Should you fund your retirement even after you retire? The idea may seem counterintuitive, but for retirees still working part time, continuing to seed an individual retirement account can ensure that they have enough money to enjoy retirement long into the future. Here’s what you should know about contributing to an IRA after you’re retired.

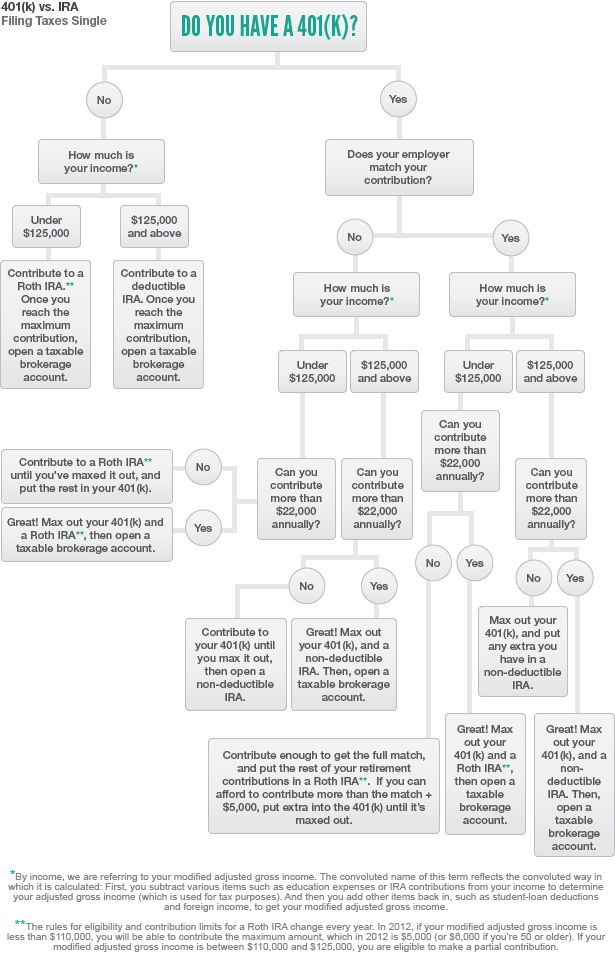

Can you contribute to your IRA after retirement?Yes, you can contribute to an IRA after you’re retired, but you’ll need to have some amount of “earned income” in order to do so. Earned income comes in the form of salaries, wages, tips or bonuses, so you’ll likely need to have at least some kind of part-time work. Income from things such as dividends, interest or Social Security does not qualify as earned income.

If you are retired and your spouse has earned income, he or she can contribute to their own IRA and also make what is called a spousal contribution to your IRA.

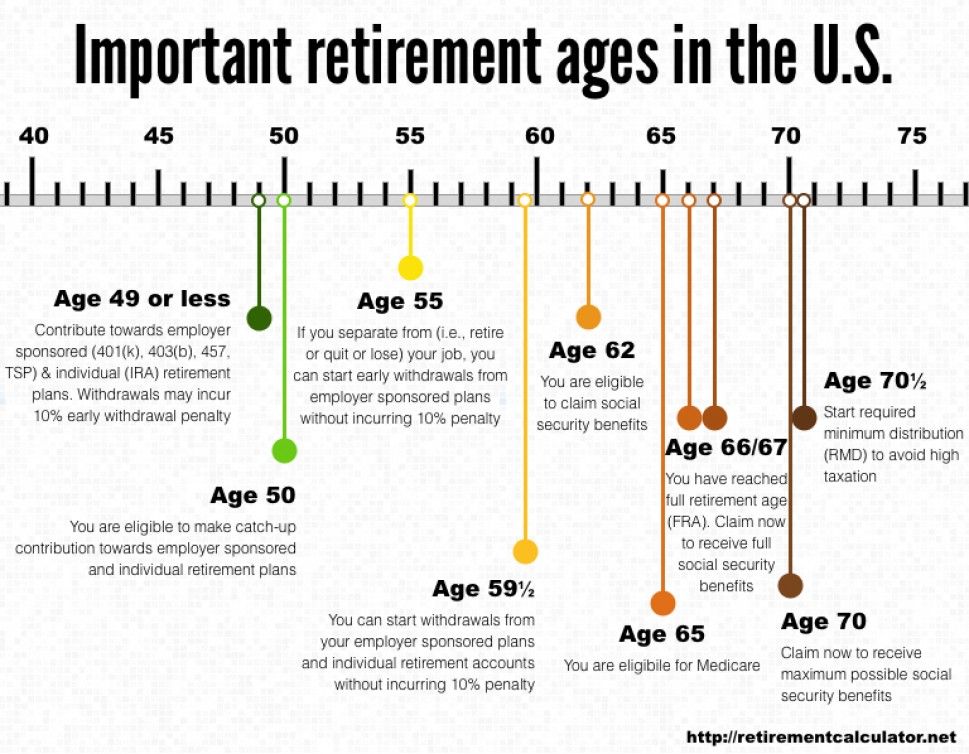

Prior to the passing of the SECURE Act in 2019, contributions to traditional IRAs were banned beyond age 70 ½, but that is no longer an issue. You can now contribute to a traditional or Roth IRA no matter your age.

