By Elizabeth Blackstock Apr 18, 2022

Aaron Miller/Capital One

Article QuickTakes:

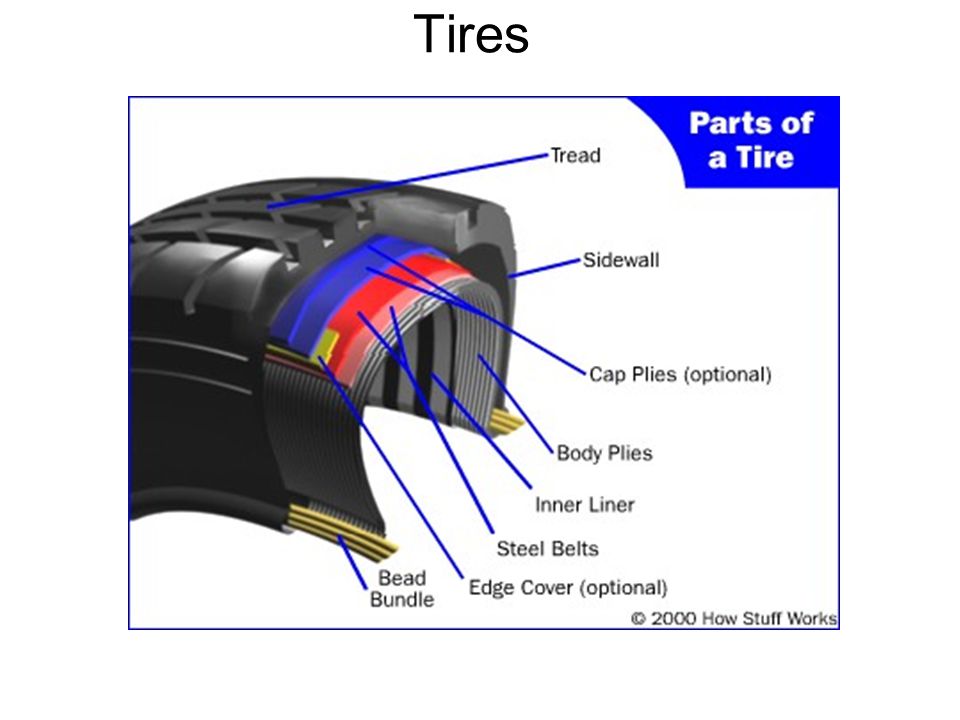

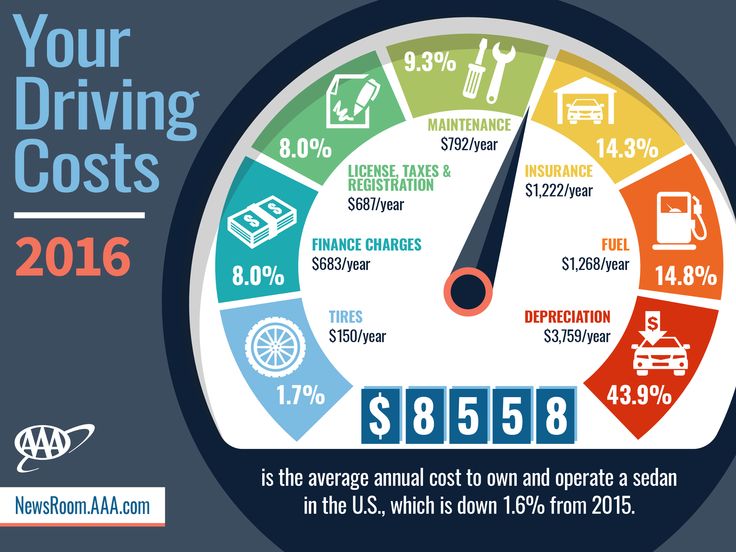

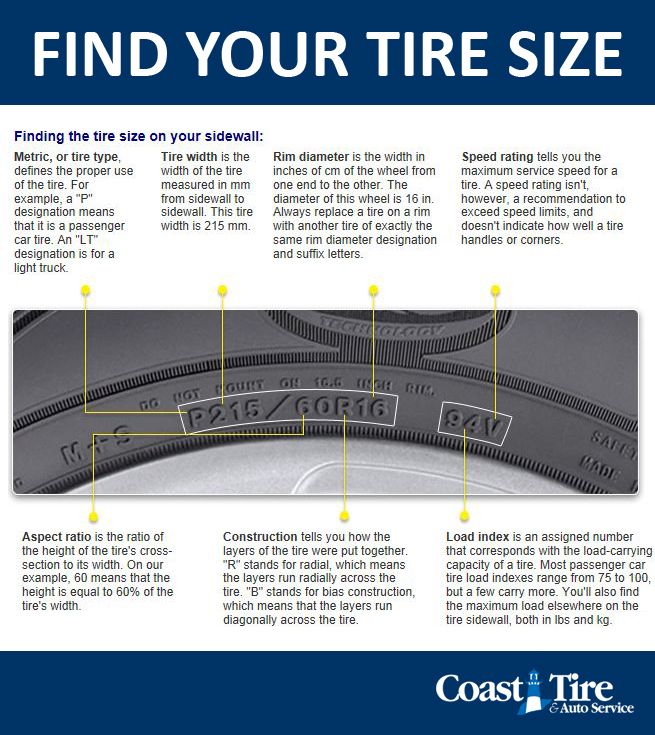

Your car’s tires and wheels take a lot of abuse. Nails, glass, potholes, curbs, and other hazards can cause enough damage to these elements to put your car out of commission — at least temporarily. Repairs can cost a pretty penny, so you may want to insure your car’s rolling gear — especially as traditional auto insurance or roadside-assistance policies tend not to cover wheels and tires. (The deductible on a comprehensive auto policy is often more than the cost to replace a tire.) Depending on the terms, tire and wheel insurance can cover the cost of repairs and replacement, as well as roadside assistance, trip interruption, and alternate transportation while your car is out of service.

Cost will vary depending on your location, vehicle, and the extent of coverage you're seeking. However, most insurance companies will charge between $60 and $90 per year for all-tire coverage, or from $10 to $30 per tire when buying replacements.

Most plans cover your tires for a predetermined amount of time, mileage, or dollar amount. For example, your policy may allow up to $5,000 worth of repairs, 60,000 miles of travel on a tire, or three years of use. It's important that you understand what is and is not covered, and if you have to pay a deductible. Many policies exclude wheel replacement, vehicle realignments, and claims for curb damage.

If you order a vehicle from the factory or purchase a vehicle off a lot, the involved dealership will likely offer you tire and wheel insurance during the finance discussion. You can also buy this kind of protection through roadside-assistance companies like AAA, your automotive insurance company, or at your local tire shop when you fit your vehicle with new tires.

It depends on your personal circumstances and the ways you intend to use your vehicle. If you have a long daily commute over heavily pockmarked roads, then the cost of insurance could save you money in the long run. But if you live in an area with nicely paved roads (and without constant freeze-thaw cycles testing the limits of concrete), your risk of flattening a tire or bending a wheel is markedly lower, and insurance may not pay off for you.

TAGStire and wheel insurancecar insuranceauto policyroadside assistance

This site is for educational purposes only. The third parties listed are not affiliated with Capital One and are solely responsible for their opinions, products and services. Capital One does not provide, endorse or guarantee any third-party product, service, information or recommendation listed above. The information presented in this article is believed to be accurate at the time of publication, but is subject to change. The images shown are for illustration purposes only and may not be an exact representation of the product. The material provided on this site is not intended to provide legal, investment, or financial advice or to indicate the availability or suitability of any Capital One product or service to your unique circumstances. For specific advice about your unique circumstances, you may wish to consult a qualified professional.

