If you own an all-terrain vehicle (ATV) or utility terrain vehicle (UTV), then having appropriate ATV insurance is critical. Not only can insurance protect you (and your wallet) in case of accident or injury, but depending on where you live, it might be required by law.

Often, ATV insurance falls under the category of motorcycle insurance. For those looking to take out an ATV insurance policy, it’s important to know what the costs of coverage generally look like — as well as what factors can impact your premiums. In many cases, you may be eligible for various discounts that can lower the costs of your ATV and UTV insurance.

If you’re on the hunt for UTV or ATV insurance coverage, this guide can help. Learn about the average costs of ATV insurance, factors affecting your premiums, common discounts, and more below.

On this page:

Based on our collection of quotes, the average ATV insurance cost is about $100. 47 per month for a standard policy. This price can vary anywhere from $40.75 to $237.77 per month, depending on your desired level of coverage.

To obtain our quotes, we used the following details:

Here’s how each insurance premium quote varied by company:

| Company | Quote (Monthly) |

| Markel | Basic = $40.75 Standard = $53.42 Enhanced = $84.75 |

| Progressive | Basic = $47 Standard = $61.50 Enhanced = $69.33 |

| Nationwide* | Basic = $69. 75 75Standard = $93.17 Enhanced = $134.25 |

| Allstate* | Basic = $103 Standard = $114 Enhanced = $135 |

| GEICO | Basic = $145.37 Standard = $180.24 Enhanced = $237.77 |

| Average | Basic = $81.17 Standard = $100.47 Enhanced = $132.22 |

*Discounts were automatically added at checkout. The other insurers listed did not disclose any automatically added discounts.

Note: Not all issuers offer the same coverage levels. For this reason, we focused on mentioning the level of coverage (basic, standard, enhanced) rather than listing specific amounts.

Generally, the more ATV insurance coverages you select, the more reimbursement you want, and the lower your deductible, the higher your premium will be. The most comprehensive insurance policies with the lowest deductibles tend to be the most expensive.

Below, you’ll see various coverage options through Allstate. The basic insurance policy, which includes the lowest levels of coverage, costs $103 per month. The highest-coverage plan — the enhanced policy — is $135 per month.

| Coverage | Basic Policy | Standard Policy | Enhanced Policy |

| Bodily Injury | $30,000/person $60,000/accident | $100,000/person $300,000/accident | $250,000/person $500,000/accident |

| Property Damage | $25,000/accident | $50,000/accident | $100,000/accident |

| Medical Payments | $1,000/person | $2,500/person | $5,000/person |

| Uninsured or Underinsured | $30,000/person $60,000/accident | $100,000/person $300,000/accident | $250,000/person $500,000/accident |

| Collision and Comprehensive | $500 deductible | $250 deductible | $100 deductible |

| Quote | $103/month | $114/month | $135/month |

When looking for any type of auto insurance, it’s essential to strike a balance between affordability and appropriate coverage. Monthly cost matters, but remember: If you’re in an accident, the amount of coverage will determine how much you’ll spend out of pocket, so this is an important factor as well.

Monthly cost matters, but remember: If you’re in an accident, the amount of coverage will determine how much you’ll spend out of pocket, so this is an important factor as well.

In addition to coverage, several other factors can impact your ATV auto insurance rates.

As you can see above, the type and amount of coverage you choose can significantly impact your insurance premiums. Additionally, some factors influence cost, including things like:

If you’re riding your ATV or UTV to work each morning, or you plan to drive it 10,000 miles this year, you’ll probably pay a bit more.

If you’re riding your ATV or UTV to work each morning, or you plan to drive it 10,000 miles this year, you’ll probably pay a bit more.Unhappy with a quote you’ve gotten? Because there are so many factors that play into ATV insurance premiums, there are quite a few steps you can take to reduce your insurance costs.

To get cheaper ATV insurance, you have three options: 1) select less coverage or smaller limits, 2) qualify for a discount, or 3) lower your risk in one of the categories mentioned above. For tips on the two latter options, see below.

For tips on the two latter options, see below.

Insurance companies often offer discounts for policyholders as ways to lower premiums and encourage good habits. Though specific discounts vary by insurer, here are a few common ones we’ve seen for ATV and UTV policies:

Sometimes, paying your full year’s premium upfront (rather than monthly) can help, too.

You can also lower the risk you present to the insurer in one of the above categories (age, usage, etc.). Some examples include driving safer, taking a driver safety course, occasionally using your ATV, buying a lower-cost vehicle, or not allowing younger drivers on board.