“If it doesn’t harm the current lifestyle, having extra for the future is seldom a bad thing,” says Ilene Davis, a certified financial planner in Cocoa, Florida, and author of “Wealthy by Choice: Choosing Your Way to a Wealthier Future.”

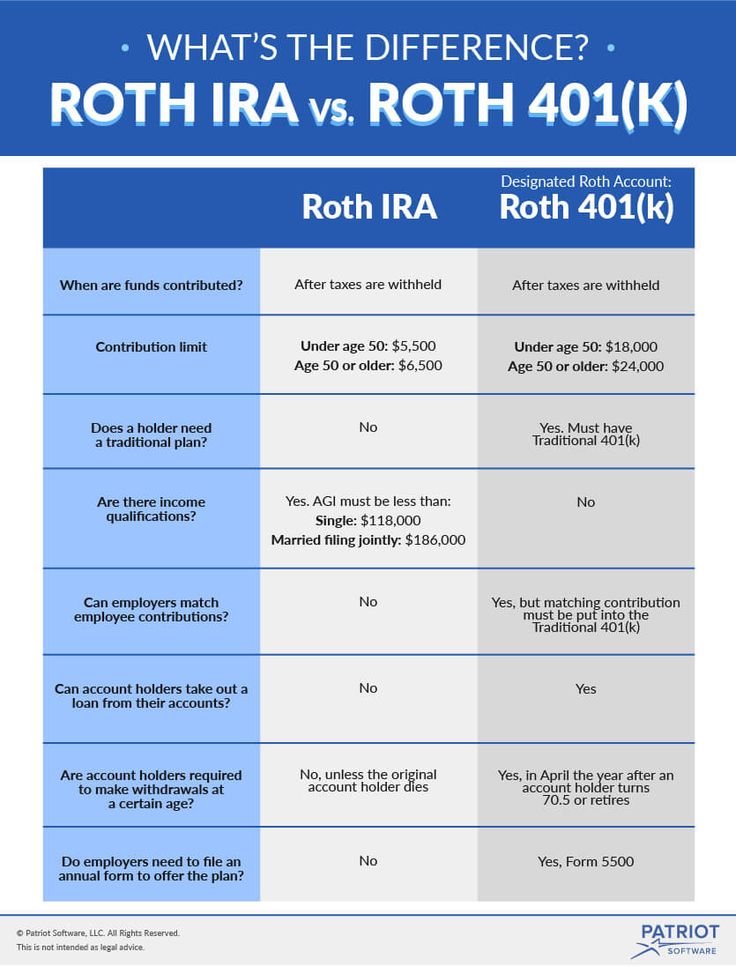

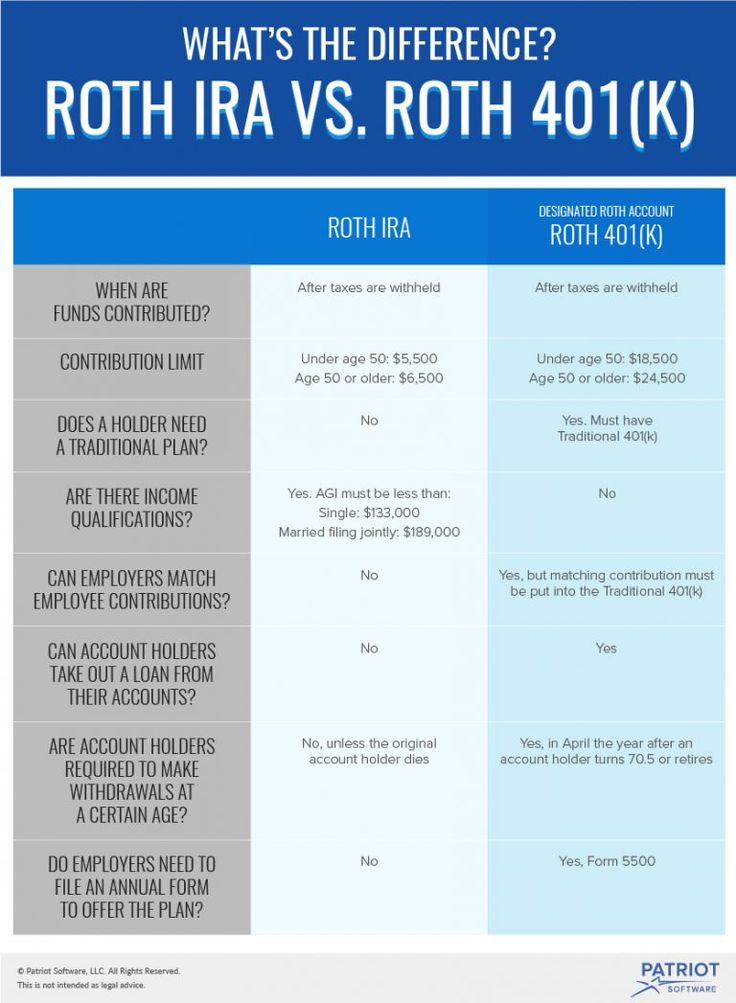

Post-retirement IRA contribution limitsIRA contribution limits are the same during retirement as they are the rest of your life. You can contribute up to 100 percent of your earned income or $6,000 (in 2022) for people under age 50, whichever is less. Those age 50 or older can contribute an additional $1,000 as a catch-up contribution for a total of $7,000.