The images shown are for illustration purposes only and may not be an exact representation of the product. The material provided on this site is not intended to provide legal, investment, or financial advice or to indicate the availability or suitability of any Capital One product or service to your unique circumstances. For specific advice about your unique circumstances, you may wish to consult a qualified professional.

Elizabeth Blackstock

I’m Elizabeth Blackstock, and after growing up around the Detroit automotive industry, I’ve made it my life’s mission to make information about vehicles accessible for the average consumer. Whether you’re a hardcore auto enthusiast or someone looking for a practical machine for the daily commute, I’m here to help you make your most informed decision.

| Insurance-it's everywhere. One can insure just about anything. Are tires an investment one needs to insure? Tire insurance, also called a road hazard policy, road hazard warranty, or tire reimbursement plan, is a rapidly growing industry in the automotive world. Tire warranty plans pay in full or in part for the replacement or repair of damaged tires and/or rims from "road hazards." Road hazards are defined as pot holes, debris, nails, wood, and other hazards found in the road. Curbs, sidewalks, and stone walls are not road hazards. This is an important distinction to consider when deciding if tire insurance is right for you (discussed further ahead). Tire plans last for a specific period of time and tire wear tread-depth. Some plans last 2-3 years. Others can last 5 years or 60,000 miles. Several plans come with fixed amounts of coverage: $500 per year up to 4 years. Many contracts require three years of law school to comprehend. In terms of tread depth, a tire is usually considered worn out (and thus the plan null and void) at 2/32 to 3/32 of an inch. Another important distinction is in the type of plan. Tire reimbursement plans are just what they say. You, the plan holder, will be reimbursed after the claims process is finalized-usually 2-8 weeks. Road hazard policies operate similarly to reimbursement plans. However, some tire insurance providers, in partnership with the repair facility, may have a direct-pay relationship. Thus, there would be no out-of-pocket expense, except for applicable deductibles, and items not covered in part or in full. These plans are primarily sold by tire dealers and repairshops. The prices range from $10 to $30 per tire. They also can be based on a percentage of the cost of the tire: usually 12% to 15%. Both types of plans have a number of variables, requiring a magnifying glass to read the fine print. Also, many are pro-rated warranties, covering only a percentage of the cost of the tire based on its wear. Claims and Coverage: Some plans offer national coverage either among their service facilities or from other repair centers. Claims procedures will vary. Others only provide local coverage, or coverage at the selling facility. Limitations: For example, many plans allow for a maximum of $30 to mount and balance one tire, and a maximum of $15 to repair a tire. However, sport tires often have significantly higher mounting and balancing fees-upwards of $50 per tire-and tire repair prices can exceed $90. Although there usually is not an issue with the latter given the competitive market, the service center's price mark up may be unacceptable to the plan provider. In this case, the service center needs to lower the price or you, the service customer, need to pay the difference-or go somewhere else. This does happen! Rim Prices and Repairs: Rims are replaced only if the damage is so extensive that the new tire, when mounted on the rim, won't hold air. Repairing rims is a bad option. While some rim repair is acceptable, badly warped or damaged rims will in no way ever be the same. Alignments: Road Hazard Protection Positives: Myths: 1) "Can I pop all 4 tires and get a new set of tires?" You can try. But this type of claim will trigger a number of red flags with the insurer. The policy holder will likely send out adjusters and/or require photographs. You will also have a difficult time explaining how a "road hazard" caused all 4 tire pop. 2) "New tires come with a road hazard warranty. New tires do come with a warranty by the tire manufacturer. However, it only covers defects in workmanship. New tire warranties do not cover punctures or damages from external sources. This is why "road hazard" protection is being pushed. New tires are rarely defective. If there is a problem, it's usually noticed when balancing the tire. Or, there is a drivability concern such as vibration or noise. If there's a defect it's generally caught right away, and the tire swapped out. 3) "It's so cheap; it's a no-brainer, right?" Actually, the experts don't agree with this statement. The Economics of Tire Warranties: "The decision to buy an extended warranty...defies the recommendations of economists, consumer advocates and product quality experts, who all warn that the plans rarely benefit consumers and are nearly always a waste of money. '[Extended warranties or purchase protection plans] make no rational sense,' Harvard economist David Cutler said. 'The implied probability [of having an issue with the product] has to be substantially greater than the risk that you can't afford to fix it or replace it. If you're buying a $400 item, for the overwhelming number of consumers that level of spending is not a risk you need to insure under any circumstances.'" In short, road hazard warranties are a waste of money. Don't insure that which you can afford to replace. Numbers Game and Slim Chances: Curbs: You Won't Notice: Despite the potential dangers of damaged tires, the damage very often does not translate into any noticeable drivability issue. The point is that if you don't notice any tire damage you can't benefit from the coverage. Research Shows: Auto Insurance: Free Road Hazard Warranties: Also, some car manufacturers provide road hazard warranties FREE of charge for 12 months or 12,000 miles. If you're buying a new car or even used, ask that the dealer provide a complimentary road hazard policy (after all the wheeling and dealing is done, of course), and just before you commit. "What's the best road hazard policy?" |

