Table of Contents

Table of Contents

How Social Security Is Taxed

How Much Untaxed Income?

Standard Deductions for Retirees

Tax Brackets for 2021 and 2022

The Bottom Line

By

Michelle P. Scott

Full Bio

Michelle P. Scott is a New York attorney with extensive experience in tax, corporate, financial, and nonprofit law, and public policy. As General Counsel, private practitioner, and Congressional counsel, she has advised financial institutions, businesses, charities, individuals, and public officials, and written and lectured extensively.

Learn about our editorial policies

Updated July 31, 2022

Reviewed by

Lea D. Uradu

Reviewed by Lea D. Uradu

Full Bio

Lea Uradu, J.D. is graduate of the University of Maryland School of Law, a Maryland State Registered Tax Preparer, State Certified Notary Public, Certified VITA Tax Preparer, IRS Annual Filing Season Program Participant, Tax Writer, and Founder of L.A.W. Tax Resolution Services. Lea has worked with hundreds of federal individual and expat tax clients.

Learn about our Financial Review Board

Fact checked by

Suzanne Kvilhaug

Fact checked by Suzanne Kvilhaug

Full Bio

Suzanne is a researcher, writer, and fact-checker. She holds a Bachelor of Science in Finance degree from Bridgewater State University and has worked on print content for business owners, national brands, and major publications.

Learn about our editorial policies

If you've been proactive, you've saved for retirement through an individual retirement account (IRA) and 401(k) plan. And you know that you'll get additional income from Social Security or through a pension. But what does this all mean for your tax bill when you leave the workforce?

And you know that you'll get additional income from Social Security or through a pension. But what does this all mean for your tax bill when you leave the workforce?

Your tax liability during retirement all comes down to a few important factors, notably your:

As such, your yearly tax bill will affect how much money you really have to pay for your day-to-day expenses.

Having said this, it’s important to understand how your retirement income will be taxed. This information can help you plan for your future if you're still working. And if you've already retired, you may need to account for additional sources so you don't run out of money. Understanding how taxes will affect your retirement income can help you consider ways to minimize your tax bill and maximize your retirement income.

There's a good chance that you won't owe taxes on Social Security if it's the only source of income you receive during retirement. That's because your income will be too low to be taxable. But if you have other sources of income, including otherwise tax-exempt interest income, a portion of your Social Security benefits may incur a tax bill.

More than half of Social Security beneficiaries pay some tax on their benefits. The percentage of families receiving Social Security benefits who have to pay income taxes on them was less than 10% in 1984 and more than 50% by 2015. This figure may rise to 56% between 2015 and 2050, according to the Social Security Administration (SSA).

This figure may rise to 56% between 2015 and 2050, according to the Social Security Administration (SSA).

The amount of your taxable Social Security benefits depends on your combined income or the sum of:

Common sources of gross income include wages, salaries, tips, interest, dividends, IRA/401(k) distributions, pensions, and annuities.Common adjustments to gross income include health savings account (HSA) contributions, deductions for IRA contributions, student loan interest deductions, and contributions to self-employed retirement plans.

The level of your combined income determines the portion of your Social Security benefits that is taxable. The following chart indicates the percentage of your Social Security benefits that will be subject to tax at different levels of combined income:

| Combined Income | Taxable Portion of Social Security |

|---|---|

| Individual Return | |

| $0 to $24,999 | No tax |

| $25,000 to $34,000 | Up to 50% of SS may be taxable |

| More than $34,000 | Up to 85% of SS may be taxable |

| Married, Joint Return | |

| $0 to $31,999 | No tax |

| $32,000 to $44,000 | Up to 50% of SS may be taxable |

| More than $44,000 | Up to 85% of SS may be taxable |

| Married, Separate Return | |

| $0 and up | Up to 85% of SS may be taxable |

This depends on a couple of factors, including the source of income and the total amount you receive. You may get distributions from 401(k)s and IRAs, Social Security benefits, pension payments, and annuity income. Some people may also continue to earn income from work, as an employee, or through self-employment, even though they may have retired from their regular or long-term employment.

You may get distributions from 401(k)s and IRAs, Social Security benefits, pension payments, and annuity income. Some people may also continue to earn income from work, as an employee, or through self-employment, even though they may have retired from their regular or long-term employment.

Unearned income may be subject to income tax and different tax rules. Ultimately, a retiree’s tax liability depends on the tax bracket in which they fall:

Both your income from these retirement plans and your earned income are taxed as ordinary income at rates from 10% to 37%. And if you have an employer-funded pension plan, that income is also taxable.