For example, say you earned $3,000 working a part-time job during the year. Your IRA contribution would be limited to $3,000 because that was all you had in earned income. The limits are the same whether you’re contributing to a traditional or Roth IRA.

The limits are the same whether you’re contributing to a traditional or Roth IRA.

Contributing to an IRA will mean you have less money to live on today.

Contributing to an IRA will mean you have less money to live on today.It doesn’t make sense to invest in an IRA in retirement if you can’t afford it. But if you can afford it, saving more money in tax-deferred accounts is beneficial, especially if you live a long time.

“It’s always optimal to save more for retirement so that you have more savings as you spend money through retirement,” says Ken Hevert, who is the business leader for digital products and customer experience at Fidelity Investments.

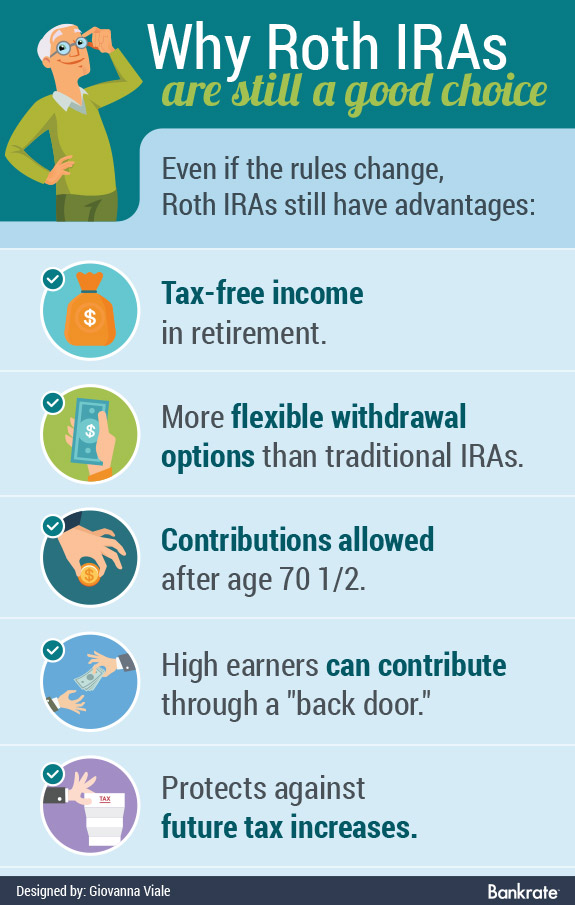

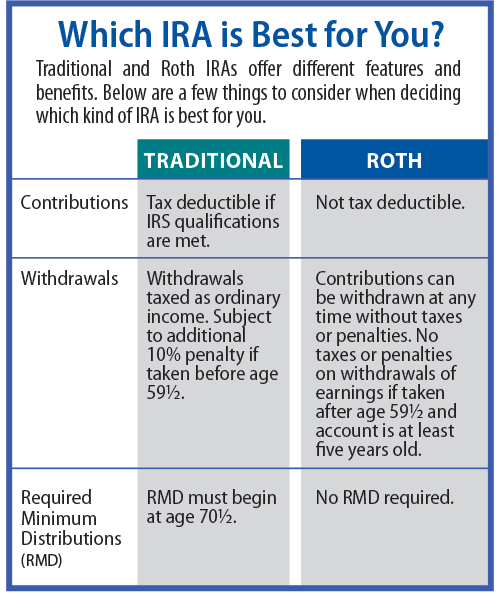

Roth vs. traditional IRAWhether to use a Roth or a traditional IRA for those your contributions depends on your tax situation. Hevert favors the Roth because there is no required minimum distribution, or RMD, so funds can continue to grow throughout retirement and can be tapped later in retirement or left to heirs in an estate.

When contributing to a traditional IRA on a pretax basis, you get the benefit of an upfront tax deduction. But some advisors don’t see the point of this strategy since the benefit is temporary.

“There could be some benefit to contributing to a traditional IRA if you are trying to save some dollars in taxes and you are still working,” says Richard E. Reyes, a certified financial planner at Wealth and Business Planning Group in Maitland, Florida. “But I don’t really find that too appealing because it will be taxed shortly when you begin taking distributions.”

“But I don’t really find that too appealing because it will be taxed shortly when you begin taking distributions.”

If you had a SIMPLE IRA or SEP IRA but have retired from that job, you can still open an IRA through investment firms such as Vanguard or Fidelity.

© Copyright 2022 Bankrate, Inc. All rights reserved.

