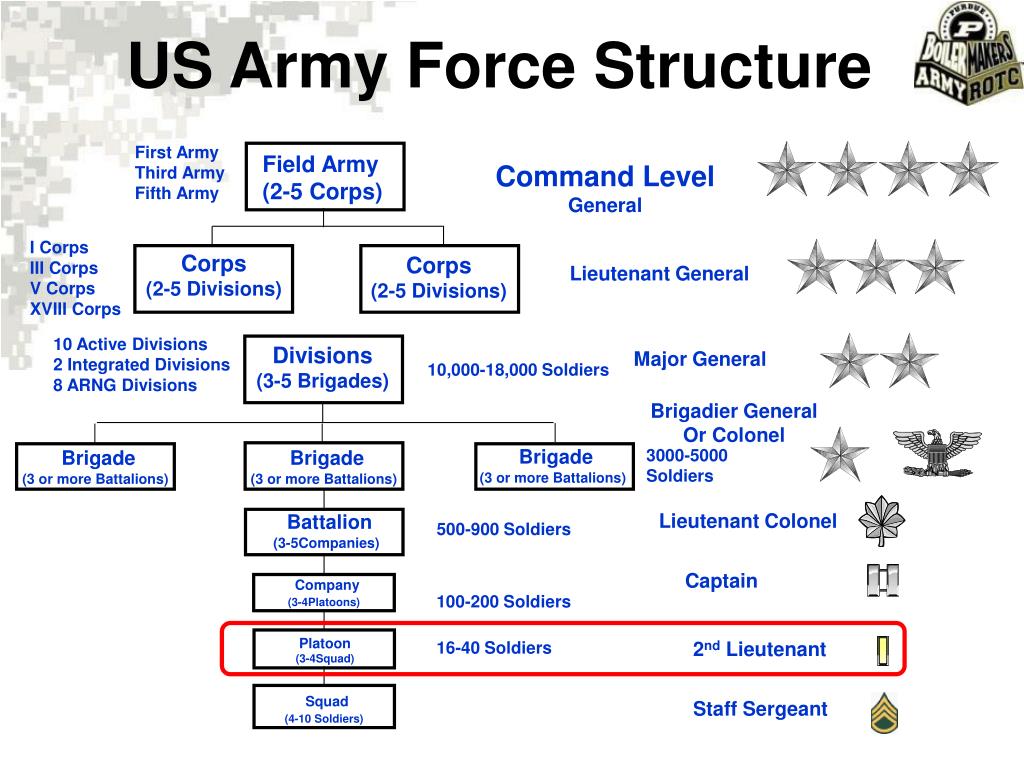

That’s a bold headline, especially if you a retired enlisted military member only bringing in a little over a thousand dollars a month in retirement pay. But it’s true. A military retirement is worth well over a million bucks. In some cases it is worth millions of dollars.

Before we get too deep into this, I want to define what I am talking about. I’m talking about two factors – the long term value in regard to how much you will receive in direct pension over the lifetime of your retirement benefits and the value of the retirement benefits including healthcare coverage, and other benefits. Combined, these benefits are easily worth over a million dollars, even if you don’t have the spending power of a million dollars right now.

Let’s look at an example of retirement pay for an average military career. Since military members are eligible for retirement benefits at 20 years, we will use a reasonable rank and service time for our examples.

It is reasonable to assume that the average enlisted member will be able to retire at 20 years having achieved the rank of E-7, and the average officer should be able to retire at 20 years at the rank of O-5. Of course there will be outliers based on when you served, your career field and other factors, but these ranks and service times should apply to the majority of careers (if anything I am aiming on the conservative side because many people choose to serve longer than the 20 year mark, earning an extra 2.5%-3.5% on their retirement pay per additional service year, depending on whether they take the high 3 retirement plan or the Redux retirement plan).

Track your TSP and other investments with Personal Capital’s free financial dashboard

As we mentioned, we will look at a military retiree with 20 years service at the ranks of E-7 for enlisted and O-5 for officers. The base pay for these ranks in 2009 is:

40

40Most retirees at 20 years will receive 50% of their base pay, which would equal the following amounts:

The next factor to consider is that military retirement pay will be there day in and day out. There are few places in the world that someone can receive a lifetime pension starting at or around age 40. Many military retirees will receive a monthly cash payment for over 40 years. When you add in cost of living adjustments and inflation adjustments, we’re talking about some serious cash!