Distributions from plans funded using after-tax contributions are not taxed the same way as those funded with pretax dollars. Form 1099-R, which is sent to a taxpayer who made after-tax contributions to plans, reports both the gross amount distributed as well as the taxable amount.

Form 1099-R, which is sent to a taxpayer who made after-tax contributions to plans, reports both the gross amount distributed as well as the taxable amount.

IRAs, 401(k)s, and similar plans are required to make annual required minimum distributions (RMDs) to beneficiaries, beginning the year they turn 72 years of age. The RMD requirement was suspended for the 2020 tax year, in response to the pandemic, but was reinstated for 2021.

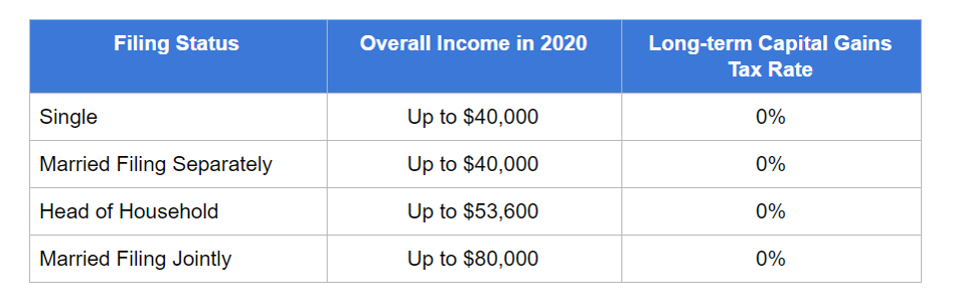

Income such as dividends, rents, and taxable interest from investments held outside IRAs, 401(k)s and similar plans are subject to tax at ordinary income rates of up to 37%. Capital gains rates apply to gains realized on the sale of investments. Long-term capital gains are taxed at low rates, ranging from a zero rate bracket to a rate of 20% for taxpayers with very high taxable incomes.

Roth IRA and Roth 401(k) distributions are not taxable. Roth plans, which are funded with after-tax dollars, do not have an RMD requirement.

While unearned income, such as income from pensions, IRAs, annuities, and other investments, is subject to income tax under rules that vary by the income’s source, earned income works a little differently. Any income you earn from regular employment and self-employment sources is subject to Social Security, Medicare, and income taxes.

Any income you earn from regular employment and self-employment sources is subject to Social Security, Medicare, and income taxes.

If you receive Social Security benefits and continue to work and earn income, you will have to pay Social Security and Medicare taxes on that earned income. However, if your total income (the sum of your earned income, unearned income, and Social Security benefits) remains low enough, you will not owe federal income tax on it. If your AGI is equal to or less than the standard deduction for your filing status, your federal income tax liability likely is zero.

The tax rates and tax liabilities for older people with earned and unearned income depend on the tax bracket that corresponds to their total taxable income. You determine your tax bracket in retirement the same way you did while you were working. Add up your sources of taxable income, subtract your standard or itemized deductions, apply any tax credits you’re eligible for, and check the tax tables in the instructions for Form 1040 and 1040 SR. You can also put all this information into a tax software program or give it to your accountant.

You can also put all this information into a tax software program or give it to your accountant.

The standard deductions for 2021 are used on tax returns filed in 2022. The standard deduction for 2021 is $12,550 for single taxpayers and married taxpayers filing separately, $25,100 for married taxpayers filing jointly, and $18,800 for heads of household. The standard deduction for married couples filing jointly increased for the 2022 tax year to $25,900, tp $12,950, and to $19,400 for heads of households.

Taxpayers who are 65 years of age or older (whether or not they are retired) are eligible for an extra standard deduction of $1,700 for 2021 ($1,750 in 2022) if they are single or heads of household (and not married or a surviving spouse) and an extra $1,350 for 2021 ($1,400 in 2022) per senior spouse if they are married filing jointly, married filing separately, or a qualified widow(er).

| Standard Deductions for Taxpayers Age 65 or Over, Tax Year 2021 | |||

|---|---|---|---|

| Filing Status | Standard Deduction | Senior Bonus | Total Deduction |

| Single | $12,550 | $1,700* | $14,250 |

| Married filing jointly or qualified widow(er) | $25,100 | $1,350 per senior spouse | $26,450 or $27,800 |

| Married filing separately | $12,550 | $1,350 | $13,900 |

| Head of household | $18,800 | $1,700* | $20,500 |

| Standard Deductions for Taxpayers Age 65 or Over, Tax Year 2022 | |||

|---|---|---|---|

| Filing Status | Standard Deduction | Senior Bonus | Total Deduction |

| Single | $12,950 | $1,750* | $14,700 |

| Married filing jointly or qualified widow(er) | $25,900 | $1,400 per senior spouse | $27,300 or $28,700 |

| Married filing separately | $12,400 | $1,400 | $13,800 |

| Head of household | $18,650 | $1,750* | $20,400 |

* If not a surviving spouse, otherwise $1,350 in 2021 and $1,400 in 2022.

