How much will you need to retire? And will it be enough? A survey from Schwab Retirement Plan Services found the average 401(k) participant thinks they'll need $1.7 million to retire. Roughly half of the people surveyed believe they can meet their retirement goals. Of course, many people in the U.S. aren't investing enough to reach that savings goal—and the income it brings. To find out if your retirement income will be enough, you have to start by estimating your retirement expenses.

There are various formulas to estimate retirement expenses, all of which are rough guesses at best. One well-known rule is that you'll need about 80% of the amount you spend going into retirement. That percentage is based on the fact that some major expenses drop after you retire like commuting and retirement-plan contributions. Of course, other expenses may go up (vacation travel, for example—and, inevitably, health care).

Many retirees report that their expenses in the first few years not only equal but sometimes exceed what they spent while working. One reason for this is that retirees simply may have more time to go out and spend money.

Having said that, it's common for retirees' expenses to go through three distinct phases:

Many retirees find they spend the most money in both the early and the final years of retirement.

Of course, future expenses are hard to predict. But the closer you are to retirement, the better idea you probably have for how much money you'll need to sustain your current standard of living—or support a different one.

If you use that as a base, subtract any expenses you expect will go away after you retire, and add in any new ones. That will give you at least a ballpark figure to work with.

If you anticipate any big bills (a lot more travel, a brand new kitchen), be sure to count those in, too. Same for any major cost-savers—for example, if you plan to downsize and move to a less expensive home.

Many financial advisors boil down this answer to one rule of thumb, at least as a starting point: the 4% sustainable withdrawal rate.

Essentially, this is the amount you can theoretically withdraw through thick and thin and still expect your portfolio to last at least 30 years. Not every expert today agrees that a 4% withdrawal rate is optimal, but most would argue you should try not to exceed it.

If you stick to the 4% rule, here's how much you could withdraw annually from three different nest eggs:

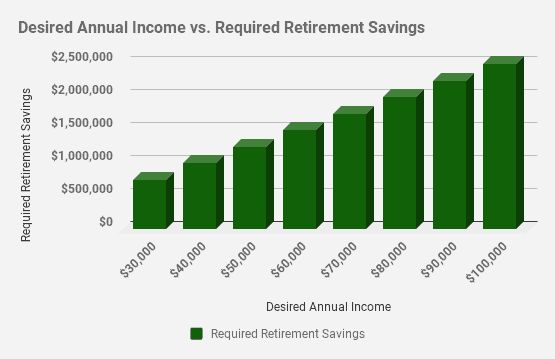

To figure out how much income you'll need in retirement, take your estimated monthly expenses (be sure it's realistic) and divide that number by 4%. So, if you estimate you'll need $50,000 a year to live comfortably, you'll need $1.25 million ($50,000 ÷ 0.04) going into retirement.

Now that you have some notion of your retirement expenses, the next step is to see whether your income will be enough to cover them. To do so, add up how much income you expect to receive from three key sources:

If you've been working and paying into the Social Security system for at least 10 years and have earned 40 credits, you can get a projection of your Social Security retirement benefits by using the Social Security Retirement Estimator. The closer you are to retirement, the more accurate the estimate is likely to be.

The closer you are to retirement, the more accurate the estimate is likely to be.

Bear in mind that the earlier you take benefits, the less you'll get each month. You can opt to take benefits as early as age 62 or as late as age 70, after which there's no further incentive for waiting since you will receive the full amount whether it is age 70 or higher.

In June 2020, the average Social Security retirement benefit was $1,514 a month. The most you can receive depends on your age when you start collecting benefits.

For 2022, the maximum monthly benefit is:

For the 2023 tax year, the maximum monthly benefits are as follows:

If you have a pension coming to you from your current employer or a former one, the plan's benefits administrator can give you an estimate of how much you'll get when the day comes.

If you have a spouse, you'll want to consider your likely income under different scenarios, such as taking benefits in the form of a joint and survivor annuity, which continues to provide a specified percentage of your benefits to your spouse if you die first.

Retirement savings include everything you've stashed in your 401(k)s, IRAs, health savings accounts (HSAs), and other accounts you have earmarked for retirement.

