Personal Finance

Content provided by Credible, which is majority owned by Fox Corporation. Credible is solely responsible for this content and the services it provides.

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as "Credible" below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

Dear Credible Money Coach,

I turned 66 in September 2020, and applied for my Social Security benefits. I understand that you have to pay taxes on money earned. I am still working. How does this work? What are the rules and tax laws that apply to someone in my position? Is there a limit on what you can earn that you don't pay tax on? Will there be a time that you can earn as much as you can or want and your earned income won't be taxed? — Ralph

Hi Ralph, and a belated happy birthday! Thanks for your great question. Social Security and income taxes are each complicated topics. Consider them together, and it’s not surprising that a 2018 survey by the Nationwide Retirement Institute found that 37% of retirees hadn’t factored taxes into their retirement planning.

Let’s break your questions down, starting with the last one first because it’s easiest to answer. It’s unlikely there will ever come a time when retired people will be able to earn as much as they want and never pay any federal income tax on it. That said, the federal tax code is intentionally written to lessen the tax burden on senior citizens in many ways.

Let’s look at how your earned income can affect taxation of your Social Security benefits.

What to know about your non-Social Security incomeIdeally, when you retire you don’t want Social Security to be your only source of income — largely because even the highest possible monthly benefit amount won’t be enough to cover all your expenses. Most other types of income you’ll have when you’re retired can be subject to federal income tax, and possibly state income tax if you live in a state that has an individual income tax (most do).

Other types of taxable income you may have in retirement include:

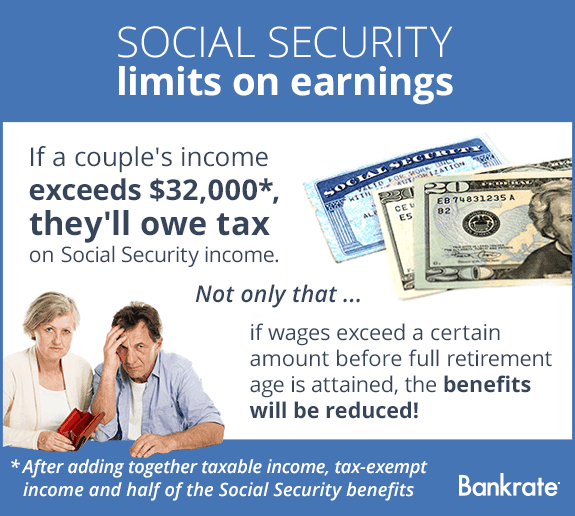

All your income combined, including the amount you get from Social Security, will determine if you have to pay federal income tax on your benefits — and, if so, how much of your benefits will be subject to taxation.

How your combined income affects tax on your Social Security benefitsTo determine what portion of your Social Security benefits may be subject to federal income tax, add up all your other sources of income — wages, interest, dividends, etc. — and add that to one half of your benefits. Then, compare that combined income total to a base amount the IRS sets for each filing status.

If your combined income is equal to or less than your base amount, you won’t have to pay federal income tax on any of your Social Security benefits. If your combined income total is more than your base amount, you may have to pay tax on some of your benefits.

If your combined income total is more than your base amount, you may have to pay tax on some of your benefits.

For 2020, the base amounts were:

Keep in mind, those base amounts could change for 2021 taxes.

So how much tax might you have to pay?If a portion of your Social Security benefits turns out to be taxable, you’ll have to pay federal income tax on either 50% or 85% of your total benefits. Which percentage applies to you will depend on how much your total combined income exceeds your base amount.

Here’s an example of how this could work:

The IRS has resources to help seniors navigate how federal income tax could apply to their Social Security benefits. Check out IRS Publication 915 and Publication 554: Tax Guide for Seniors.

Check out IRS Publication 915 and Publication 554: Tax Guide for Seniors.

And of course, your earned income may also be subject to taxes, so it may be a good idea to consult a tax professional if you have any questions about your personal tax situation.

Need Credible® advice for a money-related question? Email our Credible Money Coaches at [email protected]. A Money Coach could answer your question in an upcoming column.

This article is intended for general informational and entertainment purposes. Use of this website does not create a professional-client relationship. Any information found on or derived from this website should not be a substitute for and cannot be relied upon as legal, tax, real estate, financial, risk management, or other professional advice. If you require any such advice, please consult with a licensed or knowledgeable professional before taking any action.

