Skip to Content

Anyone, 6 months of age and older, is eligible to receive the COVID-19 vaccine. Find your nearest vaccination location at vaccines.gov.

| Aircraft Use Tax (non-retailer purchased from non-retailer) | The rate is 6.25% of the purchase price or fair market value, whichever is greater. If you acquire the aircraft by purchase from a person or business that is not in the business of selling aircraft at retail, you must pay tax on the aircraft’s purchase price. If the aircraft’s purchase price is less than the fair market value, you must pay tax on the aircraft’s fair market value on the date acquired or the date brought into Illinois, whichever is later. If you acquire the aircraft by gift, donation or transfer, you must pay tax on the aircraft’s fair market value on the date acquired or the date brought into Illinois, whichever is later. If you acquired and used the aircraft outside Illinois before you brought it into Illinois, you will receive a credit for tax properly due and paid to another state. |

|

Private Party Vehicle Use Tax

(RUT-50) (non-retailer purchased from non-retailer) | The rate is determined by either the purchase price or fair market value of the motor vehicle. Fair market value is used when there is no stated price (e. If the vehicle purchase price is $15,000 or more, the tax is based on the purchase price. Use Table B. In addition, there is a flat rate of $25 for purchases of motorcycles and all-terrain vehicles (ATV’s), and $15 for purchases from certain family members, gifts to beneficiaries (not surviving spouses), and transfers in a business reorganization if the beneficial ownership has not changed. See the Private Vehicle Use Tax Chart for more information. See RUT-6, Form RUT-50 Reference Guide, to determine whether your purchase or transfer is subject to a local private party vehicle use tax administered by the Department on behalf of certain municipalities and counties. |

| Use Tax | Use Tax rates are 6. You are allowed credit for sales taxes paid to another state; however, if you pay tax to another state at less than the Illinois rates, you must pay Illinois the difference. |

| Vehicle Use Tax (RUT-25 and RUT-25-LSE) | Click here to look up the Vehicle Use Tax rate based on location |

|

Watercraft Use Tax (non-retailer purchased from non-retailer) | 6.25 percent of the purchase price or fair market value, whichever is greater If you acquire the watercraft by purchase from a person or business that is not in the business of selling watercraft at retail, you must pay tax on the watercraft’s purchase price. If the watercraft’s purchase price is less than the fair market value, you must pay tax on the watercraft’s fair market value on the date acquired or the date brought into Illinois, whichever is later. If you acquire the watercraft by gift, donation or transfer, you must pay tax on the watercraft’s fair market value on the date acquired or the date brought into Illinois, whichever is later. If you acquired and used the watercraft outside Illinois before you brought it into Illinois, you will receive a credit for tax properly due and paid to another state. |

Your ZIP Code

If you’re buying a new or used car, it’s important to know the taxes and fees you may have to pay. Illinois tax on new and used vehicles is generally 6.25% but can vary by location. See the chart below for more.

See the chart below for more.

Did you know comparing insurance quotes can save you hundreds on your auto insurance? Receive personalized rates and policy options in minutes by calling EverQuote at 833-494-0309. Tap here to call today.

Here are typical fees in Illinois:

DMV or State Fees | |||

| Vehicle sales tax (for vehicles sold by a dealer) | Usually 6.25% but can vary by location | Use the Illinois Tax Rate Finder to find your tax | |

| Vehicle use tax (for vehicles purchased from another individual or private party) | Usually 6.25% but can vary by location | Use the Illinois Tax Rate Finder to find your tax | |

| Title Transfer Only Fee | $25 | ||

| Title and Transfer Fee | $175 ($150 title fee plus $25 transfer fee) | ||

| Vehicle Registration Fee | $150 | ||

| License Renewal Sticker |

| ||

| Local municipal and county private party use taxes | Local Tax Information | Some regions such as the City of Chicago and Cook county have additional Use Taxes on the purchase of a vehicle. Refer to the local tax information link for the most up-to-date information. Refer to the local tax information link for the most up-to-date information. | |

| Gift Tax | $15 | Instead of Use Tax, if the transaction meets one of the following:

| |

| Motorcycle or ATVS | $25 | ||

Dealership Fees | |||

| Documentation Fees | $179.81 | Charged to cover administrative costs of the dealer related to the title, registration and other paperwork. | |

| Advertising Fees | Negotiable | Check your invoice to see if your dealer is adding on fees related to their advertising. You may be able to negotiate these fees. You may be able to negotiate these fees. | |