If you have a traditional IRA or 401(k), you have to start taking required minimum distributions (RMDs) at age 72. Note that Roth IRAs have no RMDs during your lifetime (although Roth 401(k)s do). Those RMDs will determine the monthly income you receive from those accounts once you hit age 72. Still, you can start taking money out of an IRA or 401(k) as early as age 59½ without a penalty.

So after you add it all up, if your total retirement income exceeds your predicted expenses, you probably have enough for retirement. Of course, it wouldn't hurt to have more.

Of course, it wouldn't hurt to have more.

But if it looks like you're going to fall short, you may need to make some adjustments and find ways to increase your income, lower your expenses, or both. For example, you could:

The sooner you do the math, the more time you'll have to make the numbers work in your favor.

Saving often proves to result in lower returns and retirement account balances than investing. People generally save money to buy things and for emergencies. The money is there when you need it and it has a low risk of losing value—along with small potential gains.

Investing, on the other hand, is done with long-term goals in mind. When you invest money, you have the potential for better long-term returns, but with more risk. The key is to find the balance between risk and reward, based on your risk tolerance and time horizon.

When you invest money, you have the potential for better long-term returns, but with more risk. The key is to find the balance between risk and reward, based on your risk tolerance and time horizon.

While it's good to have a dollar amount as your long-term savings goal, it's helpful to focus on how much you should sock away each year.

About 10% is the historical recommended savings rate. Schwab further refines that to say that if you start in your 20s, you can retire comfortably with a 10% to 15% savings rate. Here's how a few scenarios could play out for a future retiree.

Let’s assume that Beth, a 30-year-old, makes $40,000 a year and expects 3.8% raises until retirement at age 67. Further, with a diversified portfolio of stock and bond mutual funds, Beth expects a return of 6% annually on her retirement contributions.

With a 5% savings rate throughout her working life, Beth will have saved $423,754 by age 67. If she needs 85% of her pre-retirement income to live on and also receives Social Security, then her 5% retirement savings are significantly short of the mark.

If she needs 85% of her pre-retirement income to live on and also receives Social Security, then her 5% retirement savings are significantly short of the mark.

To match 85% of her pre-retirement income in retirement, Beth needs $1.3 million at age 67. A 5% savings rate doesn't place her savings at even 50% of the funds she'll need. Clearly, a 5% retirement savings rate isn’t enough.

Keeping the above assumptions about her salary and expectations, a 10% savings rate yields Beth $847,528 at age 67. Her projected needs remain the same at $1.3 million. So even at a 10% savings rate, Beth misses the amount of her preferred savings.

If Beth pumps up her savings rate to 15%, she will reach the $1.3 million amount. Adding in anticipated Social Security, her retirement will be funded.

Does this mean that individuals who don’t save 15% of their income will be doomed to a sub-standard retirement? Not necessarily.

As with any future projection scenario, we’ve made some assumptions. Investment returns could be higher than 6% annually. Beth might live in an area with a low cost of living, where housing, taxes, and living expenses are below the U.S. average. She might need less than 85% of her pre-retirement income, or she may choose to work until age 70. Her salary might grow faster than 3.8% annually.

Investment returns could be higher than 6% annually. Beth might live in an area with a low cost of living, where housing, taxes, and living expenses are below the U.S. average. She might need less than 85% of her pre-retirement income, or she may choose to work until age 70. Her salary might grow faster than 3.8% annually.

All of these optimistic possibilities would net a greater retirement fund and lower living expenses in retirement. Consequently, in a best-case scenario, Beth could save less than 15% and have a sufficient nest egg for retirement.

What if the initial assumptions are too optimistic? A more pessimistic scenario includes the possibility that Social Security payments might be lower than they are now. Or Beth may not continue on the same positive financial trajectory. A quarter of the participants in a 2019 Schwab study, for example, had taken out a loan from their 401(k) with most of them taking out more than one.

Alternatively, Beth might live in Chicago, Los Angeles, New York, or another high-cost-of-living region where expenses are much higher than in the rest of the country. With these gloomier hypotheses, even the 15% savings rate might be insufficient for a comfortable retirement.

With these gloomier hypotheses, even the 15% savings rate might be insufficient for a comfortable retirement.

If you've reached mid-career without saving as much as these numbers say you should have put aside, it's important to plan for extra savings or income streams from now on to make up for the shortfall.