About the author:

Dan Roccato is a clinical professor of finance at University of San Diego School of Business, Credible Money Coach personal finance expert, a published author, and entrepreneur. He held leadership roles with Merrill Lynch and Morgan Stanley. He’s a noted expert in personal finance, global securities services and corporate stock options. You can find him on LinkedIn.

He held leadership roles with Merrill Lynch and Morgan Stanley. He’s a noted expert in personal finance, global securities services and corporate stock options. You can find him on LinkedIn.

Table of Contents

Table of Contents

How Social Security Is Taxed

How Much Untaxed Income?

Standard Deductions for Retirees

Tax Brackets for 2021 and 2022

The Bottom Line

By

Michelle P. Scott

Full Bio

Michelle P. Scott is a New York attorney with extensive experience in tax, corporate, financial, and nonprofit law, and public policy. As General Counsel, private practitioner, and Congressional counsel, she has advised financial institutions, businesses, charities, individuals, and public officials, and written and lectured extensively.

Learn about our editorial policies

Updated July 31, 2022

Reviewed by

Lea D. Uradu

Reviewed by Lea D. Uradu

Full Bio

Lea Uradu, J.D. is graduate of the University of Maryland School of Law, a Maryland State Registered Tax Preparer, State Certified Notary Public, Certified VITA Tax Preparer, IRS Annual Filing Season Program Participant, Tax Writer, and Founder of L.A.W. Tax Resolution Services. Lea has worked with hundreds of federal individual and expat tax clients.

Learn about our Financial Review Board

Fact checked by

Suzanne Kvilhaug

Fact checked by Suzanne Kvilhaug

Full Bio

Suzanne is a researcher, writer, and fact-checker. She holds a Bachelor of Science in Finance degree from Bridgewater State University and has worked on print content for business owners, national brands, and major publications.

Learn about our editorial policies

If you've been proactive, you've saved for retirement through an individual retirement account (IRA) and 401(k) plan. And you know that you'll get additional income from Social Security or through a pension. But what does this all mean for your tax bill when you leave the workforce?

Your tax liability during retirement all comes down to a few important factors, notably your:

As such, your yearly tax bill will affect how much money you really have to pay for your day-to-day expenses.

Having said this, it’s important to understand how your retirement income will be taxed. This information can help you plan for your future if you're still working. And if you've already retired, you may need to account for additional sources so you don't run out of money. Understanding how taxes will affect your retirement income can help you consider ways to minimize your tax bill and maximize your retirement income.

There's a good chance that you won't owe taxes on Social Security if it's the only source of income you receive during retirement. That's because your income will be too low to be taxable. But if you have other sources of income, including otherwise tax-exempt interest income, a portion of your Social Security benefits may incur a tax bill.

More than half of Social Security beneficiaries pay some tax on their benefits. The percentage of families receiving Social Security benefits who have to pay income taxes on them was less than 10% in 1984 and more than 50% by 2015. This figure may rise to 56% between 2015 and 2050, according to the Social Security Administration (SSA).

The percentage of families receiving Social Security benefits who have to pay income taxes on them was less than 10% in 1984 and more than 50% by 2015. This figure may rise to 56% between 2015 and 2050, according to the Social Security Administration (SSA).

The amount of your taxable Social Security benefits depends on your combined income or the sum of:

Common sources of gross income include wages, salaries, tips, interest, dividends, IRA/401(k) distributions, pensions, and annuities.Common adjustments to gross income include health savings account (HSA) contributions, deductions for IRA contributions, student loan interest deductions, and contributions to self-employed retirement plans.

The level of your combined income determines the portion of your Social Security benefits that is taxable. The following chart indicates the percentage of your Social Security benefits that will be subject to tax at different levels of combined income:

| Combined Income | Taxable Portion of Social Security |

|---|---|

| Individual Return | |

| $0 to $24,999 | No tax |

| $25,000 to $34,000 | Up to 50% of SS may be taxable |

| More than $34,000 | Up to 85% of SS may be taxable |

| Married, Joint Return | |

| $0 to $31,999 | No tax |

| $32,000 to $44,000 | Up to 50% of SS may be taxable |

| More than $44,000 | Up to 85% of SS may be taxable |

| Married, Separate Return | |

| $0 and up | Up to 85% of SS may be taxable |

This depends on a couple of factors, including the source of income and the total amount you receive. You may get distributions from 401(k)s and IRAs, Social Security benefits, pension payments, and annuity income. Some people may also continue to earn income from work, as an employee, or through self-employment, even though they may have retired from their regular or long-term employment.