Using the numbers above from a recently retired E-7 or O-5, we get the following lifetime payments (note: these military retirement pay numbers are not adjusted for inflation and do not include any COLA increases; this is not a planning tool, but for illustration purposes only. Your specific retirement benefits will vary based on your situation):

Your specific retirement benefits will vary based on your situation):

Even without COLA or other inflation adjustments, we can see that we are reaching some serious numbers. Each additional year you serve before you retire can add another 2.5% to your monthly and annual pay, and each higher pay grade you achieve can add hundreds, or even thousands of dollars per year. As previously mentioned, the numbers used in this article are meant to be a conservative estimate.

Visit PersonalCapital.com

OK, there is a minimal TriCare payment, but compared to what civilians pay, it is basically a non-issue. Benefits for retired military members are also guaranteed – they won’t drop you after you have required expensive procedures or for pre-existing conditions. Guaranteed medical coverage is a huge blessing in today’s American society. Here is a little more information about kinds of insurance available to civilians: comparing individual and group health insurance. Hopefully that will hep you better understand the value of military retiree medical benefits!

Benefits for retired military members are also guaranteed – they won’t drop you after you have required expensive procedures or for pre-existing conditions. Guaranteed medical coverage is a huge blessing in today’s American society. Here is a little more information about kinds of insurance available to civilians: comparing individual and group health insurance. Hopefully that will hep you better understand the value of military retiree medical benefits!

Military sponsored medical benefits are incredibly valuable, especially as you get older and when they cover your spouse. There are very few civilian plans that are similar to this. Most people spend several thousand dollars per year for basic medical coverage, and this doesn’t include out of pocket expenses for doctors visits, medical procedures, prescription medication and other associated costs. It would not be unreasonable to place a value of $10,000 per year on military retiree medical benefits, even for a healthy individual. Add a spouse to the benefits, guaranteed coverage, little to no out of pocket expenses for complex medical procedures, and other factors, and the medical benefits alone can be worth hundreds of thousands of dollars or more over the course of a lifetime (and in some instances, into the millions of dollars for people who receive complex medical care over a long term period).

Add a spouse to the benefits, guaranteed coverage, little to no out of pocket expenses for complex medical procedures, and other factors, and the medical benefits alone can be worth hundreds of thousands of dollars or more over the course of a lifetime (and in some instances, into the millions of dollars for people who receive complex medical care over a long term period).

I won’t even try to assign a value to these benefits because they don’t apply to all military retirees equally. Some people may practically live on base, visiting the base clubs, shopping at the exchanges, using the gyms, auto hobby shops, etc. and other people may not live near a base and may not be able to take advantage of any of these benefits. So this category falls in the “good deal if you can get it” benefit, but not a core part of the equation. But it is still worth mentioning because many retirees save a lot of money each year by shopping on base.

One challenge to the analysis is that the military pension includes a cost of living adjustment, so the amount of the income stream has to rise every year by the rate of inflation.

Another problem is that no one knows how long the pensioner will live, so it’s difficult to predict how long the pension will be paid out.

Finally, the calculated lump sum has to be invested in a safe and stable asset to make sure that it survives for decades. Unfortunately, the safe and stable assets have a very low yield, so it takes a larger lump sum to produce an income stream big enough to pay the pension.

The answer to these puzzles involves the mathematical process of “discounting”.

Accountants and actuaries devote entire careers to studying asset yields, human longevity, and other risks. They calculate the statistical probability that a certain lump sum will be able to pay a particular pension for the necessary number of years.

The good news for pension recipients is that the calculations are much more accurate when the analysis is simultaneously applied to hundreds of thousands of pensions as a group. Even better, the Department of Defense can rely on the number-crunching skills of another giant bureaucracy of inflation-adjusted payments: Social Security.

The mathematical details of discounting an inflation-adjusted annuity are well beyond the scope of this post. There’s not an easy formula to convert that $100/day pension to a precise lump sum. However, there are a few simpler estimates that are reasonably close to the more complicated methods.

The easiest estimate assumes that a military pension keeps up with inflation. This eliminates the more complicated factors of correcting future dollars for inflation. If a military pension keeps up with inflation then the pension’s value in today’s dollars stays constant. The lump-sum value of the pension is the total amount to be received during the rest of the veteran’s life:

A 38-year-old veteran receiving $3000/month with a COLA might reasonably look forward to 35 more years of life. The estimate of the present value of their pension would be

The estimate of the present value of their pension would be

The life-expectancy estimate ignores other discounting factors in favor of simplicity and speed. Its main advantage is that a veteran can quickly estimate a lump sum for their own personal expected lifespan. Veterans in good health with long-lived ancestors may decide that they have 40 or even 50 years of retirement, raising the current value of their pension.

