Nowadays, it’s all too common to see news headlines on retirement, although they’re not as positive as we’d like.

The sad truth is that many people struggle to make ends meet once they retire. Some are shackled by mortgages or other debts they need to consider on top of their day-to-day expenses, as reflected by the latest retirement statistics.

In this article, we’ve gathered the most important stats on retirement to give you a better understanding of the current situation in the country, so read on if you’d like to know the particulars.

There are many expectations and misconceptions regarding the latest statistics about retirement. So, let’s take a closer look at some of the most important stats and facts pertaining to retirement in the United States that you should be aware of.

(Forbes)

According to Forbes’ latest retirement statistics by age, the average retirement age has increased over the years. Currently, it is 65 for men, whereas it’s slightly lower for women at 62.

Moreover, the average retirement age has increased steadily over the past two decades. Specifically, the same research from Forbes indicates that the average retirement age in 1992 was three years lower than today - 62 for men and 59 for women.

Though most people are retiring later in life than ever before, studies also show that job satisfaction is quite high among Americans at the moment, in spite of the troubling state of the economy.

(The Motley Fool)

Regarding how much one should save for retirement, many tend to focus on the total amount. However, it’s much more important to ensure that you can secure a stable income over the full length of your retirement. A financial advisor is likely to recommend you secure 80% of your annual pre-retirement income if you wish to have comfortable and stress-free golden years.

Of course, this rule isn’t set in stone. Those who are debt-free and don’t plan on any major spending in their retirement can make do with less, whereas those who might have significant expenses should save more. This can include anything from the services of an elder law specialist or a caregiver, to paying off a mortgage or other debt.

In fact, American retirement savings statistics show that many baby boomers still have a lot of outstanding mortgage and nonmortgage debt that they’ll likely have to keep paying off even after they retire.

(The Motley Fool)

Speaking of expenses, statistics on retirement in the United States indicate that the average retiree has to set aside roughly $4,300 on healthcare every year. In fact, healthcare costs can easily become your sole biggest expense.

As such, it’s important to take healthcare costs into account when planning your retirement and to save up as much as possible in order to account for both the predictable and unpredictable costs you might face.

(Statista)

Research conducted by Statista shows that the number of retirees who rely on Social Security benefits has increased significantly over the past decade, reaching almost 47.3 million in 2021, up from 46. 3 million in 2020.

3 million in 2020.

This number has seen a steady year-on-year increase of roughly 1 million. For comparison, it’s noteworthy that in 2010, only 34.6 million retirees were receiving Social Security benefits from the state. The latest data bears no indication that this trend will change, and Social Security expenditure is expected to keep rising in the coming years.

(Statista)

According to data from Statista, the number of military retirees in 2022 is approximately 2.2 million, and it's expected to rise to over 2.3 million over the next 10 years. As the number of military retirees increases, so will the value of total benefits paid out to former military personnel.

(CNBC)

Retirement income statistics from April 2022 indicate that an American retiree can expect to receive an average of $1,666 in monthly Social Security benefits. Of course, some will receive more and some less, depending on a number of factors.

In any case, it’s obvious that Americans can’t rely solely on Social Security if they wish to have a comfortable retirement. After all, the Social Security Administration itself stated that Social Security isn’t meant to replace a full income. This is why it’s important to start saving on time, build up your assets, and spare yourself potential financial headaches later in life.

(US Census Bureau)

According to data from the US Census Bureau, the average mean annual retirement income for retirees aged 65 and above was $73,288. Notably, there was a big income gap between those who are 65 to 74 years of age and those 75 or older - $84,153 and $58,684, respectively.

Furthermore, the median retirement income for the 65-74 age bracket is $56,632, whereas it’s only $37,335 for those 75 or older.

(CNBC)

While the average retirement age has risen over the years, the COVID-19 pandemic dealt a considerable blow to both the economy and to people’s morale.

The latest US retirement statistics show that as many as 36% of Americans feel that they’ll never be able to retire and will instead have to work their entire lives. Meanwhile, 59% of study respondents said they were aware they would simply have to keep working past the expected retirement age.

(Bankrate)

One of the more concerning retirement facts, as per a recent survey by Bankrate, is that over half of Americans are contributing the same amount or less to their retirement funds compared to the previous year. Specifically, 35% said they were “significantly behind” on their savings, whereas the other 20% felt they were only “somewhat behind.”