You may get distributions from 401(k)s and IRAs, Social Security benefits, pension payments, and annuity income. Some people may also continue to earn income from work, as an employee, or through self-employment, even though they may have retired from their regular or long-term employment.

Unearned income may be subject to income tax and different tax rules. Ultimately, a retiree’s tax liability depends on the tax bracket in which they fall:

Both your income from these retirement plans and your earned income are taxed as ordinary income at rates from 10% to 37%. And if you have an employer-funded pension plan, that income is also taxable.

Distributions from plans funded using after-tax contributions are not taxed the same way as those funded with pretax dollars. Form 1099-R, which is sent to a taxpayer who made after-tax contributions to plans, reports both the gross amount distributed as well as the taxable amount.

Form 1099-R, which is sent to a taxpayer who made after-tax contributions to plans, reports both the gross amount distributed as well as the taxable amount.

IRAs, 401(k)s, and similar plans are required to make annual required minimum distributions (RMDs) to beneficiaries, beginning the year they turn 72 years of age. The RMD requirement was suspended for the 2020 tax year, in response to the pandemic, but was reinstated for 2021.

Income such as dividends, rents, and taxable interest from investments held outside IRAs, 401(k)s and similar plans are subject to tax at ordinary income rates of up to 37%. Capital gains rates apply to gains realized on the sale of investments. Long-term capital gains are taxed at low rates, ranging from a zero rate bracket to a rate of 20% for taxpayers with very high taxable incomes.

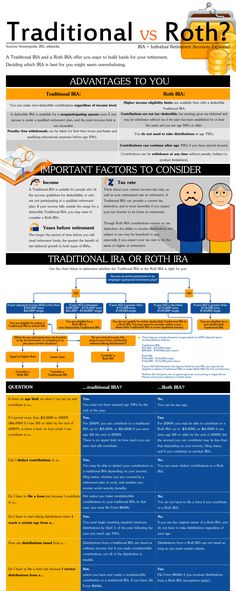

Roth IRA and Roth 401(k) distributions are not taxable. Roth plans, which are funded with after-tax dollars, do not have an RMD requirement.

While unearned income, such as income from pensions, IRAs, annuities, and other investments, is subject to income tax under rules that vary by the income’s source, earned income works a little differently. Any income you earn from regular employment and self-employment sources is subject to Social Security, Medicare, and income taxes.

Any income you earn from regular employment and self-employment sources is subject to Social Security, Medicare, and income taxes.

If you receive Social Security benefits and continue to work and earn income, you will have to pay Social Security and Medicare taxes on that earned income. However, if your total income (the sum of your earned income, unearned income, and Social Security benefits) remains low enough, you will not owe federal income tax on it. If your AGI is equal to or less than the standard deduction for your filing status, your federal income tax liability likely is zero.

The tax rates and tax liabilities for older people with earned and unearned income depend on the tax bracket that corresponds to their total taxable income. You determine your tax bracket in retirement the same way you did while you were working. Add up your sources of taxable income, subtract your standard or itemized deductions, apply any tax credits you’re eligible for, and check the tax tables in the instructions for Form 1040 and 1040 SR. You can also put all this information into a tax software program or give it to your accountant.

You can also put all this information into a tax software program or give it to your accountant.

The standard deductions for 2021 are used on tax returns filed in 2022. The standard deduction for 2021 is $12,550 for single taxpayers and married taxpayers filing separately, $25,100 for married taxpayers filing jointly, and $18,800 for heads of household. The standard deduction for married couples filing jointly increased for the 2022 tax year to $25,900, tp $12,950, and to $19,400 for heads of households.

Taxpayers who are 65 years of age or older (whether or not they are retired) are eligible for an extra standard deduction of $1,700 for 2021 ($1,750 in 2022) if they are single or heads of household (and not married or a surviving spouse) and an extra $1,350 for 2021 ($1,400 in 2022) per senior spouse if they are married filing jointly, married filing separately, or a qualified widow(er).

| Standard Deductions for Taxpayers Age 65 or Over, Tax Year 2021 | |||

|---|---|---|---|

| Filing Status | Standard Deduction | Senior Bonus | Total Deduction |

| Single | $12,550 | $1,700* | $14,250 |

| Married filing jointly or qualified widow(er) | $25,100 | $1,350 per senior spouse | $26,450 or $27,800 |

| Married filing separately | $12,550 | $1,350 | $13,900 |

| Head of household | $18,800 | $1,700* | $20,500 |

| Standard Deductions for Taxpayers Age 65 or Over, Tax Year 2022 | |||

|---|---|---|---|

| Filing Status | Standard Deduction | Senior Bonus | Total Deduction |

| Single | $12,950 | $1,750* | $14,700 |

| Married filing jointly or qualified widow(er) | $25,900 | $1,400 per senior spouse | $27,300 or $28,700 |

| Married filing separately | $12,400 | $1,400 | $13,800 |

| Head of household | $18,650 | $1,750* | $20,400 |

* If not a surviving spouse, otherwise $1,350 in 2021 and $1,400 in 2022.