Miscellaneous | |||

| Vehicle History Report Fees | Varies by provider | It's wise to get a vehicle history report when purchasing a used car. If your dealer doesn't provide one, there are plenty of companies you can use such as Carfax and AutoCheck. | |

| Pre-sale inspection | Varies by inspection company | A pre-purchase inspection is often done for used cars. The purchaser usually pays. An inspection can uncover flaws that could change your decision to buy the car. | |

You have to pay a use tax when you purchase a car in a private sale in Illinois. The tax rate is based on the purchase price or fair market value of the car. Here’s a vehicle use tax chart.

You typically have to pay taxes on a car received as a gift in Illinois. You will need Form RUT-50 to report the gift. You may qualify for a tax exemption if:

You will need Form RUT-50 to report the gift. You may qualify for a tax exemption if:

Updated Oct. 10, 2019

Your ZIP Code

Each state's tax laws are a set of legal "rules" that govern the amount of taxes that state, local, and federal governments levy each year. It covers procedures, policies and penalties for everything related to tax matters. Entrepreneurs interested in registering a company in the United States should be aware that Congress drafts Internal Revenue Code ( IRC ), which regulates the collection of taxes, compliance with tax rules, and the issuance of tax refunds. Internal Revenue Service ( IRS ) is the government agency within the US Treasury charged with these functions.

The US ranked 21st in 2021 in the international tax competitiveness ranking. The strength of the US tax system is that States fully cover the cost of business investment in equipment. Corporations can deduct property tax when calculating taxable income. Some weaknesses in the American tax system:

Opening a business in the US today is quite a popular request among foreigners. The tax system in America is 3-tier. The government receives most of the nation's revenue from income tax.

| Federal | Regional | Local |

| Corporate income tax | ||

| personal income tax | ||

| Tax payments on certain types of products (excises) | Inheritance tax | |

| Customs fees | Property tax | |

| Inheritance tax | Motor vehicle tax | Environmental tax |

| Contributions to the social fund insurance | Sales tax |

|

After registering a company in the USA, the following applies at all levels: personal income tax and CIT. In table. The percentage (%) of tax revenues is clearly shown below.

In table. The percentage (%) of tax revenues is clearly shown below.

| Taxes | Federal | Regional | Local | All levels |

| KPN | 6 | 6 | 1 | 5 |

| personal income tax | 50 | 21 | 4 | 37 |

| Soc. insurance | 34 | 27 | 6 | 27 |

| Excises | 8 | 37 | 14 | 15 |

| Property tax | - | 1 | 71 | 10 |

| Other | 2 | 8 | 4 | 6 |

| Total | 100 | |||

If you are an alien doing a trade/business in the US, you must pay tax on your effectively tied income, after allowable deductions, at the same rates that apply to US residents. If you are not engaged in a trade/business, U.S. taxes only apply to income derived from sources in that jurisdiction that is fixed, determinable, annual, or periodic, subject to flat rate tax.

If you are not engaged in a trade/business, U.S. taxes only apply to income derived from sources in that jurisdiction that is fixed, determinable, annual, or periodic, subject to flat rate tax.

The Tax Reform Act, passed December 22, 2017 (PL 115-97), moved the United States from a "worldwide" to a "territorial" taxation system. Among other things, PL 115-97 reduced the CIT rate from 35% for resident corporations to a flat rate of 21% for tax years beginning after December 31, 2017. Income of non-U.S. residents is taxable depending on whether it is related to the United States, on the extent to which non-residents are present in the States.