Alternatively, you could plan to retire somewhere with a lower cost of living to make your money last longer. You can also plan to work longer, which will augment your Social Security benefits, as well as your earnings. And remember, your Social Security benefit will be higher if you wait until your full retirement age to collect. And it will be even higher if you delay until age 70.

If you're looking for a single number to be your retirement nest egg goal, there are guidelines to help you set one. Some advisors recommend saving 12 times your annual salary. Under this rule, a 66-year-old $100,000 earner would need $1.2 million at retirement. But, as the former examples suggest—and given that the future is unknowable—there's no perfect retirement savings percentage or target number.

But, as the former examples suggest—and given that the future is unknowable—there's no perfect retirement savings percentage or target number.

Clearly, planning for retirement is not something you do shortly before you stop working. Rather, it's a lifelong process. Throughout your working years, your planning will undergo a series of stages. You'll evaluate your progress and targets, and make decisions to ensure you reach them.

A successful retirement depends not only on your own ability to save and invest wisely but also on your ability to plan. How much income you'll need in retirement is hard to know and tricky to plan. But one thing's for certain. It's far better to be overprepared than to wing it.

How much money do you need to comfortably retire? $1 million? $2 million? More?

Financial planners often recommend replacing about 80% of your pre-retirement income to sustain the same lifestyle after you retire. This means that, if you earn $100,000 per year, you'd aim for at least $80,000 of income (in today's dollars) in retirement.

This means that, if you earn $100,000 per year, you'd aim for at least $80,000 of income (in today's dollars) in retirement.

However, there are several factors to consider, and not all of your income will need to come from savings. With that in mind, here's a guide to help calculate how much money you will need to retire.

One important point when it comes to determining your retirement "number" is that it isn't about deciding on a certain amount of savings. For example, the most common retirement goal among Americans is a $1 million nest egg. But this is faulty logic.

Image source: Getty Images

The most important factor in determining how much you need to retire is whether you'll have enough money to create the income you need to support your desired quality of life after you retire.

Will a $1 million savings balance allow you to create enough income forever? Maybe, but maybe not. That's what we're going to determine in this article.

That's what we're going to determine in this article.

The reason you don't need to replace 100% of your pre-retirement income is that, when you retire, you're typically able to eliminate certain expenses. For example:

But retiring on 80% of your annual income isn't perfect for everyone. You might want to adjust your goal based on the type of retirement lifestyle you plan to have and if your expenses will be significantly different.

For example, if you plan to travel frequently in retirement, you may want to aim for 90% to 100% of your pre-retirement income. On the other hand, if you plan to pay off your mortgage before you retire or downsize your living situation, you may be able to live comfortably on less than 80%.

On the other hand, if you plan to pay off your mortgage before you retire or downsize your living situation, you may be able to live comfortably on less than 80%.

Let's say you consider yourself the typical retiree. Between you and your spouse, you currently have an annual income of $120,000. Based on the 80% principle, you can expect to need about $96,000 in annual income after you retire, which is $8,000 per month.

The good news is that, if you're like most people, you'll get some help from sources other than your savings, such as your Social Security benefits. For most people, Social Security is a significant income source.

But the percentage of income that Social Security will replace is typically lower for higher-income retirees. For example, Fidelity estimates that someone earning $50,000 per year can expect Social Security to replace 35% of their income. But someone earning $300,000 per year would have a Social Security income replacement rate of just 11% on average.

But someone earning $300,000 per year would have a Social Security income replacement rate of just 11% on average.

If you aren't sure how much you can expect, check your latest Social Security statement, or create a my Social Security account to get a good estimate based on your work history.

If you have any pensions from current or former jobs, be sure to take those into consideration. The same goes for any other predictable and permanent sources of income. For example, if you bought an annuity that kicks in after you retire, or you’re tapping your home equity through a reverse mortgage.

Continuing our example of a couple that needs $8,000 in monthly income to retire, let's say each spouse is expecting $1,500 per month from Social Security, and that one spouse also has a $1,000 monthly pension.

This means that, of the $8,000 in monthly income needs, $4,000 will come from guaranteed income. The remaining $4,000 will need to come from sources such as investments and savings.

