the right place. Here at Pay Later Tires, we offer a wide variety of quality tires from different brands at very affordable prices. We also offer free shipping on all orders!

We also offer free shipping on all orders!

Excellent choice for cheap tires and wheel financing. Ordered tires and they showed up at my door only two days later.

This place had the cheapest tires and it only took a few days for the set to show up, great service!

The bad credit tire financing process was very easy. I plan on using Pay Later Tires for all my tire purchases in the future.

My tires showed up only 4 days after I placed my order and they had the lowest prices online. My local store was asking for the same tires.

Learn all about rim and tire financing with no credit needed by reading our Pay Later Tires blog!

Date : September 8, 2022

Need new tires but don't have the cash? No problem! Check out our guide on how to finance tires and get bac...

read more

Date : August 11, 2022

Everything you need to know about electric vehicle tires, including the best EV tires, types of EV tires, b. ..

..

read more

Antonina Sergeeva

journalist

Author profile

Michel Korzhova

former bank employee

hired or you're just bored - look at your credit history.

Perhaps you will learn a lot of interesting things about yourself in it. In the first article in the series, we will tell you what a credit history is, who requests it, and why it is important.

A credit history is a record of you as a borrower. The subject of the credit history is the borrower for whom this dossier was filed.

In the credit history you can see:

Credit history is stored in the credit bureau — BKI. In July 2021, eight BKIs are operating in Russia. The largest are NBKI, Equifax, OKB and Russian Standard credit bureau.

In July 2021, eight BKIs are operating in Russia. The largest are NBKI, Equifax, OKB and Russian Standard credit bureau.

State Register of Credit Bureaus

Your credit history can be in all of them, in some of them or only in one. Each bank decides for itself which bureaus to cooperate with.

For a credit history, apply directly to the BCI or through third-party services. Twice a year you don't have to pay for getting a credit report at each bureau. All additional requests will be subject to a fee.

What to do? 04/26/18

I want to apply for a free credit report. How to do it?

There are no rules on how a credit history should look, but each must have several mandatory parts: title, main, information and closed.

Art. 4 of the Federal Law "On credit histories"

In the title part - standard general data about the subject of the credit history: full name, passport details, TIN and SNILS.

In the main - information about current loans and court decisions that have entered into force on the recovery of funds, on bankruptcy, as well as the borrower's credit rating, if the BKI calculates it.

A credit rating, or a score, is an assessment of your payment discipline based on the data that the CBI has about you. The bureau takes into account whether a person took loans, how many there were and how he paid them off. It is important to understand that a credit rating is informational in nature.

/guide/credit-raiting/

How to find out your credit rating

It helps to roughly estimate your chances of getting a loan. At the same time, a bank issues a loan, not a bureau. When deciding whether to issue a loan or not, the bank evaluates a lot of additional information about the borrower that the bureau does not have. Because of this, it happens that the credit rating may not be very high, but loans are still issued, and vice versa: the rating is high, but loans are denied.

In the information part - all submitted applications for a loan and the result of their consideration: a loan was issued or not.

Only the borrower sees the closed part . It lists everyone who has ever requested a subject's credit history and who has submitted information to it.

Credit history of an individual. For example, my credit history looks like this.

Since I have never taken loans, my CI contains only information about which banks requested itAnd this is how the credit history of a person who took loans looks like. It contains information about the type of loan, when it was taken, from which bank, for what amount and how it was paid out

Deciphering the symbols: how the client repaid the loan

Retelling the loan

Delays: green chart - no delinquency

And like this looks like the credit history of the person who took loans. It contains information about the type of loan, when it was taken, from which bank, for what amount and how it was paid

Character interpretation: how the client repaid the loan

Loan retelling

Delays: green graph - no delinquencies

If there were delinquencies, they will be indicated in the credit report as time ranges. This is how they look in Equifax In the NBKI, delinquencies look like in this picture, but in the OKB they are not highlighted at all

This is how they look in Equifax In the NBKI, delinquencies look like in this picture, but in the OKB they are not highlighted at all The credit history of legal entity is different in that it does not contain an information part. The title part contains details instead of personal data: name, address, PSRN, TIN. Since organizations can be sold, merged and change names, the title part contains information about this as well.

paragraph 5 art. 4 FZ dated December 30, 2004 No. 218-FZ

Credit history begins to form after the first application for a loan. When you apply, the bank asks for your consent to check your credit history. If you do not give consent, the bank will not be able to look at your credit history, but will not be able to issue you a loan.