| Changes in CIT from 2021 | Indiana has been gradually reducing the CIT rate since July 2012, and the last scheduled phase of this reduction came into effect in July 2021, when the rate was reduced from 5. If you are interested in registering a company in Montana , please note that the state of is among the growing ones, where the CIT proportional distribution formula is applied, which takes into account sales more than payroll and property. The state has also taken steps to reduce the income tax rate and other reforms, although these changes will not take effect until January 1, 2022. |

| Changes in personal income tax from 2021 | Idaho. Draft Law No. 380, signed in May 2021, contains provisions that came into force on July 1 of the same year. Specifically, the new law creates the Idaho Tax Relief Fund and directs the state to distribute a lump sum refund to taxpayers equal to 9% of 2019 personal income tax paid.d. Rate cuts, resulting in max. corporate and personal income tax rates decreased from 6.925% to 6.5%, introduced retroactively from the beginning of 2021 |

| 2021 sales and use tax, gross receipts tax changes | Florida. Kansas. In July of this year, the Kansas Economic Interconnection Act for Remote Sellers and Market Intermediaries went into effect. This law requires remote merchants and marketplace operators to collect state and local sales taxes if their annual gross state sales revenue exceeds $100,000. New Mexico. Several notable changes have occurred in the sales tax when registering a company in New Mexico. This refers to the so-called tax on gross receipts and, in some way, a hybrid traditional tax on retail sales. |

Corporate income tax ( CIT ) is a fee that is levied on the net profit of corporations and is calculated as the excess of income over allowable costs. All states levy income tax, but the rates differ from country to country. Those wishing to set up a company in America will benefit from knowing that until 2022, PL 115-97 allows for a full write-off of most new investments, after which this benefit is phased out until 2026. PL 115-97 limits deductions for net interest expense to 30% of adjusted taxable income.

PL 115-97 limits deductions for net interest expense to 30% of adjusted taxable income.

PL 115-97 also introduced fundamental changes to the US taxation of multinational corporations and their income from foreign sources. Prior to the passage of the Act, dividends distributed by foreign subsidiaries to their US parent companies were subject to US tax on foreign income taxes paid - a "worldwide" system. Now 10% gains on certain investments in qualified business assets are exempt from further taxation in this jurisdiction - the so-called "territorial" system.

CIT ranges from 1% to 12% at the state level. Some states do not charge it. If you are interested in registering a corporation in the United States, you should know that corporations are subject to CIT on global profits. C/S Corp corporate income is subject to double taxation. Corporation taxes are paid initially, and then dividends are paid to shareholders, which are subject to capital gains tax. Dividends must be reported on the shareholder's personal tax form. When registering an LLC in the United States, the system of double taxation is not applied, and taxes are payable only on those incomes that are received in the States.

When registering an LLC in the United States, the system of double taxation is not applied, and taxes are payable only on those incomes that are received in the States.

Important!

Registering an S corporation in the United States allows you to receive CIT exemption if the S-Corp has up to 100 eligible shareholders. However, foreign entrepreneurs can register a C corporation in the US, but cannot form an S corporation. The highest CIT rate in the US is shown in the chart below.

Taxable income of foreign companies is calculated based on effectively related income ( ECI ) from a trade/business or sale of real estate in the States by a foreign entity. The ECI tax exemption can be applied through a tax treaty. Foreign companies are subject to 30% branch income tax on ECI not invested in US trade/business and 30% withholding tax on non-ECI US source income (e. g. dividends, rents). Other arrangements may be in tax treaties.

g. dividends, rents). Other arrangements may be in tax treaties.

When deciding to register a company in the US, focus on the fact that CIT is paid in 44 states. In the vast majority of states, state taxes are significantly lower than federal taxes.

When registering a business in New Jersey, CIT is paid at the highest rate of 11.5%, followed by Pennsylvania (9.99%), Iowa and Minnesota (9.8% each). CIT in North Carolina (2.5%) is considered the lowest. Registering a company in Delaware or Virginia is subject to gross income tax in addition to CIT. South Dakota and Wyoming levy neither CIT nor tax on gross receipts.

Read also: Corporate taxes in Asia

Personal taxes play a key role in increasing America's income. This tax is levied on citizens and residents on their worldwide income. Nonresident aliens are taxed on income from sources in the United States and income related to trade / business in the United States (there are exceptions). For physical persons max. the income tax rate for 2022 is 37%, excluding long-term capital gains and qualifying dividends. PL 115-97 reduced both individual tax rates and the number of tax categories.