The remaining $4,000 will need to come from sources such as investments and savings.

In summary, you can estimate the monthly retirement income you need to generate using this formula:

Image source: The Motley Fool

Now let's determine how much savings you'll need to retire. After you've figured out how much income you'll need to generate from your savings, the next step is to calculate how large your retirement nest egg needs to be for you to produce this much income in perpetuity.

A retirement calculator is one option, or you can use the "4% rule." The 4% rule says that in your first year of retirement, you can withdraw 4% of your retirement savings.

So, if you have $1 million saved, you would take $40,000 out during your first year of retirement either in a lump sum or as a series of payments. In subsequent years of retirement, you would adjust this amount upward to keep up with cost-of-living increases.

In subsequent years of retirement, you would adjust this amount upward to keep up with cost-of-living increases.

The idea is that, if you follow this rule, you shouldn't have to worry about running out of money in retirement. Specifically, the 4% rule is designed to make sure your money has a high probability of lasting for a minimum of 30 years.

To calculate a retirement savings target based on the 4% rule, you use the following formula:

Image source: The Motley Fool

We saw in the previous section that our couple would need $4,000 per month ($48,000 per year) from their savings. So, in this case, they should aim for $1.2 million in retirement savings accounts, such as a 401(k) plan or individual retirement account (IRA), to provide $48,000 per year in sustainable retirement income.

It's important to note that the 4% rule has a number of flaws. It assumes you'll withdraw the same amount each year in retirement, adjusted for inflation. It also assumes that your portfolio will be split between stocks and bonds throughout your retirement.

It also assumes that your portfolio will be split between stocks and bonds throughout your retirement.

In some circumstances, you may want to withdraw significantly more or less than the standard 4%. For example, as of mid-August 2022, the S&P 500 index is down about 10% for the year to date. During a stock market correction or a bear market, you may want to limit your withdrawals to give your investments time to rebound.

Regardless of your retirement goals, recent stock market volatility shows just how essential it is for retirees to have some cash on hand. This can act as a buffer for your portfolio by helping you avoid cashing out on investments while the market is still down.

Working and collecting Social Security benefits? It gets complicated.

When can you retire and collect Social Security? It depends on when you were born.

n/a

Balancing risk and reward is the hallmark of a great portfolio. Here's how to do it.

There is no perfect method of calculating your retirement savings target. Investment performance will vary over time, and it can be difficult to accurately project your actual income needs.

Furthermore, it's worth mentioning that not all retirement plans are equal when it comes to income. Money you withdraw from a traditional IRA or 401(k) will be considered taxable income. On the other hand, any money you withdraw from a Roth IRA or Roth 401(k) is generally not taxable at all, which may change the calculation a bit.

There are other potential considerations as well. Many workers have to retire earlier than they planned. For example, about 3 million workers retired earlier than they anticipated because of the COVID-19 pandemic.

For example, about 3 million workers retired earlier than they anticipated because of the COVID-19 pandemic.

Even in normal times, older workers often have to retire early due to layoffs, health problems, or caregiving duties. Saving for a longer retirement than anticipated gives you a safety cushion.

It's also important to consider the impact of inflation on your retirement plans. Inflation has gotten a lot of attention in 2022 as prices have increased at the fastest pace we've seen in 40 years.

But even when costs rise at a typical rate, inflation hits senior households harder than working-age households. That's because seniors spend a higher portion of their incomes on expenses such as healthcare and housing. These expenses tend to increase faster than the overall inflation rate.

While we're trying to present the broad strokes here, it's still a good idea to consult a financial advisor who can tailor a retirement savings goal to your particular situation and also help to set you on the right path with a savings and investment plan that can make sure you reach your goals.

By using the methods discussed in this article, you can get a good idea of how much you'll need to save to retire comfortably. Keep in mind this isn't designed to be a perfect method but a starting point to help you assess where you are and any adjustments you might need to make to get where you need to be.

The Motley Fool: What is your advice for someone who may be worried about retiring because of recent financial setbacks?

David John: If your health, family responsibilities, and job status allows, continue to work longer than you might have before. The extra time allows you to save more and for the markets to continue to recover from past losses. Most important, delay taking your Social Security for as long as possible so you'll have a larger, inflation-protected benefit.