If your taxable total income falls below these amounts, you won’t owe any taxes. You usually won’t even have to file a tax return (unless you are married filing separately), though you may want to anyway. Filing a return allows you to claim any credits for which you might be eligible, such as the tax credit for the elderly and disabled or the earned income credit. Filing a return also ensures that you receive any refund you may be owed.

Taxpayers who itemize deductions may not claim the standard deduction and bonus amounts. Recent increases in the standard deduction amounts mean the threshold at which older taxpayers benefit more from itemizing than taking the standard deduction is higher. These higher levels may affect your decisions about when to make charitable donations or pay other deductible expenses. You may be able to benefit from itemizing in some years if you can lump large itemizable expenses together so that they fall within a single tax year.

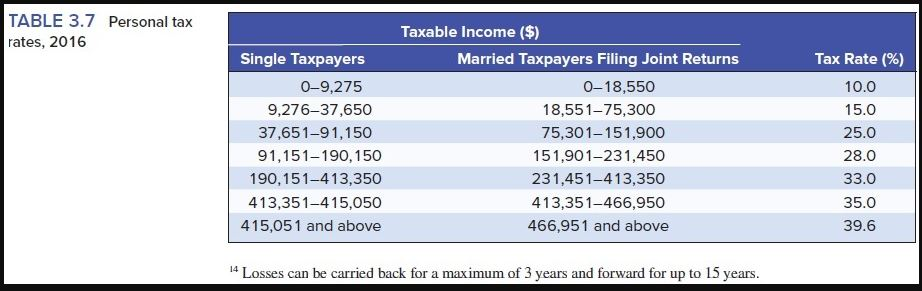

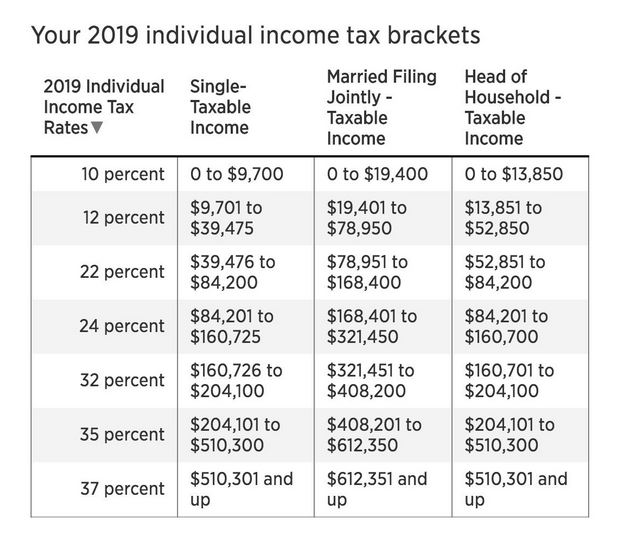

Below, you'll find the tax rates and brackets based on filing status and income thresholds for both the 2021 and 2022 tax years.

| Tax Brackets, 2021 | ||||

|---|---|---|---|---|

| 2021 Rate | Married Joint Return | Single Individual | Head of Household | Married Separate Return |

| 10% | $19,900 or less | $9,950 or less | $14,200 or less | $9,950 or less |

| 12% | $19,900 to $81,050 | $9,951 to $40,525 | $14,201 to $54,200 | $9,951 to $40,525 |

| 22% | $81,051 to $172,750 | $40,526 to $86,375 | $54,201 to $86,350 | $40,526 to $86,375 |

| 24% | $172,751 to $329,850 | $86,376 to $164,925 | $86,351 to $164,900 | $86,376 to $164,925 |

| 32% | $329,851 to $418,850 | $164,926 to $209,425 | $164,901 to $209,400 | $164,926 to $209,425 |

| 35% | $418,851 to $628,300 | $209,426 to $523,600 | $209,401 to $523,600 | $209,426 to $314,150 |

| 37% | Over $628,300 | Over $523,600 | Over $523,600 | Over $314,150 |

Marginal tax rates for 2022 don't change but the level of taxable income that applies to each rate increases. The top rate of 37% will apply to income over $539,900 for individuals and heads of household and $647,850 for married couples who file jointly.

