More people are retiring with less savings than they need to be comfortable. Much less. According to Northwestern Mutual, 21% of Americans have no retirement savings at all. The Government Accountability Office (GAO) says around 29% of households age 55 and older have neither retirement savings nor a pension.

These numbers may sound surprising and even daunting, but it’s important to remember that it’s never too late to save, even after retirement. Here are a few things you should know about saving money after retirement.

Retirement is on the rise. A 2018 report by Yahoo! Finance stated there are nearly 10,000 people turning 65 years old every day. Within the next 10 years, the number will reach nearly 12,000 people a day.

Americans are living, on average, more than two decades after the traditional retirement age of 65. A report by the Miami Herald found the average 65-year-old American man will live to be nearly 86 years old, while the average 65-year-old American woman will live to nearly 88 years old.

Nearly half of Americans aren’t sure how much they need for retirement. The 19th Annual Transamerican Retirement Survey, released in 2019, found 46% of Americans are guessing at how much money they need.

With increasing life expectancies and financial uncertainties leading up to retirement, here’s how to get on track once you’re retired.

One of the most impactful considerations for a senior’s quality of life is healthcare costs. Read our eBook, “The Complete Guide to Managing Elderly Healthcare Costs” for the financial insights you need to help you make an informed decision.

Download the Guide

It’s never too late to start saving. If you’ve retired and realize you haven’t saved enough, consider these ideas.

Maybe it’s not feasible to return to the last work position you once had. There are still work options available. You can take a part-time job in retail or hospitality. If you’ve always been the crafty type, start selling your artwork. You can work with a temp agency to get short-term work, and commit to saving part of what you earn.

There are still work options available. You can take a part-time job in retail or hospitality. If you’ve always been the crafty type, start selling your artwork. You can work with a temp agency to get short-term work, and commit to saving part of what you earn.

For those who were born in 1943 or later, there’s a strategy that will get your more Social Security. For every year you delay taking out benefits after you reach retirement age, your benefits increase by 8% until you reach the age of 70. You automatically save more money when you delay drawing Social Security.

If you own a home and have equity, you might consider a reverse mortgage. This type of loan is borrowed against the value of your home. You receive funds as a lump sum, a line of credit or a fixed monthly payment.

Consider what you own, what you need and what you’d be OK doing without. Maybe it’s selling a big home and moving to a senior retirement community, selling an extra vehicle or selling your designer clothes and handbags. Put what you make into savings.

Put what you make into savings.

According to Investopedia, once you turn 70½, you are no longer allowed to contribute to a traditional IRA. You can still contribute to a Roth IRA, however, so make sure you have one set up. If you do opt out of retirement and continue to work, you can contribute part of your salary to a 401(k).

If you do need to take out Social Security benefits, and you are married, you can still increase savings. The best way to do so is for the higher earner to delay claiming benefits longer and suspend paying contributions. The spouse with lower earnings can claim the spousal benefit. This tactic still results in savings, while also providing benefits.

Embrace your inner Golden Girl. Look for a roommate. You’ll get companionship, lower cost of living, help with housework (hopefully) and less space to take care of.

Take a look at your purchases over the past few months. Identify spending habits that you can eliminate. It might be a membership you don’t use any more, or maybe you start cooking more meals at home instead of going out to eat as often. Keep a diary to track your spending. Note extravagant purchases and see ways to save.

You could save tens of thousands of dollars a year in cost of living by moving to a new state, city or even country.

You spent years raising your children. If you have a good relationship with them, you can communicate your financial needs honestly with them and see how they can help. Other family members, like siblings, may be able to provide assistance, too.

The National Council on Aging has a benefits checkup website where you can view public programs that can help with decreasing your expenses. You may be eligible for benefits including care assistance, transportation, medical assistance and health care.

You may be eligible for benefits including care assistance, transportation, medical assistance and health care.

If your debt is too difficult to manage, talk with a financial advisor, credit counseling agency or bankruptcy lawyer to discuss your options. You may qualify for debt relief options that can help you better adjust to life in retirement.