The Motley Fool: There are no hard and fast rules about when to retire or how much we should have saved, but what three pieces of advice would you give someone who is just starting their first retirement savings account?

David John:

The Motley Fool has a disclosure policy.

Sign up for our 'Context' newsletter to keep you up to date on what's happening.

Image copyright Thinkstock

Dreaming of warm sunshine and a more fulfilling life in which food takes a backseat, retirees in developed Western countries are increasingly celebrating the end of their days away from their homeland.

Looking for a peaceful place with a warm climate, low cost of living and a favorable tax regime without sacrificing the comfort and quality of care you are accustomed to? Consider that you have found it.

Shady towns in the south of France or the beaches of Central America - in the guide BBC Capital's seven best places for retirees have what you need. Apart from money, of course…

Photo by Getty

If in your old age you want to live where there is enough money for a long time, Panama, the southernmost country in Central America, might suit you. Its capital, which is also called Panama, ranks 124th in terms of cost of living out of 131 cities in the world, according to a study conducted by the analytical department of the respected English-language magazine The Economist. It is cheaper to live there than in the Philippine capital Manila, which is considered one of the least expensive metropolitan cities in Southeast Asia.

According to numbeo.com, a website that tracks prices for everyday goods, a three-course meal for two at an average Panama restaurant will cost PB32. 50 ($32.50), more than half the price of than in New York. And because the local currency is pegged to the US dollar, US retirees don't have to worry about price spikes as a result of exchange rate fluctuations.

50 ($32.50), more than half the price of than in New York. And because the local currency is pegged to the US dollar, US retirees don't have to worry about price spikes as a result of exchange rate fluctuations.

The main condition for obtaining a visa is a stable, guaranteed income. If you receive a pension of at least $1,000 per month (both private and public pension payments are considered), you are unlikely to have any problems obtaining a pensioner tourist visa, which is valid for life. The healthcare system in Panama is considered good, with many doctors being educated in the US and Europe. However, retirees should have at least $200 per month for private health insurance.

But you don't need a lot of money to buy real estate. According to globalpropertyguide.com, a three-bedroom apartment in the popular mountain town of Boquete can be purchased for around $179,000. Foreigners have the same rights to own real estate as local residents.

The main disadvantage is poor road infrastructure outside the capital. But despite this, in 2015 Panama ranked second after Ecuador among the best places for retirees, according to International Living magazine. Low prices, a wide range of leisure activities and proximity to the United States played in her favor - a flight from the city of Miami, located in the southeastern United States in Florida, takes only two and a half hours.

But despite this, in 2015 Panama ranked second after Ecuador among the best places for retirees, according to International Living magazine. Low prices, a wide range of leisure activities and proximity to the United States played in her favor - a flight from the city of Miami, located in the southeastern United States in Florida, takes only two and a half hours.

In addition, the US Department of State's Foreign Security Advisory Board estimates that Panama is relatively safe compared to some Central American countries.

Photo Credit, Thinkstock

Skip the Podcast and continue reading.

Podcast

What was that?

We quickly, simply and clearly explain what happened, why it's important and what's next.

episodes

End of History Podcast

France is one of the most popular tourist destinations for a good reason - beautiful towns and villages, gourmet cuisine, affordable wine and a warm climate in the south are just a few of the reasons why this country is almost first place in the European Union in terms of the number of foreigners permanently residing in its territory.

However, affordability is not France's strong point in the eyes of pensioners. Taxes and social contributions are quite high there, in addition, French residents are taxed on the value of all your property if it exceeds 800 thousand euros, regardless of location.

However, not everything is as bad as it might seem at first glance. France has an excellent public transport system, including a high-speed rail network. Traveling from Paris to Montpellier, 600 kilometers south of the capital, takes just over three hours on the fast TGV train, with discounts for passengers aged 60 and over.

In addition, according to the World Health Organization, France boasts the world's best healthcare system, which is heavily subsidized by the state. Thus, holders of a residence permit in France are likely to have lower medical costs than citizens of other Western countries.