Comparing your options is key when looking to get an ATV insurance policy. Use the table above to get an idea of what coverage costs, and reach out to individual insurance companies for more personalized quotes for your all-terrain or utility vehicle.

Get New York ATV insurance quotes, cost & coverage fast. All-terrain vehicle insurance protects you against the risks of owning and operating your NY ATV or UTV/UTL - either on or off road.

To an New York ATV enthusiast or rider, there's nothing quite like driving in sand dunes in the desert or through the forest. We can't deny that riding an New York ATV is among the most fun things you can do. But, it can be risky, too.

All-terrain vehicles (ATVs) pose a danger to the riders and anyone around them. As such, any NY ATV owner ought to consider getting New York ATV insurance. In fact, it's a legal requirement to have basic All-terrain vehicle insurance in some places. Besides, ATVs can cost a significant amount of money. It's, thus, only sensible to have a reliable form of protection.

Some insurers cover ATVs under motorcycle insurance, and the policies are not very different. Other companies provide New York ATV insurance through their Off-Road Vehicle division. Often, ATVs may be insured along with; motorcycles, golf carts, go-carts, snowmobiles and dune buggies.

Other companies provide New York ATV insurance through their Off-Road Vehicle division. Often, ATVs may be insured along with; motorcycles, golf carts, go-carts, snowmobiles and dune buggies.

ATVs are neither intended nor licensed for use on roads or highways. And, although each state has its own definition of an New York ATV, they're all nearly identical. Most states class any motorized vehicle that has two or more wheels and is designed for off-road driving as an ATV.

Most people associate ATVs with single-passenger, 4-wheeled, off-road vehicles. These are popularly referred to as quads, quad bikes, quadricycles, or four-wheelers. But, there are quite many ATVs which have been designed for two passengers and others with fewer or more than four wheels.

Here's what New York ATV insurance generally covers:

Bodily Injury Liability: NY ATV insurance covers any damage associated with anyone who gets injured or killed in an accident caused by the insured New York ATV. This coverage will also pay any legal fees that result from litigation against the policyholder - however, it'll only cover up to the policy's claim limits. These limits are often specified as a certain amount per person and a particular amount per accident, irrespective of the number of people involved.

This coverage will also pay any legal fees that result from litigation against the policyholder - however, it'll only cover up to the policy's claim limits. These limits are often specified as a certain amount per person and a particular amount per accident, irrespective of the number of people involved.

You ought to ensure that your ATV is driven only by permitted or authorized persons. In case an unauthorized person rides your New York ATV, you may be found liable for the injuries he/she suffers while driving it. It's also imperative that you follow the New York ATV's guidelines. For instance, ensure you're aware of the vehicle's weight restrictions and avoid overloading it.

Property Damage Liability: It's quite similar to the bodily injury liability coverage. The only difference is that property damage liability will meet the cost of damages your ATV causes to someone else's property. That includes personal belongings. This coverage also has a certain claim limit for one incident. It's typically lower than the limit applied in the bodily injury liability coverage.

It's typically lower than the limit applied in the bodily injury liability coverage.

Medical Payments: This ATV insurance coverage is intended to meet any medical expenses that are incurred by those riding in your New York ATV.

Collision: An optional ATV insurance coverage where the insurer promises to pay for the necessary repairs in case your New York ATV overturns or collides with another vehicle. You'll be required to choose a deductible (the amount you pay out-of-pocket before your insurance kicks in). Most insurers tend to cover up to the ATV's cash value.

If you own a low-value ATV, you can consider forgoing this coverage. It'll also keep the premiums low. But, ensure your policy includes the collision coverage if you are leasing your ATV or financed its purchase.

Comprehensive: Another optional NY ATV insurance coverage where the insurer promises to pay for damages which are not a result of a collision from damages from vandalism, theft, fires, flooding, and earthquakes.

For instance, if your ATV is stolen, you'll get compensation (up to the vehicle's cash value) to replace it by filing a comprehensive claim. You'll be required to choose a deductible for this coverage, too.

Uninsured/Underinsured Motorist: This coverage will be quite handy if you or someone else gets injured in an accident where an uninsured or under-insured person was driving your ATV. It'll cover the resulting expenses. It's generally expected that, if someone else causes damage or injury, their insurer will cover the associated costs. But, some individuals may not have any ATV insurance, or enough insurance to cover your bills, even when the law requires it. This coverage has claim limits, too. These limits are usually specified as a certain amount per accident and individual.