If your taxable total income falls below these amounts, you won’t owe any taxes. You usually won’t even have to file a tax return (unless you are married filing separately), though you may want to anyway. Filing a return allows you to claim any credits for which you might be eligible, such as the tax credit for the elderly and disabled or the earned income credit. Filing a return also ensures that you receive any refund you may be owed.

Taxpayers who itemize deductions may not claim the standard deduction and bonus amounts. Recent increases in the standard deduction amounts mean the threshold at which older taxpayers benefit more from itemizing than taking the standard deduction is higher. These higher levels may affect your decisions about when to make charitable donations or pay other deductible expenses. You may be able to benefit from itemizing in some years if you can lump large itemizable expenses together so that they fall within a single tax year.

Below, you'll find the tax rates and brackets based on filing status and income thresholds for both the 2021 and 2022 tax years.

| Tax Brackets, 2021 | ||||

|---|---|---|---|---|

| 2021 Rate | Married Joint Return | Single Individual | Head of Household | Married Separate Return |

| 10% | $19,900 or less | $9,950 or less | $14,200 or less | $9,950 or less |

| 12% | $19,900 to $81,050 | $9,951 to $40,525 | $14,201 to $54,200 | $9,951 to $40,525 |

| 22% | $81,051 to $172,750 | $40,526 to $86,375 | $54,201 to $86,350 | $40,526 to $86,375 |

| 24% | $172,751 to $329,850 | $86,376 to $164,925 | $86,351 to $164,900 | $86,376 to $164,925 |

| 32% | $329,851 to $418,850 | $164,926 to $209,425 | $164,901 to $209,400 | $164,926 to $209,425 |

| 35% | $418,851 to $628,300 | $209,426 to $523,600 | $209,401 to $523,600 | $209,426 to $314,150 |

| 37% | Over $628,300 | Over $523,600 | Over $523,600 | Over $314,150 |

Marginal tax rates for 2022 don't change but the level of taxable income that applies to each rate increases. The top rate of 37% will apply to income over $539,900 for individuals and heads of household and $647,850 for married couples who file jointly.

The top rate of 37% will apply to income over $539,900 for individuals and heads of household and $647,850 for married couples who file jointly.

| Tax Brackets, 2022 | ||||

|---|---|---|---|---|

| 2022 Rate | Married Joint Return | Single Individual | Head of Household | Married Separate Return |

| 10% | $20,550 or less | $10,275 or less | $14,650 or less | $10,275 or less |

| 12% | $20,551 to $83,550 | $10,276 to $41,775 | $14,651 to $55,900 | $10,276 to $41,775 |

| 22% | $83,551 to $178,150 | $41,776 to $89,075 | $55,901 to $89,050 | $41,776 to $89,075 |

| 24% | $178,151 to $340,100 | $89,076 to $170,050 | $89,051 to $170,050 | $89,076 to $170,050 |

| 32% | $340,101 to $431,900 | $170,051 to $215,950 | $170,051 to $215,950 | $170,051 to $219,950 |

| 35% | $431,901 to $647,850 | $215,951 to $539,900 | $215,951 to $539,900 | $215,951 to $323,925 |

| 37% | Over $647,850 | Over $539,900 | Over $539,900 | Over $323,925 |

Will you pay taxes in retirement? Unless your taxable income falls at or below the standard deduction level every year, you probably will. How much you’ll pay is another story. There are many ways to help retirees minimize their tax burden. Strategies include timing distributions, bunching income, bunching deductions that can be itemized, and doing retirement account conversions.

How much you’ll pay is another story. There are many ways to help retirees minimize their tax burden. Strategies include timing distributions, bunching income, bunching deductions that can be itemized, and doing retirement account conversions.

Article Sources

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in our editorial policy.

Internal Revenue Service. “Don’t Forget, Social Security Benefits May be Taxable.”

Social Security Administration. “Retirement Benefits,”

Social Security Administration. “Retirement Benefits, 2022.” Pages 12-13.