| Auto Insurance |

Each company forms such a list based on its own practice, therefore it is impossible to list all the existing reasons for refusing to pay. However, there are a number of cases where the insurance company is guaranteed not to compensate for the damage.

First of all, it is worth mentioning the standard exceptions. They are regulated not only by the terms of insurance of a particular company, but also by insurance legislation. No auto insurer will compensate for damages due to the following events.

In addition, you should not count on payment when the car was requisitioned or confiscated by decision of one of the state bodies. If the representative of the state had sufficient powers, and his actions do not contradict the law, the insurer will refuse to compensate for the damage due to such actions.

In addition, no insurance company will compensate for moral damage.

This also includes cases of lost profits and commercial losses of the car owner, for example, due to the downtime of a damaged car.

Along with the described events, it is worth mentioning cases of damage to technically faulty vehicles. If the client has violated the rules for operating the car or has not passed the mandatory technical inspection, he will be denied compensation for damage.

The same result will be in the case of transfer of the car to hire or rent without the knowledge of the insurance company. In addition, the car owner will not be compensated for damages when using transport in competitions or tests, if such a possibility is not provided for by the terms of the contract.

The unconditional basis for denial of damages is the intentional damage to the car by the client or his representative. In other words, the car owner will definitely be denied payment if he deliberately provoked an accident. This requires strong evidence, in particular the conclusion of the trace examination and witness testimony.

This requires strong evidence, in particular the conclusion of the trace examination and witness testimony.

If the car is damaged due to the fault of third parties, you should not give up claims against such citizens, otherwise the insurer loses the right to subrogation. If the insurance company is deprived of the opportunity to make a claim to the culprit of the accident, its client will have to pay for the repairs themselves.

In addition, damages will be denied if the car is damaged under the following circumstances:

Some insurance companies include cases of gross traffic violations, for example, driving at a railway crossing at a prohibitory traffic signal, as exceptions.

The payment will also be denied if at the time of the accident the driver was under the influence of alcohol, drugs or drugs, the use of which is prohibited from driving.

Leaving the scene of a traffic accident is another ground for refusal. If the driver allowed a collision with another vehicle or with an obstacle, and then fled the scene, he will not be paid compensation under the CASCO agreement.

The car owner is not compensated for damage due to damage to the car when loading onto other vehicles and unloading. In addition, accidents during the evacuation or towing of a car do not fall under the insurance coverage under the CASCO agreement.

Special attention should be paid to cases of damage to vehicles during the loading, unloading or transportation of any things. Such damage is not recoverable. In other words, the car owner will not be paid anything if the car is damaged due to the spontaneous movement of bulky cargo inside the cabin or trunk.

Many companies include theft of certain parts of the car as an exception to their coverage. In particular, the insurer will refuse to recognize the theft of parts as an insured event if they were stored separately from the vehicle.