Moreover, life in France is not always more expensive than in other places. There are inexpensive restaurants and real estate prices outside of Paris are relatively low. So, according to French notaries who oversee real estate purchase and sale transactions, a typical residence in the Creuse department in the Limousin region, located on the territory of the Massif Central mountain, will cost only 73 thousand euros, and a medium-sized house in the Alpes-Maritimes in the region Provence - Alpes - Cote d'Azur, where such famous resorts as Cannes are located, can be purchased for 415 thousand euros.

There are inexpensive restaurants and real estate prices outside of Paris are relatively low. So, according to French notaries who oversee real estate purchase and sale transactions, a typical residence in the Creuse department in the Limousin region, located on the territory of the Massif Central mountain, will cost only 73 thousand euros, and a medium-sized house in the Alpes-Maritimes in the region Provence - Alpes - Cote d'Azur, where such famous resorts as Cannes are located, can be purchased for 415 thousand euros.

Image copyright Getty

Want to enjoy the sun all year round? Then you are in Malaysia! This former British colony has everything your heart desires, from skyscraper-studded bustling capital Kuala Lumpur to tropical beaches and deep jungles.

Yes, and living there is quite inexpensive - in the world cost of living index prepared by International Living magazine ranked Malaysia as the third cheapest. According to the magazine, the two of you can comfortably live in a luxurious apartment overlooking the ocean for $1,700 a month. The site xpatulator.com, which analyzes the costs of expats in different countries, states that the prices for medical care and housing in Malaysia are “very low”, in contrast to such expensive options as Hong Kong and Australia.

According to the magazine, the two of you can comfortably live in a luxurious apartment overlooking the ocean for $1,700 a month. The site xpatulator.com, which analyzes the costs of expats in different countries, states that the prices for medical care and housing in Malaysia are “very low”, in contrast to such expensive options as Hong Kong and Australia.

Malaysia is one of the most popular “health tourism” destinations; in 2013, according to the Malaysian Medical Tourism Board, 700,000 people came here to improve their health.

Attract foreigners and tax benefits. As part of the Dual Residence Program, it is relatively easy for retirees to obtain a residence permit in Malaysia, and with it, exemption from taxes on inheritance and on the sale of real estate. In addition, they usually receive a pension or social assistance that is not subject to Malaysian taxes (although US pensioners may have to pay US income tax on it).

In addition, many people in the country speak English, restaurants are cheap, and foreigners have direct property rights; All in all, Malaysia is a great place!

Image credit: Thinkstock

Malta is one of the world's smallest and most densely populated countries, covering just over 300 square kilometers with a population of 400,000. For many residents of this southern European island, English is their native language, and it’s only three hours to fly to London from here, so it’s not surprising that the British have chosen this place - more than five thousand British citizens live on the island.

For many residents of this southern European island, English is their native language, and it’s only three hours to fly to London from here, so it’s not surprising that the British have chosen this place - more than five thousand British citizens live on the island.

Here British pensioners feel at home (British shops are everywhere) and even better (in Malta, unlike the UK, it is very sunny, and the average annual temperature is +18°C). An additional benefit is the “Maltese Pension Plan”, under which the income tax for EU citizens who have received a residence permit in Malta is only 15%, compared to 30-40% in the US and Europe.

In the local dialect, “malta” means “honey”, and pensioners really flock here like bees. This is no coincidence: the country has an excellent health care system (according to the WTO, Malta ranks fifth in this indicator in the world), and all citizens of the country are provided with free medical care. Moreover, within the framework of the agreement on mutual support in the field of health between Malta and the UK, the British can count on the same conditions.

The rich history and beautiful architecture of this picturesque island is also open to everyone.

According to numbeo.com, renting a three-room apartment in Malta's capital Valletta will cost 700 euros, while a three-course meal for two in an average restaurant costs only 50 euros.

Image copyright Thinkstock

Portugal attracts tourists with its many charming fishing villages, medieval towns, beaches and golf courses. Foreigners have settled here for a long time, so many people speak English here.

Lisbon, the capital of Portugal, is one of the oldest cities in the world, famous for its wonderful Mediterranean climate. But pensioners who come to Portugal settle mainly on the Atlantic coast in the Algarve with its azure waters, sunny weather throughout the year and an average air temperature of + 12 ° C in January to + 24 ° C in July.