Another quick estimate is to assume that the pension is the income stream from a lump sum of Treasury Inflation-Protected Securities (TIPS). TIPS are an extremely safe and stable asset with built-in inflation protection. The market for buying and selling TIPS is huge and liquid so their prices are fairly accurate.

One flaw of this estimate is that, unlike a military pension, when the pensioner dies there’s still a lump sum of TIPS generating a stream of income. Another drawback is that a TIPS’ maturity (now a maximum of 30 years) is usually less than the pensioner’s remaining life expectancy.

Another drawback is that a TIPS’ maturity (now a maximum of 30 years) is usually less than the pensioner’s remaining life expectancy.

The advantage of this estimate is simplicity and speed:

A January 2009 Treasury auction sold 20-year TIPS at an inflation-adjusted annual percentage yield of 2.5%. So for that $3000/month pension,

Another estimate of the lump-sum value of an inflation-adjusted pension is a commercial annuity. The annuity market is generally regarded as liquid because insurance companies compete to offer the “best” price without losing money. However, they still charge more than the actual value of the annuity to make their profit.

Insurance companies could be unable to make annuity payments or even go bankrupt and should be considered a riskier source of annuity payments than TIPS or other government bonds.

One of the “less risky” annuities comes from an agency sponsored by the federal government– the Thrift Savings Plan. TSP annuities are actually purchased from an insurance company and are not guaranteed by the federal government, but the insurance company is presumably charging a smaller fee (to sell a large volume of annuities) and the annuity’s cost would be closer to its value.

TSP annuities are priced each month and do not offer full protection against inflation. The advantage of estimating a pension’s lump-sum value from a TSP annuity is its lower price and the TSP website’s calculator. Assuming that the $3000/month pension is paid to a 38-year-old veteran and limited to 3% annual inflation:

$1.4 million is the price that a veteran would pay in the market to buy a TIPS portfolio or an annuity that would yield their inflation-adjusted pension of $3000/month for the rest of their life. Other research analyzes the theoretical cost of annuities and discounted values– only the cost and not its market price. (This includes a research paper on military pensions– the citation is in the book.)

Other research analyzes the theoretical cost of annuities and discounted values– only the cost and not its market price. (This includes a research paper on military pensions– the citation is in the book.)

These estimates range from about $1 million to $1.2 million. They’re only theoretical estimates. These annuities can’t actually be purchased like the assets of the other estimates, but they’re a more conservative estimate of the probabilities of longevity and other risk factors.

Let’s get back to the veteran who’s just finished 10 years of service and is wondering if it’s worth staying in the military for another decade. After an analysis of the pension’s present value, which sounds more compelling now: $100/day, or lifetime income of over $1 million?

Thousands of dollars coming in on a regular basis quickly add up over the years. Add in increases for inflation, essentially free health care, and other benefits and you can see how the value of a military retirement can quickly be worth millions of dollars over a lifetime.

I didn’t stay in long enough to qualify for military retirement benefits – I separated from the USAF with an Honorable discharge after 6.5 years of service. Part of me looks at the military retirement system with a bit of longing. It is a great system for those who qualify and I would love to be able to receive military retirement benefits for the rest of my life. However, separating from the military was the best move for me at the time and I have no regrets regarding my separation or my military service. I am proud to have served and the military is a large part of who I am today.

*disclaimer about this article: The calculations are for illustrative purposes only and do not reflect the exact retirement benefits you will receive. This is a simplified look at military retirement benefits and does not take many factors into consideration, including taxes, disability benefits, inflation, COLA, and other factors.

It indicates, "Click to perform a search". Insider logoThe word "Insider".

It indicates, "Click to perform a search". Insider logoThe word "Insider". US Markets Loading... H M S In the news

Chevron iconIt indicates an expandable section or menu, or sometimes previous / next navigation options.HOMEPAGEMilitary & Defense

Save Article IconA bookmarkShare iconAn curved arrow pointing right.Download the app

US service members across all branches conduct state funeral services for former President George H. W. Bush. Spc. James Harvey/US Army

Spc. James Harvey/US Army How much are US troops paid?

The answer to that question depends on their rank, time in service, location of duty station, family members, and job specialty — just to name a few.

Other benefits, like government healthcare and tax-free portions of their pay, help service members stretch their earnings a bit farther than civilian counterparts.

To give you an idea, we broke down their monthly salary, or base pay, for each rank. We estimated their pay rate based on how many years they've typically served by the time they reach that rank — many service members spend more time in each rank than we've calculated, while some troops spend less time and promote more quickly.

We also didn't include factors like housing allowance because they vary widely, but these are often a large portion of their compensation. We also didn't include warrant officers, whose years of service can vary widely.