Social Security. "Income Taxes And Your Social Security Benefit."

Internal Revenue Service. "IRS Provides Tax Inflation Adjustments for Tax Year 2022."

"IRS Provides Tax Inflation Adjustments for Tax Year 2022."

Internal Revenue Service. "About Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, Etc."

Internal Revenue Service. "Retirement Plan and IRA Required Minimum Distributions FAQs."

Internal Revenue Service. "Topic No. 409 Capital Gains and Losses."

Internal Revenue Service. "Roth Comparison Chart."

Internal Revenue Service. "Publication 554: Tax Guide for Seniors," Page 12.

Internal Revenue Service. "IRS Provides Tax Inflation Adjustments for Tax Year 2021."

Internal Revenue Service. "RP-2021-45," Page 14.

Internal Revenue Service. "Credits and Deductions for Individuals."

Internal Revenue Service. "IRS Provides Tax Inflation Adjustments for Tax Year 2021."

When you retire, you leave behind many things—the daily grind, commuting, maybe your old home—but one thing you keep is a tax bill. In fact, income taxes can be your single largest expense in retirement.

In fact, income taxes can be your single largest expense in retirement.

Many older Americans are surprised to learn they might have to pay tax on part of the Social Security income they receive. Whether you have to pay such taxes will depend on how much overall retirement income you and your spouse receive, and whether you file joint or separate tax returns.

Check the base income amounts in IRS Publication 915, Social Security and Equivalent Railroad Retirement Benefits. Generally, the higher that total income amount, the greater the taxable part of your benefits. This can range from 50 to 85 percent depending on your income. There is no tax break at all if you're married and file separate returns.

The IRS also provides worksheets you can use to figure out what's taxable and how much you might owe in taxes on your retirement income. You can find these worksheets in IRS Publication 554, Tax Guide for Seniors.

You have to pay income tax on your pension and on withdrawals from any tax-deferred investments—such as traditional IRAs, 401(k)s, 403(b)s and similar retirement plans, and tax-deferred annuities—in the year you take the money. The taxes that are due reduce the amount you have left to spend.

The taxes that are due reduce the amount you have left to spend.

You will owe federal income tax at your regular rate as you receive the money from pension annuities and periodic pension payments. But if you take a direct lump-sum payout from your pension instead, you must pay the total tax due when you file your return for the year you receive the money. In either case, your employer will withhold taxes as the payments are made, so at least some of what's due will have been prepaid. If you transfer a lump sum directly to an IRA, taxes will be deferred until you start withdrawing funds.

Smart Tip: Taxes on Pension Income Vary by State

It’s a good idea to check the different state tax rules on pension income. Some states do not tax pension payments while others do—and that can influence people to consider moving when they retire. States can’t tax pension money you earned within their borders if you’ve moved your legal residence to another state. For instance, if you worked in Minnesota, but now live in Florida, which has no state income tax, you don’t owe any Minnesota income tax on the pension you receive from your former employer.

Once you start taking out income from a traditional IRA, you owe tax on the earnings portion of those withdrawals at your regular income tax rate. If you deducted any portion of your contributions, you'll owe tax at the same rate on the full amount of each withdrawal. You can find instructions for calculating what you owe in IRS Publication 590, Individual Retirement Arrangements.