What to do? 04/10/19

Inquiries from banks appeared in the credit history, which I did not contact

Even if you don't get a loan in the end, information about the submitted application will appear in your credit history.

Banks sometimes ask you to agree to a credit check if you use a debit card. This is so that the bank can continue to offer you different products, including loans.

When applying for a debit card, you can refuse to check your credit history with the bank. This cannot be the reason for the refusal of a debit card.

When I applied for a Raiffeisenbank debit card, there was a checkbox in the application for the card to agree to a credit history check. I put "No" because loans do not interest meDifferent banks assess credit history differently. For example, some banks check information on loans for the last year, others analyze how loans were paid three or even five years ago.

Another example: some banks are critical even of minor delays, while others are ready to issue a loan, even if a person had several delays of several months.

What to do? 02/05/18

I have a lot of small loan arrears

A special borrower assessment system is called scoring. Banks consider a good credit history with the following properties.

Banks consider a good credit history with the following properties.

Over one year old. The older she is, the more information about the borrower the bank can study. This helps to better assess its solvency. This criterion works in conjunction with the number of loans taken.

For example, if a person took out one loan in 2015 and repaid it in 2016, the age of the credit history will not matter much: the loan was a long time ago, the borrower’s financial situation could change and how he will be able to repay loans in 2021 is already not quite clear.

No delays. It is desirable that they do not exist at all. If they were, everything will depend on how long the loan was not paid and how long the delays were. For example, if you didn’t pay a loan for six months, then made a payment and a month later applied for a new loan, most likely the bank will not be ready to give you a loan: there is a risk that your financial situation is unstable.

Without a large number of simultaneous applications for loans. If a person applies for five credit cards or cash loans at the same time, the bank may think that the person is in financial trouble. Because of this, the scoring system may refuse a loan.

An exception is if we are talking about a mortgage or a car loan. These loans are secured by collateral, and here the bank understands for sure that a person is simply comparing offers from banks, and is not planning to take out five mortgages at the same time.

How many loans there were. The more loans the borrower has successfully repaid, the better. Separately, it will be useful if a person took different loans: cash loans, installment goods, credit cards, mortgages or car loans. So the bank will understand that a person can plan his money for different types and amounts of loans.

Credit load. If a person has a lot of open loans, he may not be able to cope with a new loan. It is simply unprofitable for a bank to issue a loan to a credited borrower.

It is simply unprofitable for a bank to issue a loan to a credited borrower.

What to do? 28.02.20

How does the debt load indicator affect the terms of loans?

The key indicators of bad credit history are delinquency and high credit load. A particularly negative factor is if the loan was sold to collectors, the borrower was sued, or he did not repay the loan at all. In such cases, the bank is likely to refuse a loan.

All other indicators are secondary. For example, the frequency of applications for loans or decisions on them are important for one bank, while another is more loyal to this information.

Some banks may be wary of borrowers who do not yet have a credit history. Since there is no information about how a person previously repaid loans, it is not clear how he will repay the loan: will he repay it on time, pay it in advance, or not pay it at all.

Credit history is used by lenders, insurers and employers. So they are looking for reliable customers and employees. By law, any organization that has the written consent of the subject of a credit history has the right to request his credit history.

So they are looking for reliable customers and employees. By law, any organization that has the written consent of the subject of a credit history has the right to request his credit history.

Lenders decide whether to lend or not. Creditors can be:

The lender must check the borrower: how reliable is he and whether he can return the money. Whichever bank you apply to, they will all see your credit history.

Insurers protect themselves from fraudsters and irresponsible people. If a client is late with payments and has several loans, then he obviously does not have enough money. For their sake, he may simulate an accident. Therefore, insurers are ready to increase the cost of the policy for such clients or even refuse them insurance. For borrowers with a good credit history, the insurer can make a discount on the insurance policy.

Customers with loan arrears more often turn to insurance companies for payment and ask for 30-50% more than reliable customers.

Source: Kommersant

Car sharing services request a credit history for similar reasons . If a person pays his loans poorly, it is more likely that he will treat the rented car in the same way, and in the event of an accident it will be problematic to recover damages from him.