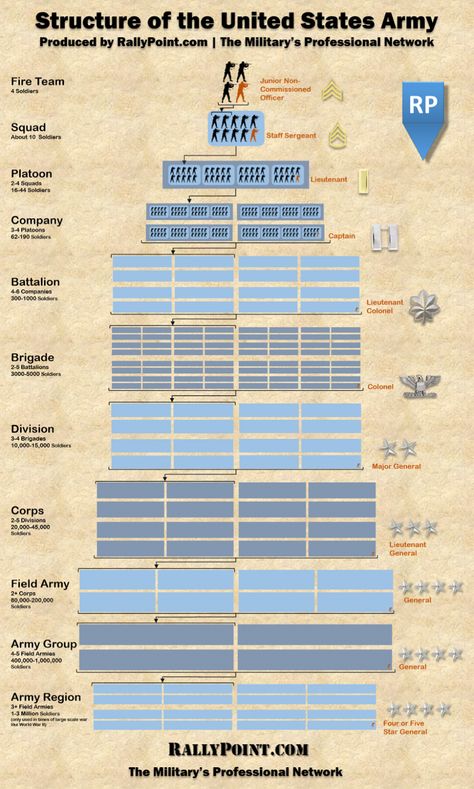

Each military branch sets rules for promotions and implements an "up or out" policy, which dictates how long a service member can stay in the military without promoting.

The full military pay chart can be found here.

Here is the typical annual base pay for each rank.

E-1 is the lowest enlisted rank in the US military: Airman Basic (Air Force), Private (Army/Marine Corps), Seaman Recruit (Navy). Service members usually hold this rank through basic training, and automatically promote to the next rank after six months of service.

Service members usually hold this rank through basic training, and automatically promote to the next rank after six months of service.

Rounded to the nearest dollar, base pay (salary) starts at $1,554 per month at this rank. After four months of service, pay will increase to $1,681 per month.

The military can demote troops to this rank as punishment.

Service members automatically promote to the E-2 paygrade — Airman (Air Force), Private (Army), Private 1st Class (Marine Corps), Seaman Apprentice (Navy) — after 6 months of service.

Their pay increases to $1,884 per month.

Promotion to the E-3 occurs automatically after 12 months of service. Airman 1st Class (Air Force), Private 1st Class (Army), Lance Corporal (Marine Corps), Seaman (Navy).

Basic pay is $1,981 at this rank, adding up to a $427 monthly increase in pay after one year on the job.

Although time in service requirements vary between each branch, service members who promote to E-4 typically have at least two years of service. Senior Airman (Air Force), Specialist/Corporal (Army), Corporal (Marine Corps), Petty Officer 3rd Class (Navy)

If an E-3 doesn't advance in paygrade after two years, their pay will still increase to $2,195 rounded to the nearest dollar.

For those who do make E-4 with two years, pay will increase to $2,307 per month. Some service members will promote to the next rank after just one year at this paygrade — those who remain at the E-4 level will see a pay raise to $2,432 per month after spending three years in service.

Promotions are no longer automatic, but troops can advance to E-5 with as little as three years in service. Those ranks are Staff Sergeant (Air Force), Sergeant (Army/Marine Corps), Petty Officer 2nd Class (Navy).

Those ranks are Staff Sergeant (Air Force), Sergeant (Army/Marine Corps), Petty Officer 2nd Class (Navy).

For these troops, their new paychecks will come out to $2,678 per month.

Service members will commonly spend at least three years at this paygrade. While they do not advance in rank during that time, their pay will still increase along with their time in service.

Four years after enlistment, an E-5 will make $2,804 per month. After six years of service, their pay will increase again — even if they do not promote — to $3,001 per month.

It is unusual for a service member to achieve the rank of E-6 — Technical Sgt. (Air Force), Staff Sgt. (Army/Marine Corps), Petty Officer 1st Class (Navy) — with fewer than six years of service.

An "E-6 with six" takes home $3,254 per month.

After another two years in the service, that will increase to $3,543 in monthly salary, equating to approximately $42,500 per year.

Achieving the next higher paygrade, E-7, before serving for 10 years is not unheard of but not guaranteed. If an E-6 doesn't advance by then, they will still receive a pay raise, taking home $3,656 a month.

Their next pay raise occurs 12 years after their enlistment date, at which point their monthly pay will amount to $3,875.

Achieving the coveted rank of E-7 — Master Sergeant (Air Force), Sgt. 1st Class (Army), Gunnery Sgt. (Marine Corps), Chief Petty Officer (Navy) — with fewer than 10 years of service is not common, but it can be done.