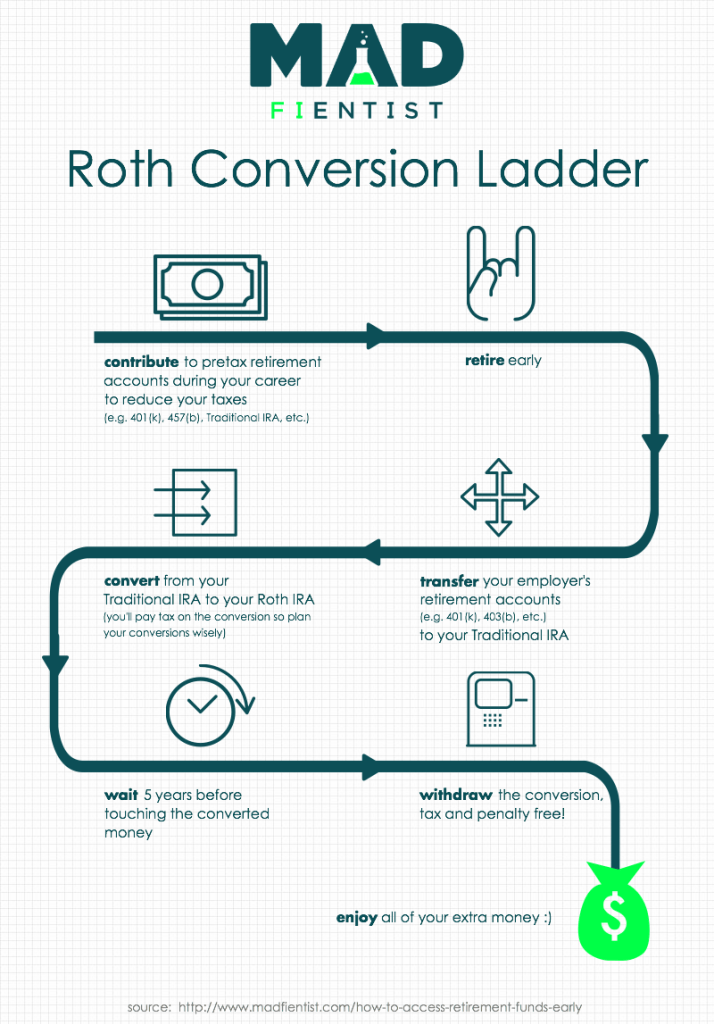

If you have a Roth IRA, you'll pay no tax at all on your earnings as they accumulate or when you withdraw following the rules. But you must have the account for at least five years before you qualify for tax-free provisions on earnings and interest.

When you receive income from your traditional 401(k), 403(b) or 457 salary reduction plans, you'll owe income tax on those amounts. This income, which is produced by the combination of your contributions, any employer contributions and earnings on the contributions, is taxed at your regular ordinary rate. Keep in mind that withdrawals of contributions and earnings from Roth 401(k) accounts are not taxed provided the withdrawal meets IRS requirements.

Interest paid on investments in taxable accounts is taxed at your regular rate. But other income—from both your capital gains and qualifying dividends—is taxed at the long-term capital gains rate of between 20 percent and 0 percent, depending on your tax bracket. This is true when you have owned the investment for more than one year. This lower tax rate on most of your earnings is one of the major advantages of taxable accounts, though it's not the only one. There are no required withdrawals from taxable accounts and no tax penalty for taking income from these accounts before you turn 59½. This means you have greater flexibility in deciding which investments to tap for income and which to preserve for later needs.

There are also ways to minimize the taxes that may be due. You can use capital losses on some investments to offset capital gains on others. Your tax professional can explain how you can bunch or defer income to a single tax year or take advantage of tax deductions and credits. Or he or she may recommend investments that pay little current income but have strong growth potential. These could include index funds, exchange-traded funds, managed accounts and real estate as well as individual securities and mutual funds. Another approach a tax professional may suggest is to make charitable gifts of assets that have increased in value. This technique allows you to avoid capital gains taxes while taking a tax deduction for the current value of the asset.

Or he or she may recommend investments that pay little current income but have strong growth potential. These could include index funds, exchange-traded funds, managed accounts and real estate as well as individual securities and mutual funds. Another approach a tax professional may suggest is to make charitable gifts of assets that have increased in value. This technique allows you to avoid capital gains taxes while taking a tax deduction for the current value of the asset.

You can't avoid income taxes during retirement. But once you stop working, you stop paying taxes for Social Security and Medicare, which can add several thousand dollars to your bottom line.

As you look ahead, you may be thinking about giving some of your assets to family members or friends, which is often beneficial to both you and them as long as you can afford to live comfortably on your remaining retirement income.

Transferring wealth is often a good way to avoid incurring estate taxes—and that's in turn good because these taxes can take a larger bite of your assets than even the highest income tax rate. In addition, some states impose inheritance taxes at various rates on what your heirs receive from your estate.

In addition, some states impose inheritance taxes at various rates on what your heirs receive from your estate.

But the good news is that prior to your death, you can make gifts to whomever you wish—and you can do so up to a certain amount without paying taxes. The IRS ceiling for individuals and married taxpayers changes from time to time.

In addition, you can make larger gifts tax-free to your beneficiaries over the course of your lifetime. You have to follow IRS rules carefully to comply with the lifetime exclusion provisions. For more details, read the instructions for IRS Form 709.

There are pros and cons to making tax-free gifts. On the upside, giving the money away reduces your taxable estate—that is, what will be subject to estate taxes when you die—while also helping your beneficiaries. But on the downside, once the gift is given, if you need access to that money later in your retirement, it's gone.