For physical persons max. the income tax rate for 2022 is 37%, excluding long-term capital gains and qualifying dividends. PL 115-97 reduced both individual tax rates and the number of tax categories.

When planning to open a company in the US, please note that personal income tax is collected in 42 states. Top 10 states (or jurisdictions) with the highest income tax for 2022:

Only 7 states have no personal income tax (Wyoming, Washington, Texas, North Dakota, Nevada, Florida, Alaska). How does the tax burden of physical. individuals in the United States are shown below.

VAT is the most common consumption tax in the United States. Sales tax is a tax applicable to the retail sale of tangible personal property and certain digital products and services listed. Although the form of the tax may vary, it is usually levied directly on the receipts from the retail sale of the object of taxation.

Sales tax is a tax applicable to the retail sale of tangible personal property and certain digital products and services listed. Although the form of the tax may vary, it is usually levied directly on the receipts from the retail sale of the object of taxation.

Sales and use taxes are the main source of state revenue. Rates range from 2.9% to 7.25%. Most states allow a "local option" that allows cities and counties to charge an additional percentage on top of the state tax. If you are interested in doing business in the US, you should be aware that sales tax is levied in 45 states (except Oregon, New Hampshire, Montana, and Delaware) and the District of Columbia. Alaska charges the lowest rate at just 1.76%.

Based on a combination of state tax and average local sales tax, the top five states for total sales tax as rated by the Tax Foundation are:

Leaders in combined sales and income taxes. According to ranking data, the top five states with the largest combination of state and local taxes are:

Since 2005, the same states have consistently been in the top three.

Each state has its own way of estimating the taxes that finance various state items. budget. Property taxes are considered one of the key sources of revenue for local governments. This tax applies to the assets of individuals and corporations. After registering a company in the United States, real estate taxes are paid at specific intervals (for example, annually).

All goods imported into the United States are importable and duty-free or duty-free according to their classification in the US Harmonized Tariff Plan. The classification determines eligibility for special programs and preferential rates under a free trade agreement. Responsibility for the payment of duties and other customs fees becomes fixed at the time of application to US Customs and Border Protection ( CBP ).

The classification determines eligibility for special programs and preferential rates under a free trade agreement. Responsibility for the payment of duties and other customs fees becomes fixed at the time of application to US Customs and Border Protection ( CBP ).

Excise taxes (including retail excise taxes) are generally levied at both the federal and state levels on a wide range of goods and activities, including the manufacture/importation of certain goods (for example, firearms and ammunition) and the retail sale of certain goods (for example, heavy vehicles). Excise tax rates vary, as do the goods and activities on which they are levied.

Corporations in the United States generally do not pay stamp duty at the state level, with the exception of the federal stamp duty levied on transfers of firearms under National Firearms Act ( NFA ).

These taxes are usually based on the value of the transferred property. The tax is levied on the direct sale of real estate, but some state and local governments levy such a tax on the sale of a controlling interest in real estate. Many state and local governments also levy stamp duty on certain items offered for sale in their respective jurisdiction.

Other taxes that the government may levy instead of or in addition to taxes on income include taxes on franchise and corporation capital. State. and council taxes are deductible expenses for federal CIT purposes.

Read also: USA: due diligence of technological M&A

Comparison of tax systems across countries reveals some interesting similarities and differences between individual jurisdictions and groups of countries. Of course, in order to compare and contrast how governments collect revenue, one must first decide which indicators to consider.

:no_upscale()/cdn.vox-cdn.com/uploads/chorus_asset/file/19915409/8_22_17highered_f2.png)

For entrepreneurs interested in setting up a business in the US, let's be a little clear on how the States compares to other developed countries in terms of total tax revenue. The common measure for this is total tax revenues on GDP. Another possible indicator is tax revenue per capita. For both indicators, some interesting trends can be observed.

Over the past 20 years, the average tax burden for OECD countries has been around 33.3%, ranging from 32% to 34%, without significant increases or decreases. Topping the list are countries such as Germany and France, collecting between 34% and 46% of GDP in tax revenue. Mexico's tax burden is at its lowest, ranging from just 11% to 16.6%. US tax burden 24.3% in 2019d.