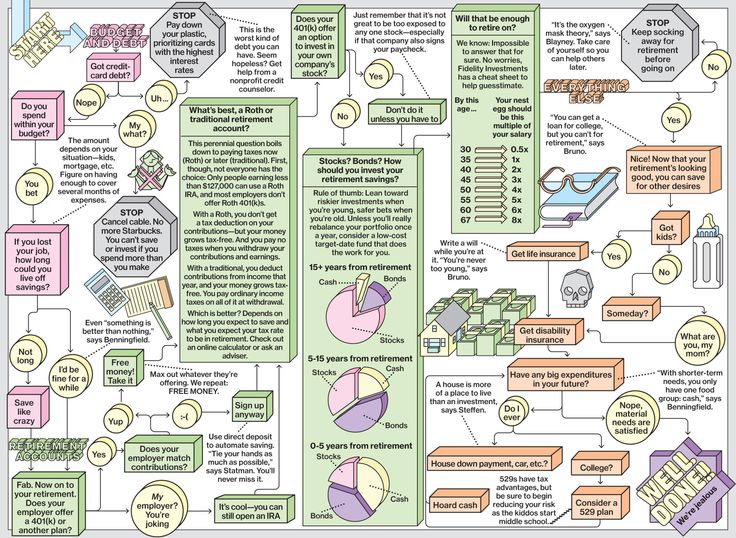

Retirement planning is an important part of any individual's financial life. Not only does it require money, but you also need to know your long-term goals. Ask yourself when you'd like to retire and consider how much money you'll need to maintain your lifestyle.

There are also some other considerations, such as whether you'll stop working completely or if you intend to supplement your retirement income with a part-time or freelance job.

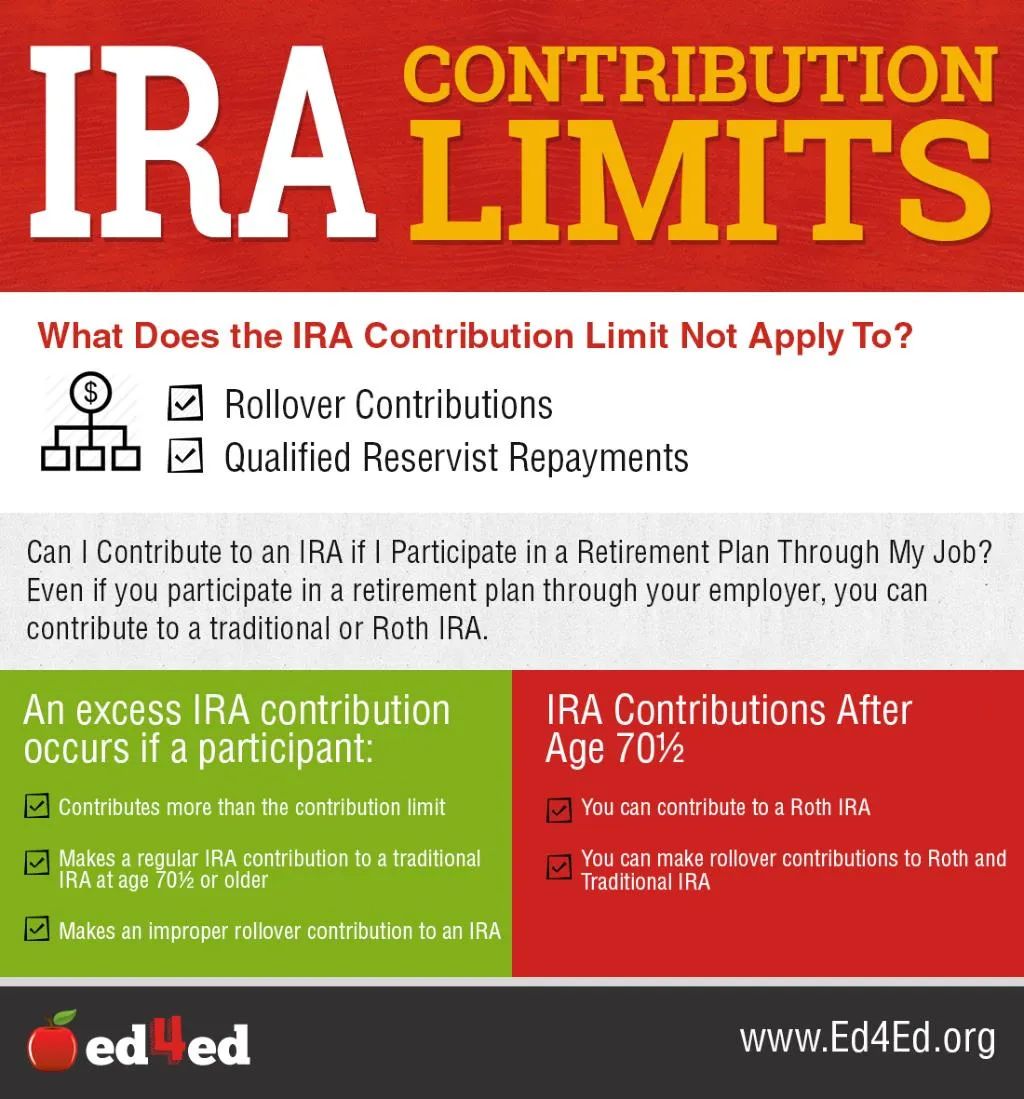

The accounts you have during your retirement will also play into how you're going to plan for that key point in your life. You may have regular interest-paying accounts like a savings account or a certificate of deposit (CD). And then there are special retirement accounts. For instance, you may participate in a 401(k) sponsored by your employer, you may fund your own individual retirement account (IRA), or both. But what are the rules about funding these accounts—especially your IRA?

In this article, we look at whether you can continue to fund your IRA and what the consequences are if you do.