Those who achieve this milestone will be paid $3,945 a month, increased to $4,072 per month after reaching their 10-year enlistment anniversary.

Some service members retire at this paygrade — if they do, their pay will increase every two years until they become eligible to retire. When they reach 20 years, their pay will amount to $4,798 per month — or $57,576 yearly.

The military places a cap on how long each service member can spend in each rank. Commonly referred to as "up or out," this means that if a service member doesn't advance to the next rank, they will not be able to reenlist. While these vary between branches, in the Navy that cap occurs at 24 years for chief petty officers.

A chief with 24 years of service makes $5,069 per month.

Service members may promote to E-8 — Senior Master Sgt. or 1st Sgt. (Air Force), 1st Sgt. or Master Sgt. (Army), Master Sgt. or 1st Sgt. (Marine Corps), Senior Chief Petty Officer (Navy) —with as little as 12 years of service.

or 1st Sgt. (Air Force), 1st Sgt. or Master Sgt. (Army), Master Sgt. or 1st Sgt. (Marine Corps), Senior Chief Petty Officer (Navy) —with as little as 12 years of service.

At that point, they will receive $4,657 per month.

Troops who retire as an E-8 after 20 years of service will take home a monthly salary of $5,374 — or $64,488 per year.

If they stay in past that point, they will receive raises every two years.

An E-8 with 28 years in the service makes $6,076 monthly.

The Army's up-or-out policy prevents more than 29 years of service for each 1st Sgt. or Sgt. Maj.

Airman 1st Class Randy Burlingame/US Air Force

Airman 1st Class Randy Burlingame/US Air Force E-9s have anywhere from 15 to 30 years of experience, although few selected for specific positions may exceed 30 years of service. Their titles are Chief Master Sgt. (Air Force), Sgt. Maj. (Army), Master Gunnery Sgt. or Sgt. Maj. (Marine Corps), Master Chief Petty Officer (Navy).

Service members who achieve this rank with 15 years of experience will be paid $5,580 per month.

They'll receive their next pay raise when they reach 16 years, and take home $5,758 monthly.

After 20 years, they will take home $6,227 — that's $74,724 yearly when they reach retirement eligibility.

Some branches allow E-9s to stay in the military up to 32 years, at which point they will make $7,475 — or $89,700 per year.

Compared to enlisted service members with the same amount of experience, military officers make considerably more money.

A freshly commissioned O-1 — 2nd Lt. (Army/Marine Corps/Air Force), Ensign (Navy) — earns $3,188 per month in base pay alone.

Officers are automatically promoted to O-2 after two years of service. This is a highly anticipated promotion, as it marks one of the largest individual pay raises officers will see during their careers. Those ranks are 1st Lt. (Air Force/Army/Marine Corps), Lt. j.g. (Navy).

An O-2 earns $4,184 per month, which comes out to $50,208 a year.

Officers will receive a pay raise after reaching three years in service.

Using the Army's average promotion schedule, officers will achieve the next rank automatically after four years in the service.

New captains and lieutenants, with four years of service, make $5,671 per month. At this rank, officers will receive pay raises every two years.

By the time they reach the rank of O-4, military officers will have spent an average of 10 years in the service. Maj. (Air Force/Army/Marine Corps), Lt. Cmdr. (Navy)

A major or lieutenant commander with a decade of experience takes home $7,236 per month, or just under $86,832 a year. Officer pay continues to increase with every two years of additional service.

Officer pay continues to increase with every two years of additional service.

O-4 pay is capped at $8,074 a month, so if an officer wants to take home a six-figure salary — additional pay, bonuses and allowances aside — they'll have to promote to O-5.

Officers typically spend at least 17 years in the military before promoting to O-5.

They'll take home $8,751 per month until their 18-year commissioning anniversary, at which point they'll earn $8,998 per month. Those ranks are Lt. Col. (Air Force/Army/Marine Corps), Cmdr. (Navy).

After 18 years in the military, officers receive annual compensation of nearly $108,000 a year.

"Full bird" colonels and Navy captains, with an average 22 years of service, are compensated $10,841 per month.

Officers who do not promote to become a general or admiral must retire after 30 years of service. At this point, they will be making $11,668 a month, or roughly $140,000 per year.

Promotion to brigadier general and rear admiral depends on a wide range of variables, including job availability.

Each of these ranks carries its own mandatory requirement; similar to the enlisted "up or out" policies, officers must promote to the next higher rank or retire.

Officers who have spent less than five years at the lowest flag rank must retire after 30 years of service. Their last pay raise increased their monthly salary to $12,985.

Generals and admirals with two stars — Maj. Gen. (Air Force/Army/Marine Corps), Rear Adm. (Navy) — must retire after their 35th year in the military.