The main reason for this, as pointed out by the survey responders, is the skyrocketing level of inflation. Specifically, the US inflation rate in 2022 is a whopping 8.3%, compared to 1.2% in 2020 and 4.7% in 2021.

(Statista)

According to a survey from Statista, 60% of Americans think Social Security will be their primary source of income once they retire. Of course, that is not to say that they’d be relying solely on state assistance without any savings of their own, as most Americans have 401(k) plans, IRAs, or other savings accounts.

However, 33% of responders expect that they will still have to keep working after they retire in order to be able to live comfortably.

(Statista)

Despite some discouraging trends, 401(k) statistics show that the total nationwide asset value in 401(k) plans surpassed $7.2 trillion in 2021, up from $6.7 trillion in 2020, marking a steady upward trend since 2018. Of the mentioned $7.2 trillion, $4.8 trillion was invested in mutual funds, and the remaining $2.4 trillion was put toward other investments.

In addition, the total value of assets in Individual Retirement Accounts was $11. 8 trillion in 2021. Much like 401(k) plans, the value of traditional IRAs has been rising steadily. Since 2018, the total value has only been going up.

8 trillion in 2021. Much like 401(k) plans, the value of traditional IRAs has been rising steadily. Since 2018, the total value has only been going up.

(Statista)

The latest retirement savings statistics indicate that 77% of Americans have a 401(k) plan. This makes it the most popular defined contribution retirement plan, and the most popular retirement plan overall. Moreover, 67% of respondents also said they’re saving for retirement by putting money into regular savings accounts.

Traditional and Roth IRAs are less popular, at 26% and 25%, respectively. On top of that, only 30% of Americans invested in certificates of deposit, 25% plan to rely on their insurance policy, and 24% also rely on taxable investment accounts.

(SeniorLiving.org)

People who were born in the baby boomer generation are now either in retirement or fast approaching their golden years. In fact, roughly 10,000 baby boomers are turning 65 every day, and all baby boomers will have passed that age by 2030.

In fact, roughly 10,000 baby boomers are turning 65 every day, and all baby boomers will have passed that age by 2030.

Baby boomers comprise 28% of the US population. Notably, as many as 40% of them said that they never plan to retire. It’s not difficult to understand this outlook, as high turnover rates among younger generations tend to leave a lot of positions open.

(Transamerica Center for Retirement Studies)

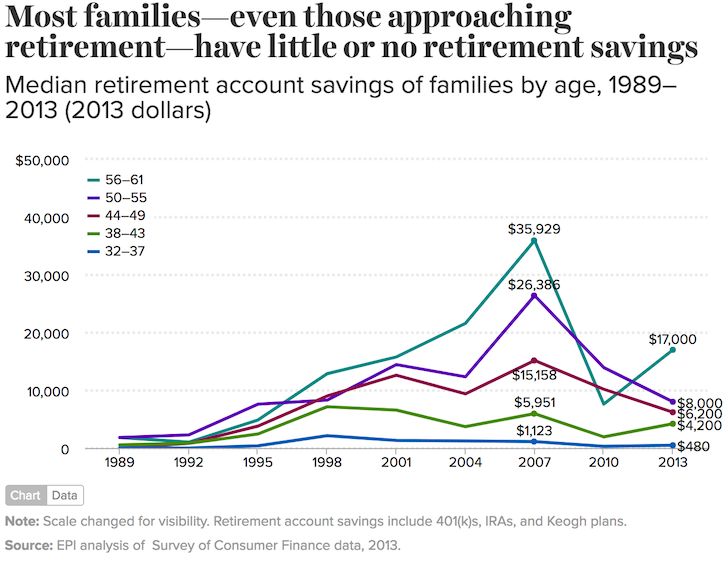

Baby boomer retirement statistics indicate that the median amount of retirement savings among the members of this generation is only $202,000, which would indicate an annual income of only $8,000 for those who follow the 4% rule.

However, 45% of baby boomers reported having saved up more than $250,000, but this is still a far cry from securing the generally recommended 80% of one’s pre-retirement income on an annual level.

(CNBC)

One of the more concerning statistics regarding retirement in the US is the fact that the average baby boomer still has almost $200,000 in mortgage debt, and that doesn’t include an additional $25,812 of nonmortgage debt.