Since your tax-free income decreases as your income increases, it is important to know how wages, pensions, benefits, and other types of income affect your tax-free income.

Knowing the amount of your income, you have the opportunity to account for tax-free income in the correct amount already during the year and thus avoid the obligation to pay additional income tax by October 1 of the next year.

If you receive monthly wages from several employers in excess of 1200 euros, then you should add up all the amounts received for work.

Since the employer does not know about your other income (for example, wages from other employers) and cannot take them into account when determining tax-free income, you yourself must notify one of the employers of the refusal to apply tax-free income or on the application of tax-free income in the amount of less than 500 euros.

Example

If you earn 1,000 euros per month with two employers, then you have the right to apply the full tax-free income (500 euros) in one workplace, and income tax will be withheld at this workplace only from the remaining 500 euros. At another workplace, tax-free income will not be taken into account and income tax will be deducted from 1000 euros.

At another workplace, tax-free income will not be taken into account and income tax will be deducted from 1000 euros.

Based on your annual income statement, your annual income will be 24,000 euros, the calculated tax-free income will be 666.62 euros per year and you will have to pay additional income tax by October 1 of the following year.

To avoid this situation, you must tell your employer that you are waiving the use of tax-free income or that you allow tax-free income to be taken into account, for example, only in the amount of 55 euros per month.

Therefore, when you have multiple employers, it is important to submit an application for the application of tax-free income, even if you ask the employer to take into account the tax-free income of 0 euros.

Therefore, when you have multiple employers, it is important to submit an application for the application of tax-free income, even if you ask the employer to take into account the tax-free income of 0 euros. If you expect your wages to fluctuate throughout the year, or you are eligible for bonuses, performance bonuses, etc., then it pays to be conservative when determining tax-free income.

Even when the formula-based tax-free income per month can be applied in the amount of 200 euros, it makes sense to submit to the employer an application for applying as tax-free income only, for example, 100 euros per month. In this way, you will avoid having to pay additional income tax on the basis of the annual income tax return by October 1st.

But if you paid more income tax during the year, then after filing your annual return by April 30, the overpaid income tax will be returned to you. Income tax will also be refunded if you ask your employer to deduct tax-free income.

If you are a working pensioner and in addition to your salary you also receive a pension from the Social Insurance Department (including old-age pension, survivor's pension, disability pension, reduced pension and pension supplements) and your monthly income exceeds 1200 euros, then you have to add up the gross amounts of wages and pensions.

A working pensioner who receives both a pension and a salary of less than 500 euros has the right to apply tax-free income in two places, and to submit an application indicating the specific tax-free amount, both to the Social Insurance Board and employer.

It is important to keep in mind that a working pensioner can distribute tax-free income between the employer and the Social Insurance Board in the amount of 500 euros.

Example

A person's pension is 416 euros and salary is 300 euros.

A person has the right to submit an application for the application of tax-free income in the amount of 416 euros to the Social Insurance Board, and an employer to submit an application for the application of tax-free income in the amount of 84 euros.

If, however, you have unexpected income during the year, such as from the sale of real estate or securities, then you can submit a lower amount on your application for tax-free income. In this way, you can avoid the obligation to pay additional income tax by October 1 of the following year.

Disability pension paid by the Social Insurance Board is included in the annual income and affects the amount of tax-free income.

Disability allowance paid by the Unemployment Insurance Fund is not taken into account in determining annual income and does not affect the amount of tax-free income.

Website of the Social Insurance Board "Income tax on benefits and pensions"

If you are a pensioner and there is no other income apart from your pension (including old-age pension, survivor's pension, disability pension, reduced pension and pension supplements), then your total tax-free income is applied to your pension ( 500 Euro).

The amount of non-taxable income depends on the income of working pensioners and persons receiving special preferential pensions, whose monthly income exceeds 1200 euros per month.

It is important that you submit an application to the Social Security Department for exemption. The application can be submitted via the eesti.ee portal or on site at the Social Insurance Board.

Social Insurance Board website "Income tax on benefits and pensions"

If you are on parental leave and receive parental benefit, parental benefit is your taxable income. If the parental benefit is less than 1,200 euros per month, then you are entitled to tax-free income of 500 euros per month. If the parental benefit is more than 1200 euros per month, then tax-free income is applied in accordance with the Income Tax Law.

If you have filed an exemption application with the Social Insurance Department and you have no other income, then the Social Insurance Department will apply the correct formula-based tax-free tax and you will have no additional tax liability.