Gen. (Air Force/Army/Marine Corps), Rear Adm. (Navy) — must retire after their 35th year in the military.

At this point, they will be earning $15,381 per month, or $184,572 a year.

Military officer pay is regulated and limited by US Code.

Both three- and four-star admirals and generals who stay in the service long enough will receive the maximum compensation allowed by the code. These ranks are vice admiral for the Navy and lieutenant general for the other branches.

Excluding additional pays, cost of living adjustments, and allowances, these officers make up to $15,800 every month.

That's about $189,600 a year.

Regardless of continued time in service, once a military officer achieves the four-star rank of general or admiral, they will no longer receive pay raises and are capped at $15,800 per month.

Read next

LoadingSomething is loading.Thanks for signing up!

Access your favorite topics in a personalized feed while you're on the go.

Features military & defense military payMore...

Who first appeared in The Mysterious Affair at Styles? The Mysterious Affair at Styles launched Christie's writing career. Christy and her husband subsequently named their home "Styles". Hercule Poirot, who first appeared in this novel, went on to become one of the most famous characters in detective fiction.

Christy and her husband subsequently named their home "Styles". Hercule Poirot, who first appeared in this novel, went on to become one of the most famous characters in detective fiction.

Who first appeared in The Mysterious Affair at Styles? Hercule Poirot, five-foot-four, egg-headed, brilliant Belgian detective who first appeared in The Mysterious Affair at Styles, is the subject of over thirty novels and fifty short stories by Agatha Christie. What makes him such an attractive and enduring character?

When did Mr. Hastings come into fashion? He is first introduced in Christie's 1920 novel The Mysterious Affair at Styles (originally written in 1916) and appears as a character in seven other Poirot novels, including the last Curtain: Poirot's Last Case (1975), as well as in the play and in many short films. stories.

When did 'Stiles' Mystery Case' take place? The novel is set in England in 1916 at Styles Court, an Essex country estate (also the setting for Curtain, Poirot's last case).

In Styles Mystery Case, Emily Inglethorp is murdered by her second husband, Alfred Inglethorp. Alfred was assisted in the murder

Where does he get the money? He leads an enchanted life - fancy sports cars, living in beautiful places, trendy hobbies, and he's a ladies' man. All we know is that he is a retired army captain, but Watson was, too, and has always fought for money. Hastings never existed and lived in a time when everything was more expensive.

Finally he gave up his task, shaking his head gravely. At that moment footsteps were heard outside, and Dr. Wilkins, Mrs. Inglethorpe's personal physician, a burly, fussy little man, ran into the room.

Answer and explanation:

No, Hercule Poirot never meets Miss Marple in the Agatha Christie novels. Despite the fact that they live at the same time, Christie made sure that their ways

Despite the fact that they live at the same time, Christie made sure that their ways

Pauline Moran, who played Miss Lemon, previously spoke about the situation, telling The Guardian back in 2013: “There was chemistry between us all right from the start. After 12 years, the rights were sold to a new production company and they wanted a noir feel not found in the books and guest stars.

Private detective. I went to visit my friend Poirot and found him terribly overtired. During World War I, Poirot left Belgium for England as a refugee, although he returned several times.

Dulcie Hastings (nee Duveen) is a stage performer and Bella's sister who works as part of her stage act called The Dulcibella Sisters. She and Arthur Hastings met on a train in Murder on the Net, but under her stage name Cinderella. Dulcie is his love interest in the novel, and she later becomes his wife.

In Styles Mystery, Mrs. Cavendish was the mother of John and Laurence Cavendish. After her death, her husband married a second time.

Although Christy was only 11 days away (she was discovered at a spa in Yorkshire) and almost 100 years have passed without a credible explanation, the cottage industry of speculation continues to grow.

Role in the novel (contains spoilers)

Before the poisoning, Emily was heard arguing with a man in her office. She later ordered her maid to light the fire. It was because she was arguing with her son John. Emily was poisoned with strychnine and accused of killing her husband.

In The Mysterious Affair at Styles, Evelyn Howard (sometimes referred to as Old Evie) was the companion of Emily Inglethorpe, a robust woman in her forties. She spoke loudly about her negative attitude towards Emily marrying Alfred Inglethorpe, who introduced himself as a distant relative of Evelyn.

Miss Lemon's love for Poirot is perhaps the smartest addition. Brian Eastman explains; "Though I don't think we've ever made it clear, the viewer is quite clear about Miss Lemon's status on the show - her aspirations, her liking for Poirot, and all that a great actress brings to a role" (p. 82).