The top rate of 37% will apply to income over $539,900 for individuals and heads of household and $647,850 for married couples who file jointly.

| Tax Brackets, 2022 | ||||

|---|---|---|---|---|

| 2022 Rate | Married Joint Return | Single Individual | Head of Household | Married Separate Return |

| 10% | $20,550 or less | $10,275 or less | $14,650 or less | $10,275 or less |

| 12% | $20,551 to $83,550 | $10,276 to $41,775 | $14,651 to $55,900 | $10,276 to $41,775 |

| 22% | $83,551 to $178,150 | $41,776 to $89,075 | $55,901 to $89,050 | $41,776 to $89,075 |

| 24% | $178,151 to $340,100 | $89,076 to $170,050 | $89,051 to $170,050 | $89,076 to $170,050 |

| 32% | $340,101 to $431,900 | $170,051 to $215,950 | $170,051 to $215,950 | $170,051 to $219,950 |

| 35% | $431,901 to $647,850 | $215,951 to $539,900 | $215,951 to $539,900 | $215,951 to $323,925 |

| 37% | Over $647,850 | Over $539,900 | Over $539,900 | Over $323,925 |

Will you pay taxes in retirement? Unless your taxable income falls at or below the standard deduction level every year, you probably will. How much you’ll pay is another story. There are many ways to help retirees minimize their tax burden. Strategies include timing distributions, bunching income, bunching deductions that can be itemized, and doing retirement account conversions.

How much you’ll pay is another story. There are many ways to help retirees minimize their tax burden. Strategies include timing distributions, bunching income, bunching deductions that can be itemized, and doing retirement account conversions.

Article Sources

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in our editorial policy.

Internal Revenue Service. “Don’t Forget, Social Security Benefits May be Taxable.”

Social Security Administration. “Retirement Benefits,”

Social Security Administration. “Retirement Benefits, 2022.” Pages 12-13.

Social Security. "Income Taxes And Your Social Security Benefit."

Internal Revenue Service. "IRS Provides Tax Inflation Adjustments for Tax Year 2022."

"IRS Provides Tax Inflation Adjustments for Tax Year 2022."

Internal Revenue Service. "About Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, Etc."

Internal Revenue Service. "Retirement Plan and IRA Required Minimum Distributions FAQs."

Internal Revenue Service. "Topic No. 409 Capital Gains and Losses."

Internal Revenue Service. "Roth Comparison Chart."

Internal Revenue Service. "Publication 554: Tax Guide for Seniors," Page 12.

Internal Revenue Service. "IRS Provides Tax Inflation Adjustments for Tax Year 2021."

Internal Revenue Service. "RP-2021-45," Page 14.

Internal Revenue Service. "Credits and Deductions for Individuals."

Internal Revenue Service. "IRS Provides Tax Inflation Adjustments for Tax Year 2021."

What Is Federal Income Tax? Definition, Tax Brackets, and Rates

What You Need to Know About Your 2022 Personal Income Taxes

Steps To Take Before You Prepare Your Taxes

State Income Tax vs. Federal Income Tax: What's the Difference?

Federal Income Tax: What's the Difference?

How to Find the Best Tax Preparer for You

Tax Preparer vs. Software: How to Choose

H&R Block vs. TurboTax vs. Jackson Hewitt: What’s the Difference?

Best Tax Software

How to Owe Nothing with Your Federal Tax Return

6 Strategies to Protect Income From Taxes

Capital Gains Tax 101

12 Top Sources of Nontaxable Income

Will Moving Into a Higher Tax Bracket Give Me a Lower Net Income?

The Most Overlooked Tax Deductions

Standard Deduction in Taxes and How It's Calculated

What Are Itemized Tax Deductions? Definition and Impact on Taxes

Tax Credit: What It Is, How It Works, What Qualifies, 3 Types

Retirement Plan Tax-Prep Checklist

Will You Pay Taxes During Retirement?

How Retirement Account Withdrawals Affect Your Tax Bracket

Deadlines for 2022 Estimated Taxes

Top Tax Filing Mistakes—and How to Avoid Them

Reasons to File an Early Tax Return

How to File for a Tax Extension

What Is a Tax Refund? Definition and When To Expect It

Tax Refund Anticipation Loan (RAL)

7 Reasons You Haven’t Received Your Tax Refund

Cheap Ways to Get a Tax Refund Faster

Can the IRS Audit You After a Refund?