Website of the Social Insurance Board "Income tax on benefits and pensions"

State benefits paid by the Social Insurance Board (including child allowance, childbirth allowance, childcare allowance, etc.) are not subject to income tax and are not declared in the income tax return.

Tax-free benefits are not taken into account in determining annual income and do not affect tax-free income.

Website of the Social Insurance Board "Income tax on benefits and pensions"

Disability and unemployment benefits are tax-free benefits that are not declared on your income tax return. Disability benefits and unemployment benefits are not taken into account in determining the amount of tax-free income.

There is a difference with the disability pension, which is taxable income, is taken into account in determining annual income and affects the amount of tax-free income.

If you receive unemployment benefits from the Unemployment Insurance Fund, this is your taxable income.

If the insurance benefit does not exceed 1200 euros per month, then you are entitled to tax-free income of 500 euros per month. If the insurance indemnity exceeds EUR 1,200, then tax-free income is applied in accordance with the provisions of the Income Tax Law.

If you have submitted an application to the Unemployment Insurance Fund for the application of tax-free income and you have no other income, then the Unemployment Insurance Fund will apply the correct tax-free tax calculated according to the formula and you will not have additional tax liabilities.

If you receive dividends during the year taxed at the company level at the ordinary tax rate of 20/80, then this is your income, which is taken into account in determining the annual income.

In the income statement, the amount of dividends transferred to you, or the money you receive (table 7. 1) is taken into account as annual income, and this affects the amount of tax-free income.

1) is taken into account as annual income, and this affects the amount of tax-free income.

At the same time, if you receive dividends from abroad, from which income tax is withheld or paid in a foreign country, then the so-called gross amount of dividends is taken into account as annual income, i.e. received dividends together with income tax withheld or paid in a foreign country.

If you receive dividends during the year that are taxed at company level at a lower tax rate of 14/86 and from which income tax of 7% has been withheld, then this is your taxable income, which also affects the amount of non-taxable income.

The amounts transferred to the business account, from which a part of the social tax has been deducted, are taken into account in the annual income and affect the amount of your tax-exempt income.

Entrepreneur account

If during the year you receive income, for example from the sale of property (from the sale of real estate, from the sale of securities, from the sale of timber or from the alienation of the right to cut down a growing forest), then this income is taxable and affects the amount tax-free income.

If you know in advance that in addition to wages and/or pensions you will also have income from the disposal of property, you can notify the employer or the Social Insurance Board, i.e. the person to whom the application for the application of tax-free income was submitted , that you waive the application of tax-free income in whole or in part.

Tax-exempt income from the sale of one's place of residence or income from the sale of movable things that are in personal use are not declared in the annual income statement and are not taken into account in determining annual income for determining tax-free income.

The taxation of the funded pension payment depends on the conditions of payment and can be either tax-free or subject to income tax at a rate of 20% or 10%.

Read more on the web page "Taxation of pensions from January 1, 2021".

Tax-free mandatory funded pension payments are not declared in the income statement of an individual, are not taken into account in his annual income and do not affect the amount of tax-free income.

State pension (I pillar) paid by the Department of Social Affairs and mandatory funded pension (II pillar) paid by the Pension Center or an insurance company, taxed at 20% or 10%, are taxable income, which is also declared in the declaration on the income of an individual, but with the difference that the state pension is included in the annual income and affects the amount of tax-free income, while payments under the mandatory funded pension (II pillar) are not included in the annual income and do not affect the amount of non-taxable income. taxable income.

Examples of calculating total tax-free income

It is still possible to deduct contributions to the supplementary funded pension, or III pillar, up to 15% of a person's taxable income in Estonia, or up to 6,000 euros per year.

The taxation of the payment of the additional funded pension depends on the conditions of payment and can be either tax-free or subject to income tax at a rate of 20% or 10%.

Read more on the webpage " Taxation of pensions from January 1, 2021 ".

Tax-free supplementary funded pension payments are not declared in the income tax return of an individual, are not taken into account as annual income and do not affect the amount of tax-free income.

Supplementary funded pension payment (III pillar) from the Pension Center or an insurance company, taxed at 20% or 10%, is taxable income, which is declared in the income tax return, except that the payment, taxed at 20% is included in annual income and affects the amount of tax-free income, and the taxable payment of 10% is not included in annual income and does not affect the amount of tax-free income.