In addition, theft of the following items is not an insured event:

In addition, the insurance company will not pay compensation for a stolen awning. Damage to this element of the machine due to the actions of intruders, again, is not an insured event. Accordingly, if a long-term parking of the car is expected, it is worth taking care of the safety of the awning.

It is noteworthy that insurance companies do not indemnify for theft or theft of the anti-theft system. However, in some cases, payment is still possible, but only if the car owner has insured such a system as additional equipment.

Exceptions include all incidents resulting from errors in the repair or maintenance of the vehicle. Therefore, you need to carefully check the reputation of a car service before starting repair work. After their completion, if possible, it is necessary to check the operation of all units and components of the machine.

After their completion, if possible, it is necessary to check the operation of all units and components of the machine.

Damage to vehicles during the washing process cannot be recognized as an insured event. True, the car owner will be reimbursed if it is known for certain which of the car wash employees damaged the car. At the same time, such a citizen must fully admit his guilt.

In addition, factory defects are worth mentioning. If the insurance company proves that the damage to the car was the result of a manufacturing defect, the car owner will not be paid anything. In this case, you should file a claim with the automaker, because it is he who is responsible for damaging the car.

Customers of insurance companies often complain about the refusal to repair certain minor damages. Meanwhile, they forget about the natural wear and tear of the car. Constant operation of the machine will certainly lead to minor damage to the paintwork and glazing. In particular, most insurers do not pay for the repair of the following defects:

In particular, most insurers do not pay for the repair of the following defects:

Accidents due to the ingress of various objects, animals or water into the internal cavities of the car are equally considered. In the latter case, it is worth highlighting the water hammer. Such an event is not included in the number of insured events, even when it occurred during a natural disaster.

In addition, you should not count on payment in case of breakage of parts. In particular, if the battery, alternator and power supply circuit are damaged due to a short circuit. The insurance company will pay for such damage only if it is the result of an insured event, such as a traffic accident.

As a general rule, damage to tires and rims is not a basis for payment when there is no other damage. In addition, if the car owner uses a winter set of tires, it should be insured as an additional equipment. Otherwise, the insurance company will refuse to pay for new tires, even if other elements of the car besides the wheels are damaged.

Otherwise, the insurance company will refuse to pay for new tires, even if other elements of the car besides the wheels are damaged.

The category of exceptions includes all cases of damage to the wheels off the road.

For example, when driving through a forest plantation, field or ice of a reservoir. In the latter case, the car owner will be denied the repair of any damage, because the failure under the ice does not apply to insurance events.

The above exceptions are typical for most insurance companies, but in any case, you should focus on the CASCO rules of a particular insurer. Each company can change the list of exclusions at its sole discretion.

Therefore, some of the exceptions described may not be in the insurance rules of an individual entity. At the same time, the insurer has the right to add additional reasons for refusing to pay out to the insurance conditions. Thus, only studying the CASCO rules will help to fully understand when an insurance company can legally refuse to pay damages.

BorisHof cooperates with leading insurance companies that successfully operate in the market and provide high quality customer service.

The company's specialists make every effort to ensure that the conditions of auto insurance are as transparent as possible. If the car is damaged, the insured event is settled without contacting the office of the insurance company.

Also, for the convenience of customers, a department for prolongation of insurance contracts was created in BorisHof.

OSAGO on-line

Breakdown insurance

Accessories insurance

Tire and wheel insurance

Property insurance

Customer insurance

Insurance

Leave your details and our manager will contact you shortly

The form is loading ...

Settlement of an insured event without the client contacting the insurance company, accompanying the client from the moment of contact (call) until the car is returned from repair

Providing the client with full and high-quality consultations on all issues related to the specifics of the settlement of insured events depending on the insurance program

Repair at the service station of the official dealer.

Large selection of reliable insurance companies

The most attractive conditions and special programs for our regular customers

Special offers for regional customers and owners of used cars

Special conditions for insurance of car parks owned by legal entities

Early notification of the need and conditions for extending the insurance contract

Attention!