Employers rate an employee: how disciplined and responsible he is. Typically, large companies, as well as financial and credit organizations, request a credit history, in particular if a person is applying for an important position. If a person is credited, then he clearly has problems with decision-making.

Community 11/23/20

Employer requests information about my financial obligations. It is legal?

Izvestiya newspaper experts believe that such an employee will fail the project, fail to notice the mistake, or cheat. Credit history is a litmus test for a position with financial responsibility: director, accountant or supply manager.

Credit history is a litmus test for a position with financial responsibility: director, accountant or supply manager.

Meet according to the report - an article in Rossiyskaya Gazeta

Credit history falls under the law on the protection of personal data, so it is not given out to just anyone. This means that if an employer wants to check your credit history, they must ask you to sign a written consent. You can refuse, but then the employer may also refuse to employ you.

Assess your chances of getting a loan. If you have already taken loans before, it is worth checking your credit history at least once a year in case there are errors.

What to do? 06/19/18

I want to correct a mistake in my credit history and not pay anything for it

For example, sometimes it happens that information about the payment of a loan did not appear in the credit history, which may cause a delay for a person. As a result, a person is denied loans, although he paid everything off.

As a result, a person is denied loans, although he paid everything off.

Understand why a loan is denied. It happens that a person has never made delinquency on loans, and he is denied new loans. In case of refusal of a loan, the bank is obliged to inform the BCI of the reason for which the loan was refused. After looking at the reason in the credit report, it will be possible to roughly understand what exactly the bank did not like: you yourself or your credit history.

What to do? 03/05/19

I refused a credit card, and a bank refusal appeared in my credit history, how so?

The credit history is updated every time new information about the borrower becomes available. For example, if a person has applied for a loan, made a payment or is late, this information will appear in the credit history.

By law, the source of credit history formation is obliged to report to the CBI information about any changes in the borrower's credit history within five working days.

Section 5, Art. 5 Federal Law "On credit histories"

All information about previously taken loans will disappear from the credit history if it has not changed in ten years: no one asked for it, you did not submit new applications, you did not have current loans. In practice, this is almost impossible.

paragraph 1 of Art. 7 FZ "On credit histories"

Information about you may be in the CBI, even if you have never applied for loans.

I have never taken loans, but there is information about me in the CBI. This is due to the fact that I agreed to check my credit history when applying for a job and applying for a debit card. Therefore, although I did not take loans, the bureau still stores information about me.

Additional information about debts can be submitted by mobile operators and bailiffs due to delays in alimony and housing and communal services.

If you have any questions or want to know more, watch the video. A bank loan expert explains what a credit history is, why it is so important for banks and what to do if you plan to take out a large loan, but there is no credit history.

A bank loan expert explains what a credit history is, why it is so important for banks and what to do if you plan to take out a large loan, but there is no credit history.

In the following articles we will tell you:

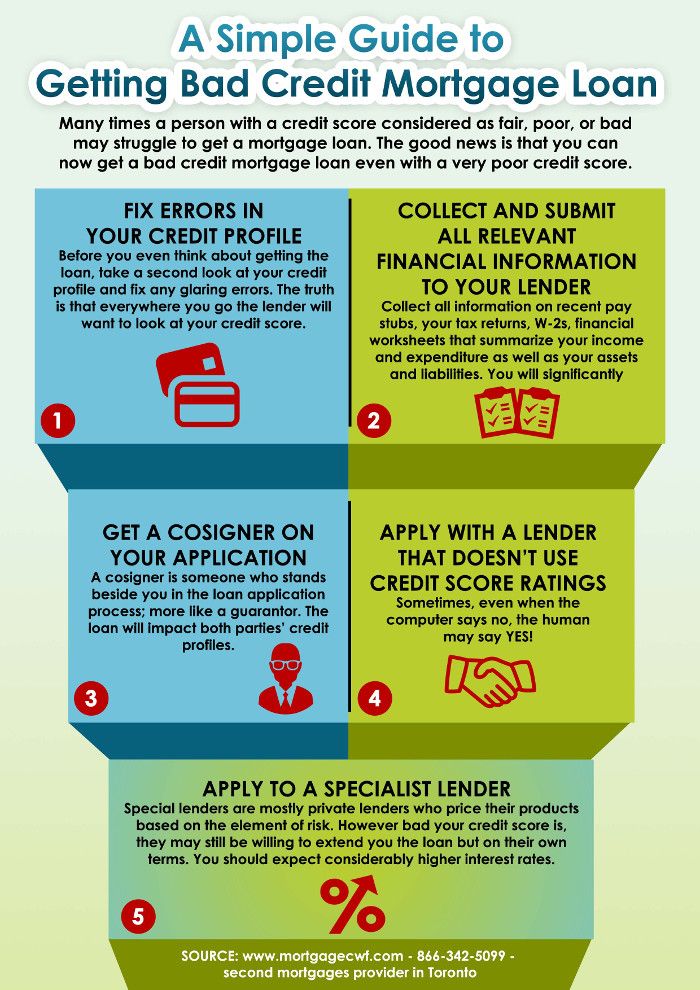

Obviously, if you are planning to buy a car on credit, you need to have an impeccable history. After all, it is unlikely that a bank will provide financial assistance to an insolvent or dishonest person. It is this information that is the key parameter for the bank manager, on the basis of which he can refuse or approve the application. However, even if you receive a negative answer, do not despair. As they say, there are no hopeless situations. Almost any issue can be positively resolved if you make certain efforts and confidently go towards the intended goal. Below we will consider how to get a car loan with a bad history, what options are available to improve it, and what needs to be done to buy a new or used car on favorable terms with a minimum of risks and hassle.

Below we will consider how to get a car loan with a bad history, what options are available to improve it, and what needs to be done to buy a new or used car on favorable terms with a minimum of risks and hassle.

Credit history is an indicator of the client's solvency. This is information about every person who has ever taken a loan from a bank. It is stored in the database of credit histories of all borrowers, without exception, and when considering an application, it is a key criterion for making a positive decision or refusal. Depending on how the previous loan was repaid, credit history can be good or bad. In the first case, it is assumed that there are no current delays in mandatory payments. The client is solvent, as he has always paid his bills on time. In this case, the probability of obtaining a car loan on favorable terms is maximum.

Bad credit refers to monthly repayments that are irregular or delayed. Delays were both short-term up to 30 days, and long-term - up to several months. In any case, under such conditions, the possibility of obtaining a loan, like any other loan, is minimal. At the same time, the higher the degree of neglect (delays), the lower the likelihood of approval.

Delays were both short-term up to 30 days, and long-term - up to several months. In any case, under such conditions, the possibility of obtaining a loan, like any other loan, is minimal. At the same time, the higher the degree of neglect (delays), the lower the likelihood of approval.

There are several ways to improve your credit history. If the delays were due to objective reasons (illness, reduction, pandemic, etc.), it is necessary to provide the bank manager with documents confirming this or that situation when applying for a car loan. This may be a certificate of illness, temporary non-payment of wages, or something else.

If you plan to purchase a car in a few months or even next year, you can first take a small loan from the bank where you are going to receive a loan and pay it off quickly. There are many options for "quick money" even with a zero interest rate, if the specified amount is returned within one or two months. Prompt repayment of debt will have a positive impact on credit history.

Prompt repayment of debt will have a positive impact on credit history.

Another important fact that affects the credit history is the absence of delays in utility and other obligatory payments. Therefore, try to pay off all debts on all accounts before applying. And it is better to do it in advance, and make payments on time for several months.

When there is no desire or time to improve your financial image, there are several legal options for how to get a bad credit car loan. Given that the bank in any case has money back guarantees in the form of collateral, the manager can approve the application if you agree to more stringent conditions:

Usually, this amount exceeds 50% of the total cost of the machine.

Usually, this amount exceeds 50% of the total cost of the machine.

An important point is the fact that, regardless of history, it is better to apply for a car loan at the bank to which your salary or pension is transferred. A good help for making a positive decision can be a deposit that increases the client's solvency.

The answer to the question of how to get a car loan without a credit history is quite simple. Contact the network of car dealerships PETROVSKY. We not only have a large selection of new models and used cars, but also the most loyal conditions for processing purchase transactions. Special programs, promotions and discounts will allow you to purchase a car with the maximum benefit without unnecessary costs and hassle.