Examples of calculating total tax-free income

Pension calculator

for Russian Railways employees

CORPORATE PENSION ASSIGNMENT

A corporate pension is granted if the following conditions are met simultaneously:

Reaching the retirement age in accordance with the legislation of the Russian Federation and the Regulations on NGOs for employees of Russian Railways, or the appointment of an early old-age insurance pension or disability insurance pension

the period of payment of pension contributions (insurance period) must be at least 5 years (60 months) *, or 1 month (in case of disability)

dismissal from Russian Railways **

* If the insurance period at the date of dismissal was less than 60 months, then it can be increased by paying additional personal contributions.

** It is possible to assign and pay a corporate pension to a contributor without dismissal from the company in the event of his transfer at his request from a position belonging to the category "managers" to a lower-paid position belonging to the category "specialists", "employees" or "workers". ".

HOW IS THE CORPORATE PENSION CALCULATED?

The amount of the non-state pension is calculated from the total amount accumulated in the individual pension account during the period of participation in the corporate pension system. This amount, in turn, consists of several components. Firstly, these are the personal contributions of the participant and the contributions of the employer. Secondly, it is the investment income that the non-state pension fund annually accrues on the entire amount accumulated in the account.

DETAILS...

Thirdly, these are additional personal contributions that each participant-contributor of the corporate pension system can make. In addition, when assigning a corporate pension, the presence of industry awards is taken into account.

In addition, when assigning a corporate pension, the presence of industry awards is taken into account.

It should also be noted that when calculating the amount of a monthly non-state pension, an annual rate of return of 4% for the entire period of payment, that is, future income, is taken into account.

In addition, by decision of the Board of Directors, non-state pensions may be indexed.

You can make a preliminary calculation of the amount of your future pension by using the Pension Calculator service or by contacting the nearest branch of JSC NPF BLAGOSOSTOYANIE.

HIDE...

PENSION PERIOD

There are several options for paying a pension: for life, urgent (for a specified period) and phased. The amount of the monthly payment will also depend on the chosen period: the smaller it is, the higher the amount of the monthly corporate pension. But it is important to understand that in the case of a fixed-term pension, payments will stop after the due date, but the need for additional income will remain.

DETAILS...

Lifetime pension is the most popular payment option: the contributor will receive a corporate pension in addition to the state pension throughout his life.

In the case of choosing a fixed-term pension, the contributor himself chooses the period during which payments will be made, for example, 10 years.

Another option is the phased payment of pensions, “step by step”. It can be chosen by contributors who draw up an urgent pension with a payment period of at least 14 years for women and 10 years for men. In this case, the pension payment period is divided into two equal stages. During the first stage, the pension is paid in an increased amount - 160% of the calculated monthly amount of the lifelong non-state pension. And at the second stage, the amount of the payment will be determined based on the funds remaining in the pension account.

HIDE...

HOW TO REMAIN THE RIGHT TO A CORPORATE PENSION IF THE INSURANCE SERVICE IS LESS THAN 5 YEARS?

Employees who leave before they have completed 5 years of insurance coverage can make up for the missing period of service by paying additional personal pension contributions.

DETAILS...

At the same time, the size of each contribution must be at least twice the amount of the monthly material assistance that the company pays to non-working pensioners with more than 30 years of experience in railway transport. The number of months during which the contributor pays additional contributions after leaving Russian Railways will be included in the length of service.

HIDE...

INCREASED CORPORATE PENSION FOR WORKERS WITH INDUSTRY AWARDS

When assigning a non-state pension, the presence of industry awards is taken into account.

DETAILS...

10% increase in the amount of corporate pension for contributors awarded with the badge "For 30 years of excellent work in railway transport" "Honorary Railwayman", sign (badge) "Honorary Railwayman".

15% increase in the amount of corporate pensions for contributors who have been awarded the badge “For irreproachable work in railway transport for 40 years”.

The size of the corporate pension is increased by 40% for contributors who have been awarded the second badge “Honorary Railway Worker of JSC Russian Railways” or “Honorary Railway Worker” of the Ministry of Transport of Russia during their work at JSC Russian Railways.

HIDE...

CORPORATE PENSION INDEXATION

The decision to increase payments to pensioners is made by the Board of Directors, based on financial performance based on the results of operations over the past year. At the same time, the increase in payments for the least socially protected groups of pensioners is carried out regularly.

DETAILS...

For example, in 2018, the amount of payment to recipients who were assigned a non-state pension in 2017 due to the establishment of group I disability was increased by 70%, in 2016 it was decided to index by 15% pensions to recipients who, as of January 1, 2014, turned from 70 to 79 years old. In 2015, payments were increased for pensioners over the age of 70, as well as for the disabled, veterans of the Great Patriotic War and other categories of pensioners.