Whether you can continue to fund an IRA primarily depends on if you have any sort of earned income after you retire. This includes wages, salaries, tips, bonuses, commissions, earnings from self-employment, as well as long-term disability and union strike benefits. Keep in mind that you cannot contribute anything from other sources, such as capital gains, dividends, or investment interest.

But remember, IRAs fall into two different general categories:

But the contributions are made with after-tax dollars.

But the contributions are made with after-tax dollars.Now let's take a look at what it means if you fund either of these accounts after you retire.

Continuing to contribute to a traditional IRA is possible even if you're officially retired but still work or perform services of any sort that you're paid for and can document or report on your tax return.

Remember that earned income does not include certain forms of compensation, including those from a pension, an annuity, or Social Security. It also doesn't include investment income or earnings generated by assets. This means that the money you contribute has to be earned from the sweat of your brow, so to speak.

Under the terms of the SECURE Act of 2019, all retirees can now contribute to traditional IRAs if they earn income. This means that the previous contribution cutoff age of 70½ no longer applies; however, holders of traditional IRAs must start taking required minimum distributions (RMDs) at age 72. Also, note that if you were born before July 1, 1949, you must still begin taking RMDs at age 70½.

Also, note that if you were born before July 1, 1949, you must still begin taking RMDs at age 70½.

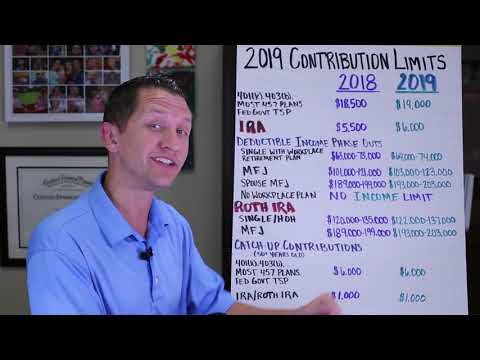

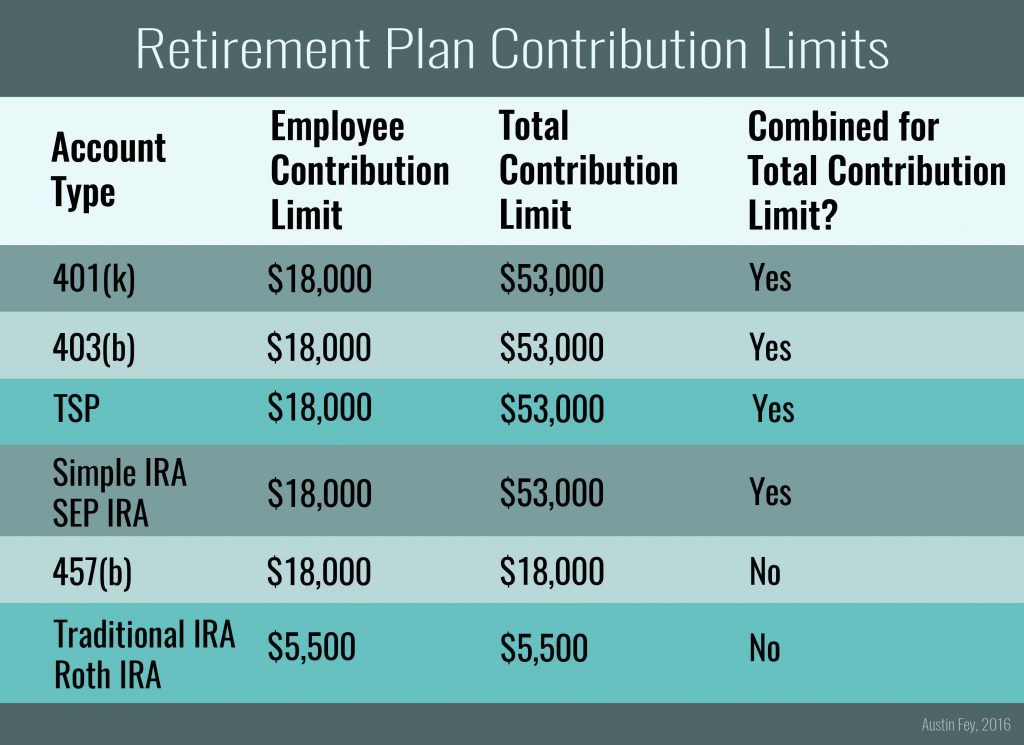

No matter your age or employment status, you can never exceed the annual contribution limits set by the IRS for both types of IRAs. For 2022, it's $6,000 a year, or $7,000 if you’re age 50 or over. For 2023, it is $6,500 and $7,500, respectively.

A Roth IRA affords a lot more flexibility. No matter how old you are, you can continue to contribute to your Roth IRA as long as you’re earning income—whether you receive a salary as a staff employee or 1099 income for contract or freelance work. On the flip side, you never have to take distributions from the account either.

Again, the deposits must be made with earned income: wages, fees, etc. So the $1,000 you got paid for a consulting job would be eligible, while your monthly $1,000 Social Security benefit doesn't count.

Of course, you aren't allowed to contribute more than the amount you have earned that year. Also, your modified adjusted gross income (MAGI) cannot exceed the general, annual income limits that affect whether you can contribute to a Roth IRA at all—less than $214,000 for married couples filing jointly, but under $144,000 for single taxpayers in 2022. These limits increase for married couples and single filers to $228,000 and $153,000 for the 2023 tax year.