Although there is no exact mention of Poirot's age, G. R. F. Keating, in his article "Hercule Poirot - Portrait of a Companion", analyzing Poirot's career from the very beginning, calculates that Hercule Poirot, born in 1844, begins to work as a private detective at age 60 and dies at 1974 at the age of 130 (207).

Hercule Poirot's first and most famous companion, Captain Hastings, remains a friend, confidant, chronicler and roommate throughout their lives. His lack of common sense complements Poirot's accuracy perfectly, and their friendship is a highlight for Christie's fans.

In a beautiful fantasy twist, Agatha Christie and her first husband Archie named their home "Styles" after "The Mysterious Affair at Styles." The beautiful postcard village stood in for the fictional Stiles St Mary, and the handsome Chavenage House, near Tetbury in Gloucestershire, stood for Stiles Manor itself.

Although Hercules never marries, he has one love interest throughout the series who appears only briefly in one novel and two short stories: The Big Four, Double Clue and Cerberus Takedown.

Sheppard was Mrs. Ferrars' blackmailer and killed Ackroyd to prevent him from learning the truth from Mrs. Ferrars. Poirot gives the doctor two options: either he turns himself in to the police, or for the sake of his clean reputation and his proud sister, he commits suicide.

Miss Marple actress Geraldine McEwan will quit her role as a noble detective after five years, she announced yesterday. The 75-year-old star said her decision was influenced by a fall before Christmas that broke her hip.

The 75-year-old star said her decision was influenced by a fall before Christmas that broke her hip.

Hercules was not a fan of tea leaves, but preferred to drink herbal tea, his favorite was always chamomile tea, and this allowed him to relax and made his little gray cells work for him. This tea blend is a delicious blend of vanilla rooibos with just the right balance of chamomile and lavender.

"Yes, [Christy] really didn't like him [Poirot] - she didn't like certain aspects of his personality," screenwriter Tom Dalton told RadioTimes.com in an exclusive interview. “You know, there were clearly things about this personality that she created that really turned her on.

Hercule Poirot, the world famous Belgian detective, died in England. Mr. Poirot became famous as a private investigator after being at 1904 retired as a member of the Belgian police.

September 4

Free press uncertainties. Nevertheless, even on the basis of publicly available data, some predictions can be made. Military expert Konstantin Sivkov, Deputy President of the Russian Academy of Missile and Artillery Sciences, captain of the 1st rank, whose competence is confirmed by many forecasts of the development of military conflicts that have taken place in the world in recent years, answers the questions of "SP".

Photo: Free pressFree press

Video of the day

"SP": - Konstantin Valentinovich, if the situation in Ukraine develops in the current direction - the unhurried advance of the allied forces and attempts to counter actions by the armed formations of Ukraine, then how much time will it take and what results can result?

– This process can drag on for quite a long period. Even the complete liberation of Donbass, including the cities of Slavyansk and Kramatorsk, is unlikely to take less than a month and a half.

Even the complete liberation of Donbass, including the cities of Slavyansk and Kramatorsk, is unlikely to take less than a month and a half.

"SP": - But the declared goals of the special operation are not limited to Donbass. What's next?

- With the liberation of Slavyansk and Kramatorsk, hostilities in this direction will most likely stop, and the main ones will be the northern one - Kharkov and the southern one - Nikolaev, Odessa, Krivoy Rog, either alternately or simultaneously. I believe that, first of all, attention will be paid to the southern direction, since a successful operation in this area will allow solving many urgent tasks, the key of which is the deblockade of Transnistria. In this case, pressure on the Armed Forces of Ukraine will continue in the Kharkov region in order to move the line of contact away from the borders of Russia and thereby stop the shelling of our territories and the actions of Ukrainian sabotage groups.

But the Kharkiv direction, I repeat, can become the main one. If the existing tendencies of warfare continue, then it may take a month or a month and a half to isolate the group in Kharkov and defeat it.

If the existing tendencies of warfare continue, then it may take a month or a month and a half to isolate the group in Kharkov and defeat it.

"SP": - How can you destroy a serious enemy grouping - and at the same time avoid such destruction in a city of a million people that we saw in Mariupol?

– The outskirts of Kharkiv are convenient enough for the encirclement of the city, which means that the option of Severodonetsk is possible – if there is a threat of encirclement and defeat, the Ukrainian armed formations will simply leave the city. If in terms of time, then it may take three weeks to encircle the city and force its garrison to retreat, but if you have to take Kharkov by storm, which, of course, is the worst option, it will take a month and a half.