Beware of scammers who pretend to be agents of Insurance Companies, employees of the Representative Office or employees of our company.

Contact only your personal managers, whose names you receive

no

License for voluntary personal insurance, with the exception of voluntary life insurance

Pyatnitskaya, 12, bld. You can get it on the website: www.ingos.ru

License for voluntary personal insurance, except for voluntary life insurance

SL No. 1209 dated 04.08.20

Address (location) Gakkelevskaya, d. -85-52/23

For more information, please visit: www..jpg) reso.ru

reso.ru

License for voluntary personal insurance, except for voluntary life insurance

SL No. 3972 dated May 11, 2017

Address (location)

115114, Moscow, Derbenevskaya embankment, 11, floor 10, office 12

Opening hours

from 09:30 to 18:30 (except weekends and public holidays)

Phone

8-800-333-8-800

More information can be found on the website: www. renins.ru

СЖ No. 3972 dated May 11, 2017

License for voluntary personal insurance, except for voluntary life insurance

СЛ No. 3972 dated May 11, 2017

Address (location)

115114, Moscow, Derbenevskaya embankment, 7, building 22, floor 4, office 13, com. 11

Opening hours

from 09.00 to 18.00 (excluding weekends and public holidays)

Phone

8 (495) 981-2-981

For more information, please visit: www.renlife.ru

SL No. 1427 dated 06/18/2018

License - for the implementation of voluntary property insurance and the commanding staff of the internal affairs bodies of the Russian Federation, the State Fire Service, employees of institutions and bodies of the penitentiary system, employees of the troops of the national guard of the Russian Federation

OS No. 1427-02 dated 06/18/2018

1427-02 dated 06/18/2018

License - for compulsory insurance of civil liability of vehicle owners

OS No. 1427-03 dated 06/18/2018 damage as a result of an accident at a hazardous facility

OS No. 1427-04 dated 06/18/2018

License - to carry out compulsory insurance of the carrier's civil liability for causing harm to life, health, property of passengers during transportation

OS No. 1427-05 dated June 18, 2018

License - for reinsurance

PS No. 1427 dated June 18, 2018

Address (location)

Russia, 115184, Moscow, 50 Malaya Ordynka, d. on the website: www.makc.ru

AlfaStrakhovanie JSC

Details of the company

OGRN

10277739431730

TIN

7713056834

CPP for location

772501001

CPP of the largest taxpayer of the Federal Tax Code of the Federal Tax Service of Russia 9000 9000 9000 according to the 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 9000 according deeds

СL No. 2239

2239

License for voluntary life insurance

СЖ No. 3447 dated August 10, 2018

License for voluntary personal insurance, except for voluntary life insurance

SL No. 2239 dated November 20, 2017 Shabolovka, 31B

Opening hours

from 9.00 to 18.00 (Sat/Sun from 9.00 to 18.00)

Phone

+7 (495) 788-09-99

For more information, please visit: www. alfastrah.ru

CJSC VSK

Company details

121552, Russian Federation, Moscow, st. Ostrovnaya, 4

Working hours

Mon–Thurs: 9:00–18:00, Sat, Sun: 09:00–16:45 (except weekends and non-working holidays)

Telephone

+7 ( 495) 784-77-00

You can get more detailed information on the website: www.vsk.ru

LLC Consent

Details of the company

OGRN

1027700032700

TIN 9000 7706196090 by location

770201001

Registration number in the Unified State Register of Subjects of Insurance Business

1307

License to voluntary life insurance

SZh No. 3511 dated 03/27/2015

3511 dated 03/27/2015

License to voluntary personal insurance, with the exception of voluntary life insurance,

2222 SL No. 1307 dated May 25, 2015

Address (location)