A generation that’s rapidly approaching retirement years, baby boomers are under considerable pressure to pay off their debts as quickly as possible so that they don’t pose an additional burden on their savings in retirement.

Preparing adequately for retirement in the US is getting more and more challenging in these precarious economic circumstances. These retirement statistics attest to that, providing ample insight into the problems and obstacles that millions of future retirees will have to face.

On the bright side, keeping these factors in mind can help ensure you take all the steps needed to make your golden years as comfortable and peaceful as possible.

Q:

How much does the average person have when they retire?

A:

According to data from Vanguard, the average retirement account balance for those 65 and older is $279,997, and it’s $256,244 for those in the 55-64 age bracket who are approaching retirement.

Q:

What is the average age most people retire?

A:

According to the latest data, the average retirement age in the United States is 65 for men and 62 for women. The average retirement age has increased over the past two decades, as it was 62 for men and 59 for women in the early 1990s.

Q:

What is the average nest egg in retirement?

A:

The average retirement nest egg in the US in 2022 is $86,869, which is 11% lower than the previous year’s average of $98,800.

Q:

What is the average retirement income in the US?

A:

According to retirement statistics from the US Census Bureau, the average mean annual income for retirees over the age of 65 is $73,288. However, the average mean income for those in the 65-74 age bracket is significantly higher than it is for those over the age of 75 - $84,153 compared to $58,684.

As employers contend with growing numbers of younger employees quitting in the great resignation, the COVID-19 recession and gradual labor market recovery has also been accompanied by an increase in retirement among adults ages 55 and older.

As of the third quarter of 2021, 50.3% of U.S. adults 55 and older said they were out of the labor force due to retirement, according to a Pew Research Center analysis of the most recent official labor force data. In the third quarter of 2019, before the onset of the pandemic, 48.1% of those adults were retired. In regard to specific age groups, in the third quarter of 2021 66.9% of 65- to 74-year-olds were retired, compared with 64.0% in the same quarter of 2019.

The leading edge of the Baby Boomer generation reached age 62 (the age at which workers can claim Social Security) in 2008. Between 2008 and 2019, the retired population ages 55 and older grew by about 1 million retirees per year. In the past two years, the ranks of retirees 55 and older have grown by 3.5 million.

How we did this

The COVID-19 recession caused millions of Americans to leave the labor force, including many older workers. The recovery began in April 2020, and labor markets have tightened. Retirement is not necessarily permanent, as some retired adults may subsequently reenter the labor market. The track of the retirement rate sheds some light on how durable or long-lasting the employment disruptions are proving to be among older adults.

Retirement is not necessarily permanent, as some retired adults may subsequently reenter the labor market. The track of the retirement rate sheds some light on how durable or long-lasting the employment disruptions are proving to be among older adults.

The share of retired U.S. adults is derived from the monthly Current Population Survey (CPS), conducted by the U.S. Census Bureau for the Bureau of Labor Statistics. The CPS is the nation’s premier labor force survey and is the basis for the monthly national unemployment rate released on the first Friday of each month. The CPS is based on a sample survey of about 70,000 households. The estimates are not seasonally adjusted.

“Retired” in this analysis is based on labor force status. Those who cite “retired” as the reason for not being in the labor force (neither employed nor seeking work) constitute the retired population. This is a moment-in-time measure, and increases reflect the net change of adults moving both into and out of “retirement” due to changes in labor force participation.

The CPS microdata files analyzed were provided by the IPUMS at the University of Minnesota.

The COVID-19 outbreak has affected data collection efforts by the U.S. government in its surveys, especially limiting in-person data collection. This resulted in about an 8 percentage point decrease in the response rate for the CPS in September 2021. It is possible that some measures of retirement and labor market activity and its demographic composition are affected by these changes in data collection.

The large impact of the COVID-19 recession – February 2020 to April 2020 – on retirement differs from recent recessions and marks a significant change in a long-standing historical trend toward declining or steady retirement rates among older adults.

During the Great Recession and its aftermath, retirement rates declined. By the third quarter of 2010, 48% of adults ages 55 and older were retired, down from 50% in the same quarter of 2007. The prior recessions did not disrupt the longer-running trend of rising labor force participation and declining retirement among older Americans that began around 1997. Gradually declining retirement reflected in part rising education levels among older Americans as well as gains in their health. In addition, there were policy changes in Social Security that may have impacted retirement decisions. (For example, in 2000 the earnings test on benefit claimants was no longer applied to those who had reached full retirement age.)