Also, your modified adjusted gross income (MAGI) cannot exceed the general, annual income limits that affect whether you can contribute to a Roth IRA at all—less than $214,000 for married couples filing jointly, but under $144,000 for single taxpayers in 2022. These limits increase for married couples and single filers to $228,000 and $153,000 for the 2023 tax year.

The full retirement age for individuals born after 1960, at which point they can begin collecting full Social Security retirement benefits.

Funding an IRA during retirement has both benefits and drawbacks. And there's no hard-and-fast rule as to whether it's a good idea. After all, it all depends on your own personal situation, so it's up to you to decide whether contributing to your account after you retire is the right move for you.

The main advantage of contributing to your IRA during retirement is that you'll be padding your nest egg. Doing so can allow you to save up a nice amount of money. If you play your cards right, you can accumulate some additional interest on this sum and have more down the road.

Doing so can allow you to save up a nice amount of money. If you play your cards right, you can accumulate some additional interest on this sum and have more down the road.

If you're disciplined enough, saving more may help you spend less during retirement. Setting aside and budgeting for your IRA contributions during retirement can help you cut down other expenses. Maybe you can reduce that daily coffee run to just once or twice a week, or skip it altogether and put that money into your IRA for a few years.

If you choose to fund a traditional IRA, you can effectively lower your tax liability and put yourself into a lower tax bracket today. That's because these accounts are funded using pretax dollars. If you fund a Roth IRA after retirement, you can allow your savings to grow tax-free because you contribute after-tax money to it.

One of the main cons of contributing to an IRA during retirement is affordability. You're probably on a fixed income, even if you still have wages coming in. But it may not be that much. Putting aside money when you have limited funds may end up eating away at your monthly budget, which means you may have to make some sacrifices.

But it may not be that much. Putting aside money when you have limited funds may end up eating away at your monthly budget, which means you may have to make some sacrifices.

Contributing also chips away at any emergency fund you may be able to access. After all, you just don't know what's going to happen in the future. Putting your money into an IRA when you've already retired may mean locking it in for a certain amount of time. You may be better off putting that money into a savings account or a CD—something that's easy to liquidate if you need it in a hurry or for an emergency.

There is no age limit for opening an IRA, which means you can open an account even after you retire. Keep in mind that contributions can only come from earned income. You may also choose to transfer or roll funds over from an eligible retirement account you already have. There are also contribution limits that you must adhere to in order to avoid being charged a penalty by the IRS.

You can contribute and continue funding an IRA after retirement. This applies to both Roth and traditional IRAs. Prior to the passing of the SECURE Act, individuals could not contribute to traditional IRAs after age 70½. There were and are no age restrictions to contributing to a Roth IRA. If you fund your IRA after retirement, you still have to keep the maximum contribution limits in mind. If you go over these limits, you will be charged a penalty of 6% on the overfunded amount until it is corrected.

Yes, you can contribute to a Roth IRA after you retire. You can only contribute earned income to the account, which means you cannot set aside distributions from other retirement accounts, dividends, or interest income to the account. You may make contributions to your Roth IRA as long as you don't exceed the maximum annual contribution limits.

Yes, you can continue to contribute to an IRA even if you begin collecting Social Security benefits. But any money from your monthly benefits can't be contributed because Social Security isn't considered earned income. You can only contribute money to your IRA that you earn from a job.

But any money from your monthly benefits can't be contributed because Social Security isn't considered earned income. You can only contribute money to your IRA that you earn from a job.

Retirement planning is very important for anyone who wants to secure their financial future. You want to make sure that you're not going to struggle to keep up your lifestyle and standard of living. But what happens if you've already retired and no longer have any compensation? There is still a way that you can contribute.

If your spouse continues to work and has earned income, they can establish and fund a Roth IRA for you even if you're not actively working. This spousal Roth IRA must be in your name even if your spouse is the one making the contributions.

1. When will applications for Lonely Pensioner's Benefit start?

The pensioner does not have to apply for the allowance himself – the Social Insurance Board will pay the allowance after verification of the data.

2. How can I check who is registered (registered) in the same housing as me, since I don't remember this myself (a)?

To check the address of residence or to enter it in the Population Register, contact the city government of the part of the city where you live. nine0005

3. My grandson (my granddaughter) is registered in my apartment, who has not actually lived with me for many years. I live alone, am I eligible for benefits?

A pensioner who really lives alone, but a child, grandson, granddaughter or other person who does not actually live there is registered (registered) at the same address does not meet the conditions for receiving benefits.

4. My husband and I have been living in separate apartments for a long time, but we are not divorced. Am I eligible for benefits? nine0005

When paying benefits, it is not the family status of pensioners that is taken into account, but residence. If, according to the data of the Population Register, only you are registered in the apartment, you are entitled to the allowance.

5. If a private residential building has two owners and, according to the Population Register, they live at the same address, is there then a right to a pensioner living alone allowance?

If a private residential building has two owners and, according to the Population Register, they live at the same address, then they do not live alone, and therefore do not meet the conditions for receiving benefits. If the households located in the same building are listed as separate addresses in the Population Register, then the pensioner meets the conditions for receiving the allowance. nine0005

6. Is a pensioner living separately on the second floor of a private residential building entitled to receive pensioner living alone?