In the southern direction, access to the borders of Transnistria will not be quick, it may take two to three months. Accordingly, the total time for solving the main tasks in both these areas may take about 4 months. However, everything can change under the influence of a number of factors, primarily external ones.

However, everything can change under the influence of a number of factors, primarily external ones.

"SP": - What exactly?

- It is necessary to follow the development of the situation in the United States of America, where it has now reached an acute phase - so acute that it is fraught not only with a political crisis, but also with a transition to a large-scale armed confrontation. Even with the risk of the US breaking up into separate states. In this case, support for the Kyiv regime will either be completely terminated or reduced significantly and will be carried out only by European allies.

"SP": - And how can the crisis that has already begun in Europe affect support for the Kyiv regime?

– It must be understood that Western countries have reached the limit of their ability to supply Ukraine with weapons. Accordingly, the pace of deliveries will decline and may be reduced quite substantially, taking into account the intra-European crisis.

But consider two options. First: after the November elections to the Senate, the United States retains the current alignment of forces, President Joe Biden continues his policy - and then the Armed Forces of Ukraine, with a decrease in the level of military supplies, will simply lose the ability to resist. That is, even this factor can reduce the time of our offensive in key areas. Second, if the election sparks a serious internal conflict in the US, support for Zelensky will end abruptly, plus US influence in Europe will decrease.

First: after the November elections to the Senate, the United States retains the current alignment of forces, President Joe Biden continues his policy - and then the Armed Forces of Ukraine, with a decrease in the level of military supplies, will simply lose the ability to resist. That is, even this factor can reduce the time of our offensive in key areas. Second, if the election sparks a serious internal conflict in the US, support for Zelensky will end abruptly, plus US influence in Europe will decrease.

Accordingly, if this happens, the Zelensky regime will collapse essentially at once. The entire local elite, realizing that it is no longer possible to earn money from the hostilities and the deaths of thousands of citizens, will try to quickly flee the country. And then the disintegration of Ukraine will begin. If the political regime collapses, then the armed forces, deprived of leadership, will also begin to crumble. A conflict between the national battalions and the Armed Forces of Ukraine is also likely. At the same time, a struggle for power left without owners may flare up in Kyiv. Then - the collapse of the front, desertion, mass surrender. Under such conditions, the achievement of the full goals of the special operation will be greatly facilitated, taking the whole of Ukraine under control will take a very short time, measured literally in two to three weeks.

At the same time, a struggle for power left without owners may flare up in Kyiv. Then - the collapse of the front, desertion, mass surrender. Under such conditions, the achievement of the full goals of the special operation will be greatly facilitated, taking the whole of Ukraine under control will take a very short time, measured literally in two to three weeks.

"SP": - And how ready is Russia now for such a scenario? Even in relatively small liberated territories, there are many problems with governance. And then suddenly such a gift - a whole country dependent ...

- Taking into account the country's deprivation of European and American support, local officials will come to power in Ukraine. And even if they have been anti-Russian all this time, they will have nowhere to go. They will be ready to conclude agreements with Russia on any terms, if only to preserve Ukraine as a state and their power in it. Proposals may also appear from regional authorities to become part of Russia by some territories - if only the local authorities would retain their seats.

"SP": - Somehow recently they have been talking seriously about the possibility of a coup d'état in Ukraine ...

- Twice-retired General Krivonos, who recently accused the Zelensky team of the senseless death of hundreds of thousands of military personnel, thereby declared himself as a political figure. Before that, he was a prominent figure, participated in the presidential elections, transferring his electorate to Petro Poroshenko. If we take his words on faith, then “hundreds of thousands” of those killed plus three times as many, according to military statistics, wounded - this is 500-600 thousand people, twice as many as there were in the ranks of the Armed Forces of Ukraine at the time of the start of our special operation. Such losses directly affect about three million people in the country, and since the entire population of Ukraine is now estimated at 20-22 million, we get 10-15% of people who openly hate the Zelensky regime. This is quite enough for a revolutionary explosion and a change of power.

The fact that a criminal case has been opened against Krivonos indicates that he is supported by very serious forces, which the current regime has every reason to fear.

The coming of a new person to power automatically means a cessation of hostilities, since he will not be able to achieve this on any other wave, which the West, which is striving with all its might to maintain military tension against Russia, will certainly not like it.

The only thing is that such a change of power can be accepted by the West, provided that foreign puppeteers decide to keep at least the remnants of Ukraine under their control. And everyone who came to power after 2014 is likely to be simply physically destroyed - the West does not need those who can talk about its ugly deeds.

"SP": - And what is the profit for us from the change of power in Kyiv?

- Russia will not conclude any peace treaties without the condition of denazification. So, the goals of the special operation will be achieved.