Gradually declining retirement reflected in part rising education levels among older Americans as well as gains in their health. In addition, there were policy changes in Social Security that may have impacted retirement decisions. (For example, in 2000 the earnings test on benefit claimants was no longer applied to those who had reached full retirement age.)

The financial context in which older adults are making retirement decisions during the pandemic is markedly different from the Great Recession. During that period – December 2007 to June 2009 – there was a steep decline in the value of financial assets as well as home prices. The resulting loss of wealth induced some older workers to remain in the labor force and postpone retirement. In contrast, household wealth has been rising since the onset of the pandemic. House prices have been rising in most markets. The stock market did have a sharp sell-off in March 2020 but reached new record highs by August 2020.

The retirement uptick among older Americans is important because, until the pandemic arrived, adults ages 55 and older were the only working age population since 2000 to increase their labor force participation. Labor force participation for the entire working age population declined from an annual average of 67% in 2000 to 63% in 2019. This partly reflects a steep drop in participation among 16- to 24-year-olds (66% to 56%) as young people increasingly pursued schooling rather than employment. Participation has also been declining this century among the “prime working age” population, those ages 25 to 54. The overall decline in labor force participation would have been larger if adults 55 and older had not increased their labor force participation (from 32% in 2000 to 40% in 2019).

Labor force participation for the entire working age population declined from an annual average of 67% in 2000 to 63% in 2019. This partly reflects a steep drop in participation among 16- to 24-year-olds (66% to 56%) as young people increasingly pursued schooling rather than employment. Participation has also been declining this century among the “prime working age” population, those ages 25 to 54. The overall decline in labor force participation would have been larger if adults 55 and older had not increased their labor force participation (from 32% in 2000 to 40% in 2019).

It is unclear whether the pandemic-induced increase in retirement among older adults will be temporary or longer lasting. Newly published labor force projections from the Bureau of Labor Statistics suggest it will be temporary. BLS projects large increases in labor force participation among older adults from 2020 to 2030, with nearly 40% of 65- to 69-year-olds being in the labor force by 2030, up from 33% in 2020.

The recent retirement spike has not been uniform across demographic groups. The share of older White adults who are retired increased 3 percentage points from Q3 of 2019 to Q3 of 2021. The retirement rate of older Black adults did not significantly increase. The retirement rate of U.S.-born adults ages 55 and older rose 3 points from 2019 to 2021, while the rate for their foreign-born peers was unchanged.

Retirement among those 55 and older who have completed at least a bachelor’s degree rose 3 percentage points over this period. Among older adults who have a high school diploma or less the rate increased 1 point. The retirement rate increased for older adults living in metropolitan areas (2 points) and also increased for older adults in rural areas (1 point).

Richard Fry is a senior researcher focusing on economics and education at Pew Research Center.

POSTS BIO TWITTER EMAIL

A selection of the most important documents upon request Retirement of a woman born in 1966 (regulations, forms, articles, expert advice and much more).

free of charge at 2 days

Ready-made solution: What a personnel officer needs to know about employees of pre-retirement age In the table given in the Letter dated 12/18/2018 N 21-2/10/P-9349, the age is indicated when men and women begin to be classified as citizens of pre-retirement age, and the years of their birth for calculations in 2019 - 2028. In 2021, the generally established age at which the right to an insurance pension arises for women is 58 years, for men - 63 years. Therefore, pre-pensioners in 2021 are women born in 1964 (except for those who are assigned an old-age pension), 1965, 1966, 1967 and 1968, men - in 1959 (except for those who are assigned an old-age pension), 1960, 1961, 1962 and 1963

In 2021, the generally established age at which the right to an insurance pension arises for women is 58 years, for men - 63 years. Therefore, pre-pensioners in 2021 are women born in 1964 (except for those who are assigned an old-age pension), 1965, 1966, 1967 and 1968, men - in 1959 (except for those who are assigned an old-age pension), 1960, 1961, 1962 and 1963

Register and get trial access to the ConsultantPlus system for free for 2 days

Article: Downsizing (staff) in an institution - how to do it right?

(Ivanova I.E.)