St. Petersburg, Torfyanaya Doroga, 7F

Working hours

Mon-Fri 09:00-20:00, Sat 10:00-19:00, Sun 10:00-18:00

Telephone

8 (800) 755-00-01

More You can get detailed information on the site: www.soglasie.ru

Tinkoff Insurance JSC

Details of the company

OGRN

102773

40

TIN

77082517

GRDs for

9000 771301 state register of subjects of insurance business0191

License for voluntary property insurance

SI No. 0191 of May 19, 2015

License for voluntary personal insurance, except for voluntary life insurance for the implementation of compulsory insurance of civil liability of vehicle owners

OS No. 0191-03 dated May 19, 2015

Address (location)

127287, Russia, Moscow, 2nd Khutorskaya street, 38A, bld. 800) 755-80-00

800) 755-80-00

You can get more detailed information on the website: www.tinkoffinsurance.ru

PJSC Energogaranta

Details of the company

OGRN

102773

0 9000TIN 9000 77050412222 9000 9000 by location

770501001

KPP The largest taxpayer

997950001

Registration number in the Unified State Register of Insurance Board

1834

license for voluntary life insurance of

NO

license for voluntary personal insurance, with the exception life

SL No. 1834 dated February 1, 2016

Address (location)

Moscow, Sadovnicheskaya embankment, 23

Opening hours

from 9:00 to 18:00 (except weekends and public holidays)

Phone

+7 (495) 737-03-30

You can get more detailed information on the site: MSK-garant.ru

Zetta Insurance LLC

Details of the company

OGRN

1027739205240

TIN

7710280644

GRDs for location

773001001001 9000 9000

checkpoint of the largest taxpayer

773001001

Registration number in the Unified State Register of Subjects of Insurance Business

1083

License for voluntary personal insurance, with the exception of voluntary life insurance

Sl No. 1083 of 06/24/2015

1083 of 06/24/2015

voluntary property insurance

SI No. 1083 dated June 24, 2015

Compulsory civil liability insurance of vehicle owners

OS No. 1083-03 dated 06/24/2015

Compulsory civil liability insurance of the owner of a hazardous facility for causing harm as a result of an accident at a hazardous facility

OS No. 1083-04 dated 06/24/2015

Compulsory civil liability insurance carrier for causing damage to life, health, property of passengers during transportation

OS No. 1083-05 dated 06/24/2015

compulsory state insurance of life and health of military personnel, citizens called up for military training, private and commanding staff of internal affairs bodies of the Russian Federation, the State Fire Service, employees of institutions and bodies of the penitentiary system, employees of the troops of the National Guard of the Russian Federation, employees of the enforcement agencies of the Russian Federation

OS No. 1083-02 dated December 23, 2019

1083-02 dated December 23, 2019

For reinsurance

PS No. 1083 dated June 24, 2015

Address (location)

121087, Bagration pr. 7, bldg. 11

Office hours on the website zettains.ru

Sales department:

Mon-Thu: 09:00-20:00, Fri: 09:00-19:00, Sat: 10:00-17:00, Sun: closed

Mon-Thu: 09:00-18:00, Fri: 09:00-16:45, Sat: 10:00-17:00, Sun: closed

OMTPL Claims Office:

Mon-Thu: 09:00-18:00, Fri: 09:00-16:45, Sat, Sun: closed

Opening hours of all offices on the site zettains.ru

Phone

+7 (495) 727-07-07

You can get more information on the website: Zettains.ru

LLC TIT

Details

OGRN

11074683380 9000

Inn TIN

Working hours

from 9:00 to 18:00 (except weekends and public holidays)

Phone

+7 (495) 967-86-12, +7(495) 274-01-00

You can get more detailed information on the site: www.titins.ru

GSK Ugrians

Details of the company

OGRN

1048600005728

TIN

8601023568

gearbox for

9000 86010101010101010101010101010101010IST taxpayer773601001

Registration number in the Unified State Register of Subjects of Insurance Business

3211

License for voluntary personal insurance, with the exception of voluntary life insurance

SL No. 3211 dated 08/26/2019

3211 dated 08/26/2019

address (location)