You could well outlive the average life expectancy. The world’s oldest living person is Kane Tanaka, who will turn 117 years old in 2020. Save now by decreasing your lifestyle costs to ensure you have enough for the future. Use these techniques.

Managing your debt is a good first step to cutting lifestyle costs. In some cases, it may be better to keep debt like a home loan so that you have more to spend now. As mentioned, a reverse mortgage may be a viable solution that can help you save even more.

Seek out bargains and discounts

Seek out bargains and discountsCut coupons. Use deals websites. Take advantage of senior citizen discounts. The money you save adds up over time.

Using public transportation provides lots of benefits if it’s accessible to you. You can get exercise by walking to the transportation stop. You lessen your environmental footprint when you don’t drive a car. And it’s a nice way to get out in the community life and see some new sights along the way. If you use transportation like a subway or light rail, you’ll always know how long it will take you to get somewhere, since you don’t have to worry about traffic. That can reduce stress in your life, too.

Experiencing new homes away from home doesn’t have to be expensive. Check out destinations within driving range of your town. You might be able to encounter an entirely different climate and change of scenery just an hour away. Also, explore options like home-sharing services to save money on hotel rooms when traveling. Book vacations in off seasons to save more.

Book vacations in off seasons to save more.

There is no shame in seeking out financial help. There are numerous government and nonprofit programs designed for seniors. Do an online search for senior services in your city to see what’s available.

One of the easiest ways to save money is to prioritize your health. Preventive care is a big money-saver. The Centers for Disease Control and Prevention recommends that adults ages 50 years and older get at least 150 minutes of moderate-intensity aerobic activity a week, plus at least two strength-building sessions a week.

Get rid of things you don’t need by selling them online. There are tons of broad and niche online marketplaces like eBay and OfferUp where you can make some quick cash by selling your things.

Entertainment is nice to have, not a necessity. Life should be fun, though. Look for free entertainment options like art fairs or movies in the park. If you’re looking for entertainment because you’re bored, explore free or lower-cost hobbies, like yoga or reading books from the library.

Look for free entertainment options like art fairs or movies in the park. If you’re looking for entertainment because you’re bored, explore free or lower-cost hobbies, like yoga or reading books from the library.

Avoid stress about money in your retirement by consciously managing it. You’ll want to have a nice nest egg to continue enjoying life, pay for medical expenses and cover any emergencies that come up. Follow these steps.

Look at your spending over the past 3 months, using your banking statement. If you primarily use cash, write down what you think you spent on purchases. Start keeping a spending diary so you get an accurate view of your expenses.

Saving is always important, even after you’ve retired. In your budget, allot funds for savings. Try to build a solid emergency fund that could cover at least 3 months of your expenses in your savings.

Use the money-saving tips in this article to put those savings toward debt. Debt is stressful and can climb quickly when it builds interest. Pay off growing debts like credit card debt as soon as possible.

Talk with a financial planner about setting up guaranteed income, perhaps part of your retirement savings through a tool like a guaranteed annuity income. This way, you’ll still be generating income, even in retirement.

You’ll still owe taxes even when you’re not working. Work with a financial planner to get organized for taxes. Set aside money accordingly.