("Head of a budgetary organization", 2022, N 1) The dashes in this and other columns are associated with the non-approach of the retirement age in a given year. For example, for women born in the 2nd half of 1965, the retirement age comes in 2022 (in the 1st half). And all women born at 1966, retire a year later - in 2024. Thus, no one will retire in 2023. We put a dash.

Ruling of the Constitutional Court of the Russian Federation of March 16, 2006 N 69-O

"On the refusal to accept for consideration the complaint of citizen Gusak Nikolai Aleksandrovich about the violation of his constitutional rights by paragraphs 1 and 2 of Article 346. 26 of the Tax Code of the Russian Federation and paragraph 3 of Article 28 of the Federal Law "On Compulsory Pension Insurance in the Russian Federation", the Constitutional Court of the Russian Federation in the said Determination came to the conclusion that, having recognized individual entrepreneurs as participants in the compulsory pension insurance system and giving them the opportunity to independently form their pension rights, the federal legislator, taking into account the specifics entrepreneurial income introduced a rule for them to pay insurance premiums for compulsory pension insurance in the form of a fixed payment, i.e. in a fixed amount, and determined its minimum amount, mandatory for payment; for a labor pension depending on the receipt of income; payment by individual entrepreneurs for themselves of insurance premiums calculated according to rules different from those provided for persons making payments to individuals does not mean a violation of the constitutional principle of equality.

In addition, as the Constitutional Court of the Russian Federation pointed out, by virtue of Articles 22 and 33 of the Federal Law "On Compulsory Pension Insurance in the Russian Federation", insurers making payments to individuals do not have to pay insurance premiums at the rates established by these articles to finance the funded part of labor pension for persons of a certain age group, namely 1966 years of birth and older (in 2002-2004, insurance contributions to finance the funded part of the labor pension were not payable for men born in 1952 and older and women born in 1956 and older), and, accordingly, these persons are entitled to the funded part of the labor pension do not purchase; establishing such a differentiation in relation to the collection of insurance premiums to finance the funded part of the labor pension (depending on the age of the insured person), the federal legislator proceeded from the need to ensure, by the time the retirement age is reached and the pension is awarded, the formation of pension savings sufficient to pay this part of the pension, which requires relevant time period; thus, individual entrepreneurs 1966 years of birth and older (and in 2002 - 2004 - men born in 1952 and older and women born in 1956 and older) must pay insurance premiums to the budget of the Pension Fund of the Russian Federation in the form of a fixed payment in the amount established by Article 28 of the Federal Law "On Compulsory Pension Insurance in the Russian Federation", only in the part directed to finance the insurance part of the labor pension.

A selection of the most important documents upon request Retirement age for women BORN in 1965 (regulations, forms, articles, expert advice and much more).

Register and get trial access to the ConsultantPlus system for free to 2 days

"Commentary to the Federal Law of December 28, 2013 N 400-FZ "On insurance pensions"

(line by line)

(Mironova T.K., Arzumanova L. L., Peshkova (Belogortseva) Kh.V., Rozhdestvenskaya T.E., Bondareva E.S., Gusev A.Yu., Luminarskaya S.V., Menkenov A.V., Rothko S.V., Sapozhnikova N.I., Chernus N. Yu., Elaev A.A., Zagorskikh S.A., Kotukhov S.A., Sokolov R.A.)

L., Peshkova (Belogortseva) Kh.V., Rozhdestvenskaya T.E., Bondareva E.S., Gusev A.Yu., Luminarskaya S.V., Menkenov A.V., Rothko S.V., Sapozhnikova N.I., Chernus N. Yu., Elaev A.A., Zagorskikh S.A., Kotukhov S.A., Sokolov R.A.)

(Prepared for the ConsultantPlus system, 2021) Thus, an additional pension benefit has been introduced for this category of citizens, it concerns men who were born at 1959 and 1960, and women born in 1964 and 1965. Men born in 1959 and 1960, as a general rule, should have retired in 2020 and 2021 at the age of 61 and 62. However, the newly introduced benefit allowed them to retire six months earlier. Women born in 1964 and 1965 were due to retire in 2020 and 2021 at ages 56 and 57, but they could also retire six months earlier.

Register and get trial access to the ConsultantPlus 9 system0013 free for 2 days

Article: Downsizing (staff) in an institution - how to do it right?

(Ivanova I.E.)

("Head of a budgetary organization", 2022, N 1) The dashes in this and other columns are associated with the non-approach of the retirement age in a given year.