Whatever part of the country pensioners choose, they are guaranteed preferential tax treatment. Under the system for non-indigenous citizens, income earned abroad may be tax-deductible for up to ten years.

Under the system for non-indigenous citizens, income earned abroad may be tax-deductible for up to ten years.

Outside the most luxurious resort towns in Portugal, such as Quinta do Lago or Vilamoura, the cost of housing is set at a reasonable level. Prices for one-bedroom apartments in the popular resort of Albufeira, according to real estate website rightmove.com, start at 60,000 euros.

In the WHO world ranking, the Portuguese health care system ranks 12th.

Image credit: Thinkstock

Low cost of living, no taxes on overseas retirement income, a tropical climate and a culture of respect for elders - what more could a retiree want from living in a country called the "Land of Smiles" "?

According to International Living magazine, living there is really quite inexpensive. In the magazine's Comparative Cost of Living Index, Thailand came in second for being the cheapest, with a chic one-bedroom apartment with great views available for less than 40,000 baht ($1,200) a month, and a meal of traditional Thai rice noodles for just a dollar.

A one-year retirement visa is issued to those who receive a monthly pension of 65,000 baht ($2,000) or deposit 800,000 baht ($24,000) in a Thai bank.

Local health insurance must be included in the budget. Although the British Foreign and Commonwealth Office ranks many private hospitals as up to Western standards, International Living notes that local hospitals vary in their level of care.

Image credit: Thinkstock

Belize is the only Latin American country with English as its official language, and more and more retirees are coming here, fascinated by the swaying palm trees and white sandy beaches.

The country has a population of only 350,000, but the number of eco-tourists who are attracted by the rainforest, traces of the Mayan civilization and the largest barrier reef in the Western Hemisphere is constantly growing.

An additional benefit has been created for pensioners in the form of a special pension program that provides a number of tax benefits, in particular, exemption from import duties on certain household items, such as a car or a yacht, as well as from taxes on income, including on investments received for outside Belize. The program applies to people over the age of 45 with a monthly income of at least two thousand dollars.

The program applies to people over the age of 45 with a monthly income of at least two thousand dollars.

Real estate prices are lower than in the US, but not as much as in other Central American countries. Hollywood actor Leonardo DiCaprio is said to have recently bought himself an island to the west of the largest island in the Belizean archipelago, Ambergris Key, for $1.75 million. But still, buying property in Belize is relatively easy - the contract is in English, and local laws are based on the British system, which helps protect the interests of buyers.

There are inexpensive private clinics in Belize that offer quality medical care, but for complex procedures, many foreigners prefer to travel to the United States - insurance often covers the cost of the flight.

Read the original of this article in English is available on the website BBC Capital .

https://inosmi. ru/20221121/bayden-258062155.html

ru/20221121/bayden-258062155.html

The British diagnosed 80-year-old Biden as dead above his shoulders

The British diagnosed 80-year-old Biden as dead above his shoulders

The British diagnosed 80-year-old Biden as dead above his shoulders

Daily Mail readers were not happy anniversary of Joe Biden. Commercial airline pilots are required to retire at 65 so as not to endanger anyone, and | 11/21/2022, InoSMI

2022-11-21T15:31

2022-11-21T15:31

2022-11-21T16:55

daily mail

politics

joe biden

usa

anniversary

reader comments

/html/head/meta[@name='og:title']/@content

[@name='og:description']/@content https://cdnn1.inosmi.ru/img/07e6/0b/15/258065930_0:0:3073:1728_1920x0_80_0_0_62b298280fafa55dc29029b32a8c3c16.jpg 901 Wills Robinson (901 Wills Robinson) On Sunday, November 20, Joe Biden celebrated his 80th birthday with his family at the White House, becoming the first President of the United States to reach such an advanced age. But now, while Biden blows out the candles on his birthday, 50 years after Ever since he first entered the Senate, questions have been raised about his age and suitability for office, and calls have grown louder to step down to make way for younger leaders. Biden has already indicated he "intends" to run for a second term. However, on November 10, he acknowledged that "ultimately" it will be a "family decision." If Biden wins the next election, he will be 82 years old at the time of his inauguration and 86 years old at the end of his presidential term. Critics are already expressing concern about his age, memory problems and ability to be the country's commander in chief. Despite Biden's claims that he is ready to continue to carry out all the duties of the president, in a recent interview with MSNBC he did acknowledge that voters have " absolutely legal" right to ask questions about his age. With two more years left on his current term, the Republicans will be constantly talking about this topic.