Know the Sneakiest IRS Scams

The Truth About IRS Tax Settlement Firms

fi

fi If you are employed in Finland by a Finnish employer, you will accumulate a work pension (työeläke) in Finland, the part of your salary that will be paid to you in the future with interest in the form of a pension.

In addition to the labor pension, under certain conditions, you are also entitled to other Finnish social benefits, such as medical and family benefits.

Aivar lives in Estonia and travels to Finland to work on a construction site. Aivar has a Finnish employer. Aivar spends the week in Finland and spends the weekend in Estonia. The Finnish employer is obliged to insure Aivar in the Finnish social system. All statutory contributions must be made in Finland.

In Finland, occupational pension insurance is provided by law, i. it is obligatory for all, and is entrusted to the Finnish funds and institutions of labor pension insurance.

Insurance is compulsory for everyone who works for wages in Finland as an employee or as an entrepreneur. The citizenship of the worker or the country of his taxation does not matter. Foreign workers are covered by the same statutory labor pension insurance as workers permanently resident in Finland.

The citizenship of the worker or the country of his taxation does not matter. Foreign workers are covered by the same statutory labor pension insurance as workers permanently resident in Finland.

The length of stay and work in Finland is irrelevant for the obligation to take out occupational pension insurance. The labor pension begins to accumulate from the first day of work in Finland. A labor pension is assigned even for a couple of weeks of work.

Having a job in Finland, receiving a salary for this job, which also pays taxes and pension contributions, is crucial. The amount of the pension insurance depends on the amount of the paid salary, which must be at least 62.88 euros per month (in 2022).

. Thus, the labor pension is accumulated even for small incomes in the form of wages.

Pension and accident insurance is arranged by your employer. For other benefits, you must apply on your own to the Finnish social security Kela.

For other benefits, you must apply on your own to the Finnish social security Kela.

An employer is required to take out labor pension insurance for all of its employees aged 17-68. The pension will be accumulated on the basis of tax and pension contributions made by him to the institution of labor pension insurance.

You have the right to ask your employer for proof of your insurance. For more information about the accumulated pension or for assistance with pension insurance, please contact the Finnish Pension Center Eläketurvakeskus.

Your pension rights in Finland do not expire. Even after several decades have elapsed since the time you worked in Finland, the accumulated pension then remains and belongs to you. The amount of the accumulated pension is adjusted by annual indexation.

If you come to Finland as a posted worker of a foreign employer, see the page “Lähetetty työntekijä – Posted worker” for more information.

If you work in both Finland and Estonia, see page "Työskentely useassa maassa - Working in several countries".

If you are living in Estonia, you should contact the Estonian Social Insurance Institution Sotsiaalkindlustusamet for questions about foreign social security and obtaining an A1 certificate.

Estonian official institutions will also assist you in applying for a pension accumulated in Finland and advise you on how the Finnish pension paid to you may affect your Estonian social benefits.

Coordinates Sotsiaalkindlustusamet

Social Insurance Institution Sotsiaalkindlustusamet

st. Endla 8

EE-15092 Tallinn

ESTONIA

Tel: +372 612 1360

E-mail E-mail: info(at)sotsiaalkindlustusamet.ee

www.sotsiaalkindlustusamet.ee

If you live in Finland, please contact the Finnish pension authority Eläketurvakeskus for questions about pension insurance and employment pensions. Applications for A1 certificate are also submitted to Eläketurvakeskus. Tel. +358 29 411 2110 (Finnish/English)

Applications for A1 certificate are also submitted to Eläketurvakeskus. Tel. +358 29 411 2110 (Finnish/English)

email Email: asiakaspalvelu(at)etk.fi

www.etk.fi

For other questions about social security and social benefits (sickness benefits, child allowances) in Finland, please contact Kela's social welfare office.

www.kela.fi/web/en

Regularly check how much pension you have accumulated for work performed in Finland.

You can check your pension status by registering with your Finnish bank codes here or by contacting Eläketurvakeskus.

Online service only available in Finnish or Swedish.

An extract from the pension register indicating the status of the pension can be requested from the Eläketurvakeskus Service Department in writing or by calling +358 29 411 2110.

pension accumulated on the basis of other non-wage benefits.

Don't forget to keep all supporting documents for work done in Finland, such as employment contracts, payroll and pay stubs. This may be required when checking the status of the pension and processing the start of its payment.