As a percentage of total tax revenue, the US, Canada, Switzerland, and Australia rely heavily on CIT, with averages of 46%, 45%, 47%, and 57%, respectively. For other taxes, such as social security, property taxes, there are also quite significant differences between countries, which is also important to consider when choosing a country for company registration.

One of the contentious issues in America was the corporate income tax. Tax Cut and Jobs Act ( TCJA ) reduced CIT from 35% to 21% and introduced some provisions that should increase the repatriation of foreign income. Another issue to consider is at what level of taxation the government collects most of the tax revenue. The more centralized a country is, the more taxes are collected at the national/federal level. More decentralized countries collect taxes at the local and state levels. Countries such as Canada, USA and Switzerland collect about 34-49% of income at the subnational level.

The US has tax treaties with a number of foreign countries. Under these agreements, residents of foreign countries may be eligible to pay a reduced rate of tax or receive an exemption on certain items of income they receive from sources in the States. The provisions of the treaty, as a rule, are mutual (apply to both countries-participants of the treaty).

The article provides introductory information. To get answers to your questions, you can contact IQ Decision UK representatives and order a consultation on the specifics of registering a company in the United States.

Cities in Illinois have some of the highest sales taxes, including even a special Chicago tax on water. Illinois also has the highest sales tax on cigarettes in the entire country. However, cities and counties offer a long list of properties with property tax exemptions, as well as a flat-rate income tax of 5%.

Illinois Property Tax

The state of Illinois does not fund its budget through property taxes - all money goes only to local governments. According to the Illinois Department of Revenue, about 62% of local property taxes are invested in schools to promote education.

In Illinois, property taxes are paid on a next-year basis. Thus, the tax on property assessed as of January 1 will be paid next year (taxes on property assessed in 2011 are paid in 2012).

Thus, the tax on property assessed as of January 1 will be paid next year (taxes on property assessed in 2011 are paid in 2012).

Property is valued at 33.33% of its market value. Cook County (Chicago County) uses a computer model that determines a value based on a comparison of home sales history over the past five years and reduces the valuation of single-family homes to 16% of market value. Agricultural areas in Illinois are valued based on their ability to generate income (also known as agricultural value).

Property Tax Exemptions

The State of Illinois has some benefits that reduce your property tax by lowering the assessed value of your home. A General Homestead Exemption can be claimed up to $5,000 for single-family homes that are the owner's primary residence. A tenant who owns a home and is required to pay property tax may also qualify for this benefit. Long-Time Occupant Homestead Exemption is available to Cook County residents for long-term residence in one home that has been their primary residence for 10 years or more (5 years if the home was purchased through government assistance or non-profit programs and organizations). To qualify for this benefit, your income must be less than $100,000 per year. The maximum rebate amount is $10,000.

To qualify for this benefit, your income must be less than $100,000 per year. The maximum rebate amount is $10,000.

There are also benefits for retirees: a $2,000 deduction for disabled people, up to $70,000 for war invalids, and deductions for home improvement after natural disasters and emergencies.

In addition to exemptions, there is also a limitation on increases in property taxes from the previous year, known as the Property Tax Extension Limitation Law (or “tax caps”). This law limits the increase in total property tax to no more than 5% or a percentage of annual inflation (national Consumer Price Index) in the year preceding the tax year, which may be even less. If, in the opinion of local authorities, it is necessary to increase the amount of tax payments, then this restriction can be changed by voting.

Illinois Income Tax

Illinois has a flat income tax rate of 5%. It is one of seven states that has a fixed percentage regardless of your income level.

Additional Illinois State Taxes

Sales Tax : The state sales tax is 9.5% and is the third highest percentage in the entire US. Prescription and over-the-counter drugs, medical supplies and equipment, and certain food products are subject to a sales tax of only 1% . Local agencies are free to add their own sales taxes, which in some cases raise the overall percentage to 11.5%.