Typically New York ATV insurance doesn't cover (excludes):

A standard policy will only cover the ATV's use for either commuting or recreational purposes. It won't cover any damages or losses brought about by organized racing. But, you can get an New York ATV racing insurance policy from select specialty insurers.

It won't cover any damages or losses brought about by organized racing. But, you can get an New York ATV racing insurance policy from select specialty insurers.

Riding ATVs on highways is excluded from coverage because it's illegal. There are several exceptions to that rule, though. Local government agencies may allow ATVs on specific highways. These highways are often within state-owned properties, like large parks or reserves.

ATVs may cross a road but under specific conditions. For example, they must cross the road at a point that's designed for vehicle crossing. Besides that, if an ATV is crossing the road, it ought to come to a stop, and the driver must ensure it's visible to other traffic.

Also intentional damages caused or injuries caused during a criminal act are excluded.

How much does New York ATV insurance cost? Insurance rates for ATVs and UTVs vary based on the state requirements and other factors. Prices can range from a few hundred to over a thousand dollars a year. In areas where there are greater risks and a larger number of claims, rates can go higher.

In areas where there are greater risks and a larger number of claims, rates can go higher.

One factor that keeps costs down is that ATV accidents are often single-vehicle incidents. As such, injuries stem right from the inherent ATVs' dangers, and not other vehicles. And, people probably drive fewer miles and spend less time on ATVs. The result is fewer accidents and insurance claims. Besides, ATVs typically move slower than most other vehicles and have low top speeds.

Request a New York ATV Insurance quote in Albany, Amherst, Auburn, Babylon, Binghamton, Bronx, Brookhaven, Brooklyn, Buffalo, Clarkstown, Clay, Colonie, Elmira, Glen Cove, Greenburgh, Hamburg, Hempstead, Huntington, Islip, Ithaca, Jamaica, Jamestown, Long Beach, Manhattan, Middletown, Mount Vernon, New Rochelle, Newburgh, Niagara Falls, Orangetown, Oyster Bay, Perinton, Poughkeepsie, Queens, Rochester, Rome, Rye, Schenectady, Smithtown, Southampton, Staten Island, Syracuse, Tonawanda, Troy, Union, Utica, Watertown, West Seneca, White Plains, Yonkers and all other cities in NY.

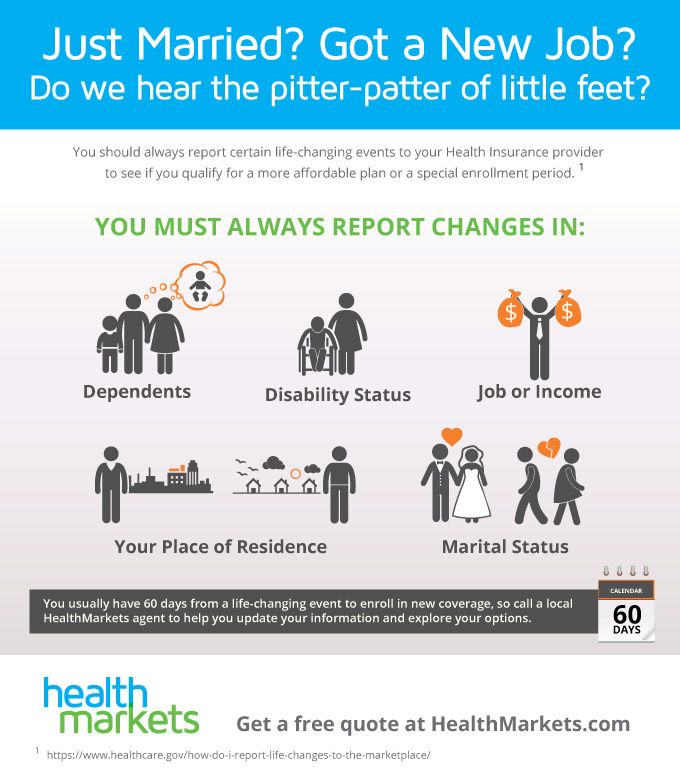

In the state of New York, there are a couple of different types of insurance that are regulated by the state that you should be aware of - as well as the regulations behind them. Understanding what is required for business and personal insurance will help you make sure that you have the right insurance if you ever decide to open a business or even if you are simply looking for information on what kinds of personal insurance you need and what sort of oversight there is for them. Let's take a closer look at personal and business insurance in NY State.