Khanty-Mansiysk, st. Komsomolskaya, d. 61

Working hours

from 9 to 18 (except weekends and public holidays)

Phone

8 (800) 100-82-00

You can get more information on the website: www.ugsk.ru

LLC Absolute Insurance

Details

OGRN

10277718719

77281788835

Checkpoint by location

772501001

Checkpoint of the largest taxpayer

772501001

Registration number in the unified state register of insurance business entities

2496

License for voluntary life insurance SJ

none

License for voluntary personal insurance, except for voluntary life insurance SL

none

Address (location)

115280, Moscow, st. Leninskaya Sloboda, 26

Working hours

from 9:00 to 18:00 (except weekends and public holidays)

Telephone

8 (495) 025-77-77

You can get more detailed information on the website: www. absolutins.ru

absolutins.ru

LLC SK “CONSTRUCTION-VITA”

Details of the company

OGRN

1027700035032

TIN

7706217093

gearbox for

9000 70201001KPP of the largest taxpayer

997950001

Registration number in the unified state register of subjects of insurance business

3511

License for voluntary life insurance

СЖ No. 3511 dated March 25, 2015

License for voluntary personal insurance, except for voluntary insurance

СЛ No. 3511 dated March 25, 2015

Address (location)

12910 Moscow st. Gilyarovskogo, 42

Working hours

Mon-Thurs from 9-00 to 18-00 except weekends and holidays, on Fri until 16-45 Moscow time.

Telephone

8 (495) 660-58-30

The Central Bank of the Russian Federation controls the Company's insurance activities. Official website address: www.cbr.ru

SL No. 1208 dated 08/05/2015

Address (location)

Moscow, Akademika Sakharova ave. 45-17:30 (except weekends and non-working holidays)

45-17:30 (except weekends and non-working holidays)

Phone

8 (495) 739-21-40

Company details

PSRN

102773

89TIN

7707067683

CPP according to the whereabouts of

502701001

KPP of the largest taxpayer

997950001

Registration number in the Unified State Register of Subjects of Insurance Bades "2 April 2017

License for voluntary personal insurance, except for voluntary life insurance

SL No. 0001 of June 06, 2018

Address (location)

119991, Moscow - 59, GSP-1, st. Kyiv, 7

Working hours

Mon.-Fri. from 9.00 to 18.00 (except weekends and non-working holidays)

Phone

7 (495) 926-55-55

Company details

PSRN

1027810229150

TIN

7812016906

CPP for location

783501001

Registration number in the Unified State Register of Insurance Subjects

1675

License to voluntary personal insurance, with the exception of voluntary life insurance,

Cl No.

There is an out-of-pocket expense. These plans are often sold by new car dealerships. The prices can range from $300 to $600 dollars.

There is an out-of-pocket expense. These plans are often sold by new car dealerships. The prices can range from $300 to $600 dollars. This delay may be an hour or an entire weekend. This means that you'll have to "ok" the tire replacement, and then hope it's authorized for the full amount, or drive on your spare.

This delay may be an hour or an entire weekend. This means that you'll have to "ok" the tire replacement, and then hope it's authorized for the full amount, or drive on your spare. There are also discrepancies on the tire and rim prices themselves, which in the end, may have to be supplemented by the service customer.

There are also discrepancies on the tire and rim prices themselves, which in the end, may have to be supplemented by the service customer. However, even in this case, especially if it's an expensive sport wheel, they may still attempt to repair it.

However, even in this case, especially if it's an expensive sport wheel, they may still attempt to repair it. "

"

Secondly, hub bearings, front end components: tie rods, spindles, ball joints, and a variety of other components may have sustained damage. In this case, auto insurance, which you are already paying for, will pay for everything-brand new.

Secondly, hub bearings, front end components: tie rods, spindles, ball joints, and a variety of other components may have sustained damage. In this case, auto insurance, which you are already paying for, will pay for everything-brand new.