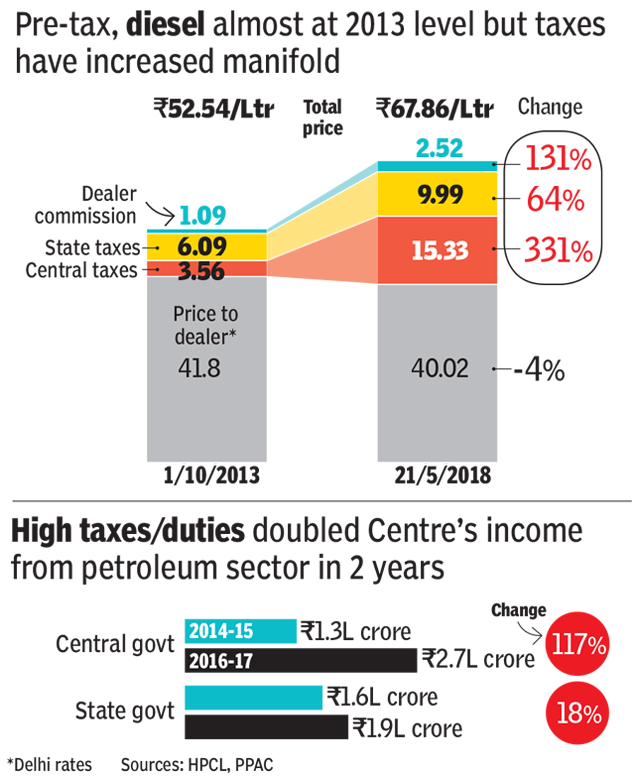

Gasoline Tax : $0.39 per gallon (3.78 liters) of unleaded gasoline. Chicago and Cook County are authorized to raise taxes by 5 cents and 6 cents. Diesel is taxed at 41.7 cents per gallon.

Cigarette Tax : 98 cents for a pack of 20 pcs. Illinois cities and counties may levy additional taxes of approximately $2.00. According to a survey by The Campaign for Tobacco-Free Kids, Chicago is the second-highest city in the nation at $90,003 $3.

25% of the purchase price of general merchandise and 1% of the purchase price of qualifying food, drugs, and medical appliances.

25% of the purchase price of general merchandise and 1% of the purchase price of qualifying food, drugs, and medical appliances. If you acquire a share of a watercraft, tax is based on the purchase price or fair market value of the share acquired. There is no provision for a trade-in allowance under Watercraft Use Tax. The tax due is based on the fair market value of the watercraft or share of the watercraft.

If you acquire a share of a watercraft, tax is based on the purchase price or fair market value of the share acquired. There is no provision for a trade-in allowance under Watercraft Use Tax. The tax due is based on the fair market value of the watercraft or share of the watercraft. 25% to 4.9%.

25% to 4.9%.  Effective July 1, 2021, Florida is among the states requiring remote merchants and marketplace operators to remit state sales taxes if annual sales exceed $100,000 (Senate Bill 50, passed April 2021). Missouri, the only state to not have such rules in the current legislature, passed similar legislation in May, but the state will not implement rules for dealing with remote sellers and resellers in the marketplace until 2023.

Effective July 1, 2021, Florida is among the states requiring remote merchants and marketplace operators to remit state sales taxes if annual sales exceed $100,000 (Senate Bill 50, passed April 2021). Missouri, the only state to not have such rules in the current legislature, passed similar legislation in May, but the state will not implement rules for dealing with remote sellers and resellers in the marketplace until 2023.  The changes came into effect on July 1 this year. According to the current legislation, the sale of tangible property is subject to state tax. rate of 5.125% with the corresponding rate of compensatory tax (tax on use). However, for the sale of services, the compensatory tax rate is lower, only 5%. From July 1, the state rate. of the compensatory tax on services will be increased to 5.125% to match the tax rate on goods.

The changes came into effect on July 1 this year. According to the current legislation, the sale of tangible property is subject to state tax. rate of 5.125% with the corresponding rate of compensatory tax (tax on use). However, for the sale of services, the compensatory tax rate is lower, only 5%. From July 1, the state rate. of the compensatory tax on services will be increased to 5.125% to match the tax rate on goods.