This may be required when checking the status of the pension and processing the start of its payment.

On the basis of the contributions to the labor pension fund deducted from your earnings in Finland, in the future you will be paid the Finnish labor pension. As savings, these contributions are non-refundable, even if you leave Finland before retirement age.

The Finnish work pension will be paid to you regardless of your citizenship and transferred to any country of residence.

When you reach retirement age, you can request that your retirement pension start. In Finland, the retirement age is 63-68 years. Starting from 2017, the minimum retirement age for persons born at 1955 and after - gradually increases to 65 years. After that, the retirement age depends on life expectancy. If incapacity for work occurs before retirement age, then an application for the beginning of the payment of a pension can be submitted immediately.

Payments to the labor pension fund are made by the employer, employee and entrepreneur. The employer makes contributions to the labor pension fund, but at the same time withholds from the salary of his employee his share of labor pension contributions. The entrepreneur fully makes all pension insurance payments for himself.

The employer makes contributions to the labor pension fund, but at the same time withholds from the salary of his employee his share of labor pension contributions. The entrepreneur fully makes all pension insurance payments for himself.

The amount of the labor pension contribution is approved annually. So, in 2022, it averages 24.85% of the amount of wages paid.

At the same time, 7.15% of the amount of the salary paid to him is deducted from the salary of an employee up to the age of 53 and over 62 years old, and 8.65% from the salary of an employee over 53 years old, up to the age of 62 years.

Entrepreneur's pension contributions in 2021 amount to 24.10% up to the age of 53, and after the age of 53 and up to 62 years - 25.6%, over 62 years - 24.10%.

At the age of 17, a pension is accumulated in the amount of 1.5% of the annual salary.

Temporarily until 2025, 1.7% is accumulated for people aged 53-62.

In the case of continuing to work at an age older than the minimum pension age, an additional 0. 4% bonus per month for postponing retirement is added to the already accumulated pension.

4% bonus per month for postponing retirement is added to the already accumulated pension.

From the amount of labor earnings, which are available in addition to the received pension, 1.5% per year will be accumulated in the form of a pension, regardless of age. Pension accumulation stops at the end of the calendar month in which one turns 68 years old.

Finnish work pension, työeläke work pension – provides security in the event of old age, disability or loss of a breadwinner.

Starting from 2018, the minimum retirement age for persons born in 1955 and younger is increased from 63 by three months a year until it reaches 65, i.e. in 2027, after which the retirement age will depend on the increase in age. As an old-age pension, a labor pension accrued for the length of service is paid. The longer the service, the larger the pension.

If you live in Finland when you retire and your work pension savings remain low, you can receive the so-called work pension in addition to your work pension. national pension (kansaneläke) and guarantee pension (takuueläke). For more information, see Finnish social security Kela.

national pension (kansaneläke) and guarantee pension (takuueläke). For more information, see Finnish social security Kela.

If you have worked in Finland, you can receive a disability pension (työkyvyttömyyseläke) in Finland.

Disability pension is granted in case of reduction or loss of ability to work due to illness, injury or defect for a period of at least one year.

In the event of forced retirement due to an accident at work or an occupational disease, an accident pension (tapaturmaeläke) is calculated. In addition to contributions to the labor pension fund, the employer is also obliged to make contributions to the accident and occupational disease insurance fund specified in the legislation.

Family pension provides a guaranteed income in the event of the death of a spouse (registered and common-law marriage) or a guardian. Family pensions are also widow's or widower's pension and children's pension. All these pensions make up the family pension and mutually influence the size of the pension.

All these pensions make up the family pension and mutually influence the size of the pension.

For more information on work pensions and other pension benefits, contact the Finnish Pension Center Eläketurvakeskus, and on accident pensions, the Association of Insurers Tapaturmavakuutuskeskus.

Information about other types of pensions, such as national and guarantee pensions, from Kela's social security authorities.

The payment of the Finnish labor pension työeläke is processed by completing a pension application. An application for a pension must be submitted in advance, two months before retirement.

The Finnish labor (old-age) pension is applied for at the earliest after reaching the minimum pensionable age, which is determined by the year of birth.

If you live in Finland, you can apply for both a work pension and a national pension with one application. If you have also worked in Estonia, you can apply for an Estonian pension with the same application. The relevant application will be forwarded by the Finnish pension authorities to Estonia.

The relevant application will be forwarded by the Finnish pension authorities to Estonia.

For application forms and instructions on how to complete them, see the English section of this online service.