But now, while Biden blows out the candles on his birthday, 50 years after Ever since he first entered the Senate, questions have been raised about his age and suitability for office, and calls have grown louder to step down to make way for younger leaders. Biden has already indicated he "intends" to run for a second term. However, on November 10, he acknowledged that "ultimately" it will be a "family decision." If Biden wins the next election, he will be 82 years old at the time of his inauguration and 86 years old at the end of his presidential term. Critics are already expressing concern about his age, memory problems and ability to be the country's commander in chief. Despite Biden's claims that he is ready to continue to carry out all the duties of the president, in a recent interview with MSNBC he did acknowledge that voters have " absolutely legal" right to ask questions about his age. With two more years left on his current term, the Republicans will be constantly talking about this topic. <...>Readers' comments:SwiftwithwindThese goofs are planning to run him for president again. Obviously, America has run out of ideas - and worthy candidates. Helle Nback I hope he will be the last head of the White House of such an advanced age. We need younger leaders. And now we see old minds and old ideas. Enough! Paula. Just tell him that his presidential term is over. He won't even understand. He is dead above the shoulders.d32mullisThe awakened left constantly complains that the country is run by old white men. And then they make Biden their candidate. This is completely illogical. This makes me think that some other force is really running the show. suddenly dies and Kamala Harris takes his place, communist China will invade Taiwan the very next day.gravedigger 159Commercial airline pilots are required to retire at age 65 because it is believed that if they continue to fly, they will endanger the lives of many people. Now consider that Joe's finger is on the nuclear button.

<...>Readers' comments:SwiftwithwindThese goofs are planning to run him for president again. Obviously, America has run out of ideas - and worthy candidates. Helle Nback I hope he will be the last head of the White House of such an advanced age. We need younger leaders. And now we see old minds and old ideas. Enough! Paula. Just tell him that his presidential term is over. He won't even understand. He is dead above the shoulders.d32mullisThe awakened left constantly complains that the country is run by old white men. And then they make Biden their candidate. This is completely illogical. This makes me think that some other force is really running the show. suddenly dies and Kamala Harris takes his place, communist China will invade Taiwan the very next day.gravedigger 159Commercial airline pilots are required to retire at age 65 because it is believed that if they continue to fly, they will endanger the lives of many people. Now consider that Joe's finger is on the nuclear button. Sleep well, America! Zippy1-Watch any Biden video from ten years ago, and then watch some of the latest videos. You'll quickly see why he won't run for president again. Gravy Edgar I'm a liberal, but even I think that's ridiculous. Why do we admit that people who often confuse the gas pedal with the brake pedal run our country? We need younger leaders who can represent the interests of the majority of our people. Why don't people in their 40s or 50s run for president? Ruthe007He also became the first US president to suffer from dementia. The first president to commit treason, and while the evidence of treason is enough to sink any ordinary citizen, the Justice Department and the FBI choose to ignore it. GeoKing He became the worst president in the history of the United States. From Afghanistan straight into recession. Worst two years in our country's history. Linnae Biden won't last long given all the evidence in Hunter's laptop - evidence of crimes involving the entire Biden family. He will have to leave the presidency with a scandal.

Sleep well, America! Zippy1-Watch any Biden video from ten years ago, and then watch some of the latest videos. You'll quickly see why he won't run for president again. Gravy Edgar I'm a liberal, but even I think that's ridiculous. Why do we admit that people who often confuse the gas pedal with the brake pedal run our country? We need younger leaders who can represent the interests of the majority of our people. Why don't people in their 40s or 50s run for president? Ruthe007He also became the first US president to suffer from dementia. The first president to commit treason, and while the evidence of treason is enough to sink any ordinary citizen, the Justice Department and the FBI choose to ignore it. GeoKing He became the worst president in the history of the United States. From Afghanistan straight into recession. Worst two years in our country's history. Linnae Biden won't last long given all the evidence in Hunter's laptop - evidence of crimes involving the entire Biden family. He will have to leave the presidency with a scandal.