The first type of insurance is general liability insurance. Although general liability insurance is not required by law for New York businesses, it is a good thing to have. General liability protects companies from lawsuits that stem from slips and falls, damage to property while they are on the premises and a variety of other potential incidents that customers may file a lawsuit for. General liability simply keeps you safe in case something happens to someone on your property and they decide to bring a lawsuit against you.

General liability simply keeps you safe in case something happens to someone on your property and they decide to bring a lawsuit against you.

In addition, businesses in New York must carry specific types of insurance such as Worker's Compensation insurance when they have at least one full or part-time employee. This does not apply to independent contractors and subcontractors. The only other regulation in New York is that commercial vehicles that are operating as part of a business must carry commercial auto insurance.

Now, we move onto personal insurance starting with auto insurance. New York State requires that anyone operating a motor vehicle carry liability insurance with $25,000 for bodily injury to one person and $50,000 total for a single accident. In addition, motorists must carry $10,000 for property damage as well.

There are also some regulations governing life insurance. In Article 32 of the New York Consolidated Law it says that residents have a free look period that is limited to 10 days, as well as a grace period of 31 days and then insurance companies must make timely payments within 30 days of receiving notification of the death. If the insurance company does not make these payments on time, then interest can be added to the amount owed. You can find out more about this life insurance information as well as information on the New York state guaranty that ensures that you will receive a payment even if your life insurance company goes out of business.

If the insurance company does not make these payments on time, then interest can be added to the amount owed. You can find out more about this life insurance information as well as information on the New York state guaranty that ensures that you will receive a payment even if your life insurance company goes out of business.

If you are looking for state specific ATV insurance quotes, costs and information: California ATV Insurance, Colorado ATV Insurance, Delaware ATV Insurance, Florida ATV Insurance, Illinois ATV Insurance, Kentucky ATV Insurance, New Jersey ATV Insurance, New York ATV Insurance, Oregon ATV Insurance, Oregon ATV Insurance, Pennsylvania ATV Insurance, Texas ATV Insurance, Washington ATV Insurance.

EK Insurance » New York ATV Insurance

Key factors affecting

the cost of the MTPL policy

Enter the vehicle registration number and find out the cost of the policy

I do not have a number

Insurance indemnity

under OSAGO

We will pay up to 400,000 ₽ to each owner of property damaged in an accident through your fault

We will pay up to 500,000 ₽ to each participant in an accident, the victim of your fault

,000

to the calculator for legal entities

Car

Enter the registration number and click "Find" - the car data will be filled in automatically

Loading data. ..

..

Number format

If the car is not registered, select the number format "I do not have a number" Express Casco

Buy Casco at half price completely online and without car inspection

, including only those risks against which you want to protect your car

More details

Questions and answers

This is an online OSAGO policy. It comes to your e-mail and appears in your personal account. E-OSAGO is equivalent to a paper policy issued in the office.

E-OSAGO

2. Does the price of OSAGO depend on the region in which the car is registered?

Territorial coefficient affects the cost of the policy. It is determined by the registration of the owner of the car.

It is determined by the registration of the owner of the car.

At the same time, the car can be registered in any region of Russia. If the car is registered in a foreign country (does not have a Russian state number), the country of registration does not affect the price of the policy.

3. Do I need to carry a printed e-OSAGO policy with me?

At your discretion. E-OSAGO has the same legal force as a paper policy. It is enough for the traffic police officer to provide the insurance number or show the policy on the phone screen, for example, in the IngoMobile application.

4. What determines the price of the policy?

From the insurance rate and coefficients established by the Central Bank of the Russian Federation 6007-U, as well as the tariff factors established by the company.

OSAGO contract

5. Is an electronic policy cheaper than a paper one?

In accordance with our tariff factors, the price of the policy depends on the method of registration and many other factors.

Application for E-OSAGO

6. Is it possible to get a discount for OSAGO?

No. Tariffs for OSAGO are regulated by the state. The cost of insurance is formed from the base rate set by the Central Bank and the applied coefficients, which depend on the driver's experience, region, vehicle power, etc. You can make an OSAGO policy cheaper due to the bonus-malus coefficient (BM). This indicator is calculated for each driver based on the history of OSAGO insurance payments. The longer the driver does not get into an accident, the lower the value of KBM and the final price of the OSAGO policy will be.

7. How much can the car be insured for? From what risks?

OSAGO can be insured in any subject of the Russian Federation, regardless of the place of registration of the car, while the territorial coefficient that affects the cost when calculating the price of the policy is determined by the registration of the car owner. Please note that in the territory of the Donetsk People's Republic, Luhansk People's Republic, Kherson and Zaporozhye regions as part of the Russian Federation, OSAGO is not valid until January 1, 2024.