If you live in Estonia, claim your Finnish pension with your Estonian pension application. The relevant application will be forwarded by the Estonian pension authorities to Finland. In Estonia, contact the Social Insurance Office Sotsiaalkindlustusamet.

In Finland, a pension application can be submitted to any private or public pension fund, Eläketurvakeskus Pension Center or Kela Social Security. There you can also get instructions and advice on how to apply for a pension.

Your pension decision is made by the pension institution that contributed most of your earnings in the previous two years. The same pension institution will also pay your pension and respond to inquiries about the pension decision.

Below are the ways in which income is calculated for the eligibility test:

Please note that the amounts in the examples are for illustration purposes only and are not actual benefit amounts.

(valid from 01/01/2020)

You receive old-age and/or survivors' benefits and have no additional income. The amount of benefit income to qualify for the Living Wage Supplement is NIS 3,799. (starting from 01.01.2022) per person and NIS 6,002 (starting from 01/01/2022) for a married couple.

For example:

both spouses in a couple receive old-age benefits: the husband's benefit is NIS 1,500, the wife's benefit is NIS 2,000. The sum of the two benefits is NIS 3,500. per month. The couple has no additional income. The maximum living wage allowance per couple will be NIS 5,000. Since the couple has benefit income, they will receive a partial increase after their benefits are deducted.

Since the couple has benefit income, they will receive a partial increase after their benefits are deducted.

The amount of the allowance to which they are entitled : 5,000 - 3,500 = 1,500 NIS

You receive benefits and also have income from work.

The maximum amount of income from work that can qualify for a living wage supplement is NIS 2,479. (starting from 01/01/2022) for one person or NIS 2,902 (starting from 01/01/2022) for a married couple.

If your income from work exceeds the above amounts, we will deduct 60% of your remaining income.

For example:

you are not married and receive an old age benefit of NIS 2,000. and have an income from work of NIS 2,500. The allowable income from work for a single person is NIS 2,000.

The living wage supplement is NIS 3,000.

We will subtract the allowable income from the income from work and multiply the remainder by 60%. From the amount of the subsistence minimum allowance for a single person, we subtract the result obtained after multiplication and the total amount of the old-age allowance:

From the amount of the subsistence minimum allowance for a single person, we subtract the result obtained after multiplication and the total amount of the old-age allowance:

2.500 - 2.000 = 500

60% x 500 = 300

3.000 - 2.000 - 300 = 700

The amount of the allowance for which is the right (not in marriage) a person is 700 N.Sh.

You receive benefits and also have pension income.

The amount of income from a pension that allows you to receive a benefit supplement is NIS 1,372. (starting from 01/01/2022) for a single person and NIS 2,163 (starting from 01/01/2022) for a married couple.

If your pension income exceeds the allowable amount, we will deduct the balance from your allowance supplement.

Example:

Spouse receives an old-age benefit of NIS 2,000.

Both spouses' pension income is NIS 4,000.

The allowable pension income for both spouses is NIS 2,500.

Amount to be deducted: 4,000 - 2,500 = 1,500

The amount of the couple's subsistence allowance is NIS 5,000.

The amount of the supplement to which a married couple is entitled is 5,000 - 2,000 - 1,500 = 1,500 n.s.

You receive benefits and have income from work. To check how these incomes affect your eligibility for a living wage supplement, use the calculator.

If you have income from financial assets or property and the total amount of all income from these sources and from benefits from the National Insurance Institute does not exceed the amounts shown in the table, you may be eligible for a living wage supplement.

For more information, see the "Property" section.

If you have savings, cash deposits or a reserve fund of an amount not exceeding NIS 36,060 (starting 01/01/2022) for an unmarried person or NIS 54,090 (starting 01/01/2022) for a married couple, you may be eligible for a living wage supplement.

For more information, see the "Property" section.

Owners of a vehicle (including a motorcycle), as well as permanent users of a vehicle without owning it, may be eligible for a living wage supplement if the value of the vehicle is below NT 60,000 .w (starting from 01/01/2022).

If you are the owner of a vehicle that is worth more than the indicated amount, or you own two vehicles, even if they are worth less than NIS 60,000. (starting 01/01/2022), you may only be eligible for a supplement in certain cases. For more information follow the link.

The cost of the vehicle is set according to the Leki Yitzhak (Mechiron) price list, as well as according to the data specified in the driver's license, such as brand, year of production, owner, etc.

More information can be found in the "Vehicle" section.

Under certain conditions, it is possible to receive a living wage supplement even while living abroad, but there are some restrictions.