A pensioner who lives separately on the second floor of a private residential building, but at the same address with which, according to the Population Register, other residents are registered, does not meet the conditions for receiving benefits.

7. My address is inaccurate and the same as the name of the local government - for example, Audru parish - will I receive the pensioner's pension allowance? nine0005

Living alone means that a person is registered at the address of his place of residence. An address that matches the name of a local government is not considered a single residence.

8. How much pension can I receive in order to receive the Lonely Pensioner's Benefit? What amount of pension is taken into account - net or gross?

Pensioners are entitled to the allowance if the amount of the granted pension and its monthly net amount is less than 1.2 times the average old-age pension in Estonia. In 2021, the amount of 1.2 times the average pension is 636 euros. The net amount is the amount of the pension from which income tax has been deducted. nine0005

9. Are pensioners living in a care home (nursing home) entitled to benefits?

All persons who have reached retirement age and who are recipients of an old-age pension and receive a 24-hour care service, i. e. living in a care home (nursing home), whose pension is less than 636 euros, will receive a pensioner's pension allowance. Residential residence details from April 1st to September 30th will be verified and if the person meets the conditions for receiving benefits, they are eligible to receive benefits. nine0005

e. living in a care home (nursing home), whose pension is less than 636 euros, will receive a pensioner's pension allowance. Residential residence details from April 1st to September 30th will be verified and if the person meets the conditions for receiving benefits, they are eligible to receive benefits. nine0005

10. My parents live together in the same apartment and my father has been appointed guardian of my mother. Is the mother or father entitled to benefits?

In addition to pensioners living alone, guardians and wards also have the right to receive a pension living alone. This means that if both the guardian and the ward live in the same dwelling, and one or both of them are pensioners, they are entitled to the pensioner living alone allowance. If other tenants are registered (registered) at the same address as the guardian and the ward, the pensioner does not meet the conditions for receiving benefits. nine0005

11. Two old-age pensioners live at the same address, and one is registered for the other by a custodian on the basis of an agreement with the local government: are the custodian and ward entitled to benefits?

A guardianship contract does not give the right to a pensioner living alone if the guardian and the ward live together at the same address.

12. I have been living alone for some time, but in May I will be moving to a new place of residence, where I will also live alone. Do you check when you receive benefits that I was living alone before May? nine0005

If a pensioner lived alone in his first place of residence and later, when changing his place of residence, he lives alone again, he is entitled to the pensioner living alone allowance.

13. I live alone, go to work, and my pension is less than 636 euros - will I receive benefits or will my benefits not be paid due to work?

When paying benefits, it does not take into account whether a person who has reached retirement age is working or not. Earned income is not taken into account to encourage working at retirement age, so it doesn't matter if the pensioner is working full-time or part-time. The Lonely Pensioner's Allowance is not subject to income tax, and the allowance paid is not included in income when calculating the living allowance (indigence allowance). nine0005

nine0005

14. When will the benefit be paid?

If all conditions for receiving benefits are met between April 1 and September 30, benefits will be paid in October.

15. On the basis of what law is the allowance for a pensioner living alone?

The allowance of a pensioner living alone is regulated by the Social Welfare Act (Sotsiaalhoolekande seadus), articles 139 1 -139 3

can I put the data in the population register in order? nine0005

If a person is registered in the apartment who no longer lives there and who no longer has the right to use this dwelling as their place of residence, the owner of the apartment has the right to submit an application for changing the address data in the population register to the rural municipality or city government.

The owner of the dwelling has the opportunity to send a request to a specific city or rural municipality administration, depending on the location of the dwelling, in the following ways:

ee (an ID-card, an ID-card reader and the presence of PIN-codes from the ID-card are required).

ee (an ID-card, an ID-card reader and the presence of PIN-codes from the ID-card are required). I retired at the age of 55 due to work in the regions of the Far North. Now I am a full 66 years old, that is, I have been retired for the 12th year, but I continue to work. nine0005

Until August 1, 2015, my pension was indexed for inflation twice a year, from January 1 and April 1, as for all pensioners. And it was also recalculated from August 1 as for a working pensioner. The amount of the recalculation was significant, as it depended on the size of the employer's contributions to the funds, and at that time my average income was 50,000 rubles. . I have only three pension points at R74.27 - the annual recalculation is R222.81.

In five years, from 2015 to 2019, my pension grew by 1114.05 R, while before August 1, 2015, the increase was much larger. And this despite the fact that now my average income is 77,000 R, and from this amount the employer makes contributions to the funds.

I applied on this issue to the PFR department, to the hotline and in the chat on the fund's website. The answers are incomprehensible. As always in official papers, they contain a lot of references to documents with such long titles that by the time you read to the end, you no longer remember how it all began. Moreover, all subsequent editions of these documents are listed in brackets. Therefore, all hope is on you. nine0005

Explain in simple terms what needs to be done to raise pensions for people like me. I'm sure there is a way.

Viktor Mikhailovich

Viktor Mikhailovich, since 2016, pensions for working pensioners have indeed ceased to be indexed by a fixed percentage. If you are not satisfied with how your pension is being calculated now, the only option is to quit, wait for indexation, and then get a job again.