8. How to terminate the e-OSAGO agreement?

The contract is terminated according to the standard procedure in one of our offices or in a personal account on our website.

9. What is the difference between an electronic notice of an accident and a paper one?

Nothing. But the electronic notice does not need to be taken to the insurance company. It is convenient to issue it using the mobile application "OSAGO Assistant" or "Gosuslugi AUTO". To use the application, both participants must have a verified account on the State Services. Detailed information on filling out an electronic notice of an accident can be found on the website of the Russian Union of Motor Insurers.

10. What should I do if my car has changed ownership?

The policyholder is obliged to notify the insurer of the change of the owner of the vehicle, as provided for by the OSAGO Rules. At the same time, the OSAGO Law requires the new owner to conclude a new OSAGO agreement. Thus, when the owner of the policy is changed, the norm of the law is executed only if the policyholder has become the new owner. In other cases, when the owner changes, the contract must be terminated, this is required by paragraph 9 of the Decree of the Plenum of the Supreme Court of the Russian Federation of November 8, 2022 No. 31.

Thus, when the owner of the policy is changed, the norm of the law is executed only if the policyholder has become the new owner. In other cases, when the owner changes, the contract must be terminated, this is required by paragraph 9 of the Decree of the Plenum of the Supreme Court of the Russian Federation of November 8, 2022 No. 31.

11. Termination of the CMTPL policy

When terminating the CMTPL policy, in some cases a part of the insurance premium is returned, depending on the number of remaining days of the period of use, minus 23%, the retention of which is provided for by law.

1. What is the Europrotocol?

Europrotocol (European protocol) is a procedure for fixing an accident without calling the police.

Participants of the accident independently fill out a notice of an accident on a special paper form or in electronic form through a special application (OSAGO Assistant)

2. When can an accident be registered according to the European protocol?

The following conditions must be met at the same time:

To count on compensation, you need one of the following options:

Europrotocol” or “OSAGO Assistant”

Europrotocol” or “OSAGO Assistant” from the method of registration of an accident?

Sum insured within which compensation can be received is 400,000 ₽. At the same time, it should be taken into account that the compensation limit depends on how the accident was registered:

Useful information

Documents necessary for the execution of the insurance policy

Forms of applications

Application for OSAGO

Insurance Rules

Conscious On a note

Russian OSAGO is in deep crisis. Will the experience of abroad help us again? How is "autocitizenship" organized in Japan, the USA, Australia and other countries?

27.01.15

445

Share

Developed countries have a functioning institution of compulsory motor insurance. Russia in 2003, forming the national OSAGO rules, followed the European path. Meanwhile, the difficult situation in the compulsory auto insurance market in 2014 once again forced experts to talk about the need to correct the chosen approach. The study of world experience in the introduction of compulsory auto insurance in this regard is very appropriate.

The study of world experience in the introduction of compulsory auto insurance in this regard is very appropriate.

More than once, initiative groups of Russian citizens have put forward specific proposals for reforming the national institution of OSAGO. For example, in November 2014, the following proposals appeared on the Internet portal of the Russian Public Initiative:

It should be noted that the authors of the project have not yet been able to collect 100,000 signatures required for the initiative to be considered by a group of federal experts. Insurers, in turn, to solve all the problems of the domestic "auto-citizen" offer only to increase OSAGO rates. Ideally, they are supposed to be formed on the basis of a market pricing mechanism, as is the case in Europe.

Ideally, they are supposed to be formed on the basis of a market pricing mechanism, as is the case in Europe.

Traffic laws in America are the responsibility of the states. In five of them, there is still no compulsory liability insurance for car owners.

There is no mandatory liability insurance for hardware in Japan. The insurer's liability limit under the local OSAGO policy ($315,000) is intended only to compensate for damage to the life and health of the victims. An interesting fact is that compensation for harm is not paid to relatives. For example, if both cars involved in an accident were driven by brothers, then the insurer will legally refuse to pay out.

The country encourages the merging of police and insurance functions. Thus, the cost of compulsory auto insurance increases if there are several traffic fines over the past year. A technical inspection of the car is required every five thousand kilometers. A mark on the passage of MOT is entered into the insurance policy. There are three types of OSAGO policies: basic and two extended.

Belarus. The Europrotocol bar is set at 400 euros. For a simplified registration of the accident, the presence of the culprit of the accident is sufficient. Thus, in the Republic of Belarus, the problem of minor accidents occurring in parking lots and occurring, as a rule, in the absence of the victim has been solved.