Alla Evgenyeva

lawyer

While you are working, you can increase your insurance pension only by recalculating it based on the earnings from which the employer paid insurance premiums to the PFR in the previous year.

So what? 08/05/19

Who will receive an increase in pensions from August 1 and how to receive an increase

Depending on the amount of earnings and insurance premiums paid, everyone is annually awarded pension points, which are called individual pension coefficients - IPC in the legislation. However, for working pensioners, no more than 3 IPC can be taken into account per year. nine0005

Art. 18 of the Law "On Insurance Pensions"

Recalculation is made automatically, without any applications, from August 1 of the year following the one in which the pensioner worked. So, from August 1, 2020, the recalculation of pensions for working pensioners is made taking into account the IPC, which were formed from the salary for 2019, from August 1, 2022, taking into account the IPC, which were formed from the salary for 2021.

If your average monthly earnings in 2019 amounted to 77,000 R, then in 2020, when recalculating your pension, the maximum possible number of IPC was taken into account - 3. And if you were earning, for example, 20,000 R, you could accumulate only 2,086 IPC - when recalculating, this amount would be taken into account. That is, less than 3 IPCs can be taken into account, but more can not. nine0005

And if you were earning, for example, 20,000 R, you could accumulate only 2,086 IPC - when recalculating, this amount would be taken into account. That is, less than 3 IPCs can be taken into account, but more can not. nine0005

If you continued to work until 2022 and your average monthly income did not decrease, then in 2020 and 2021 you accumulated 3 more points each.

To calculate the specific amount by which the size of the insurance pension will increase, you need to multiply the number of points by their value.

/guide/skolko-pensiya/

How to calculate the old-age pension

The cost of the IPC depends on the date of retirement: the recalculation uses the cost of points, which was taken into account in the initial calculation of the pension. nine0005

| Date of retirement | Cost of IPC | Maximum annual allowance |

|---|---|---|

| Before February 1, 2016 | 71. 41 R 41 R | 214.23 R |

| After February 1, 2016 | 74.27 P | 222.81 R |

| After February 1, 2017 | 78.28 P | 234.84 R |

| After April 1, 2017 | 78.58 R | 235.74 R |

| After January 1, 2018 | 81.49 P | 244.47 R |

| After January 1, 2019 | 87.24 P | 261.72 R |

| After January 1, 2020 | 93 P | 279 Р |

| After January 1, 2021 | 98.86 R | 296.58 R |

| After 1 January 2022 | 107.36 R | 322.08 P |

| After January 1, 2023 | 113.37 R | 340.11 Р |

| After January 1, 2024 | 119.61 R | 358.83 R |

Pension Until February 1, 2016

Cost of the IPK

71. 41 R

41 R

The maximum increase for the year

214.23 r

Pension after February 1, 2016

Cost IPK

74.27 r

The maximum size of the increase for the year

222.81 P

Pension after February 1, 2017

Cost IPK

78.28 R 9000

The maximum size is maximum size Relaxes for the year

234.84 r

Pension after April 1, 2017

Cost IPK

78.58 R

The maximum increase for the year

235.74 P

Pension after January 1, 2018

Cost of IPK

81.49 R

The maximum increase in the increase for the year

244.47 P

Pension after January 1, 2019 9000

Cost cost IPK

87.24 r

The maximum size of the increase for the year

261.72 R

Pension after January 1, 2020

Cost of IPK

9000 ° 9000

The maximum increase for the year

279 p

Pension after January 1, 2021

Cost of IPK

98. 86 R

86 R

The maximum increase for the year

296.58 R

Pension after January 1, 2022

Cost of IPK

107.36 R

The maximum size of the increase for the year

322.08 P

Pension after January 1, 2023

Cost IPK

113.37 P

The maximum increase for the year

340.11 P

Pension after January 1, 2020

Cost IPK

119.61 P

The maximum increase for the year

358.8 Thus, when recalculating in August 2020 the pension assigned before February 1, 2016, the maximum amount of the increase for a working pensioner will be 214.23 R. The same amount will be added when recalculating in August 2021 and 2022. Unfortunately, while you are employed, you will not be able to increase your insurance pension in any other way. nine0005

You can increase your pension after dismissal. According to the law, for pensioners who have left their jobs, the amount of the insurance pension is calculated taking into account the missed annual indexations, starting from the first day of the month that follows the month of dismissal.

According to the law, for pensioners who have left their jobs, the amount of the insurance pension is calculated taking into account the missed annual indexations, starting from the first day of the month that follows the month of dismissal.

hh. 3, 4, 6-8 st. 26.1 of the Law "On Insurance Pensions"

At the same time, based on the established recalculation procedure, a larger pension will actually be paid only three months after dismissal. For example, if a pensioner quits on December 31, 2020, then the amount of his insurance pension will increase from January 1, 2021, but he will receive an increased pension only from March 1, 2021. nine0005

If a pensioner gets a job again, he will have an increased pension - the amount that he received the day before he was hired.

Thus, in order to increase your pension, you can quit your job, wait for recalculation taking into account indexations from 2016 to 2021 and get a job again.

/ops-2020/

What you need to know about the funded pension in 2020

an increased pension.