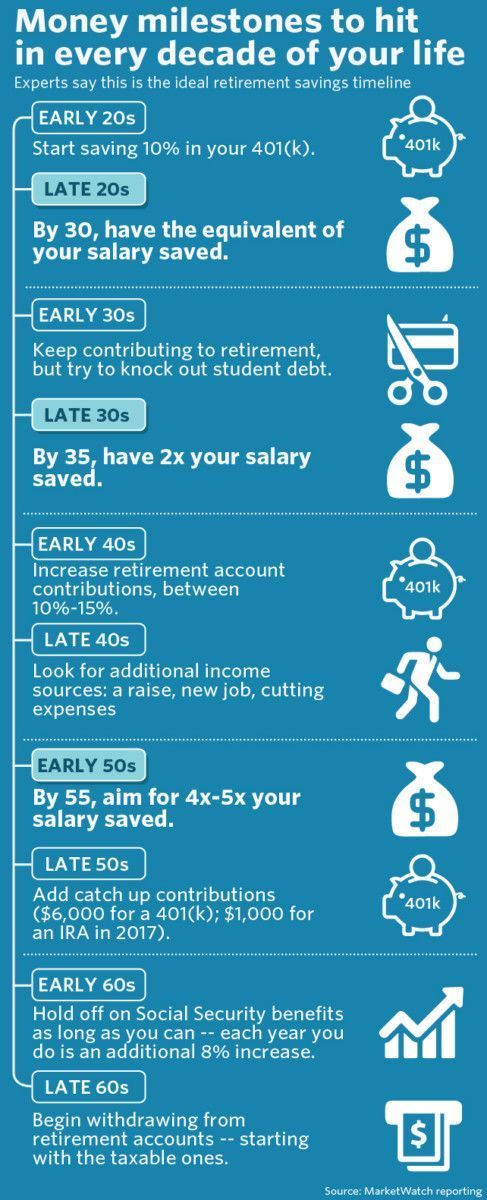

At this point in life, you’ll want to make less risky investments than you did when you first started working. But you’ll still want to invest. You can get a much higher return on investment by investing in stocks compared to waiting for a savings account to grow. After the age of 50, you can take advantage of catch-up contributions to IRAs and 401(k)s, too.

Look at the perks your current credit cards offer, like points for travel or cash back, and make sure you’re taking advantage of them. You might also consider signing up for a new credit card that has a bonus offer you want, like extra travel miles if you are planning a trip.

It’s not too late to start saving and maximize what you already have. Use these tips to make your retirement more comfortable.

*This content is for informational purposes only. This information should not be considered to be legal, tax, or tax advice.

Post retirement, you’re likely interested in various ways you can save money. Sure, you may have put money away in your retirement fund, and you receive social security, but it doesn’t mean your days of saving are over. You want to live that post-work life you’ve always dreamed of, right?

So what are some of the best ways to save money when you’re retired?

This was likely a necessity before retirement, but now that you no longer need to commute to work, consider selling a car. This will also save you money on your monthly car insurance.

This was likely a necessity before retirement, but now that you no longer need to commute to work, consider selling a car. This will also save you money on your monthly car insurance.

Make sure you’re shopping the sales when you create a meal plan. If there’s a good deal on a specific food, incorporate it into your plan for the week.

Make sure you’re shopping the sales when you create a meal plan. If there’s a good deal on a specific food, incorporate it into your plan for the week. There are plenty of tax-friendly states that will help you get the most out of your retirement savings. Florida, for example, has no state income tax. Similarly, Delaware doesn’t tax Social Security benefits—and it’s one of only four states with no state sales tax.

There are plenty of tax-friendly states that will help you get the most out of your retirement savings. Florida, for example, has no state income tax. Similarly, Delaware doesn’t tax Social Security benefits—and it’s one of only four states with no state sales tax.The need for healthcare as we age is sometimes overlooked (or perhaps ignored, as we may prefer not to think about it). You might be perfectly healthy now, but that could change in a number of years. And because of this, you need to be prepared. Some retirement communities, including Acts Retirement-Life Communities, offer healthcare to residents as they age. Acts also has on-site healthcare centers that rank among the top state and federal agencies.

Want to learn more about retirement community pricing? Select a community near you from this list and request an information kit.

The short answer is yes. You can absolutely maintain your lifestyle and save money while you’re retired.Not only that, but you can thrive in retirement – traveling the world, exploring new hobbies, and doing pretty much whatever you want. Assuming you follow the above steps and find ways to continue to save in retirement, your golden years can be whatever you want them to be.

You can absolutely maintain your lifestyle and save money while you’re retired.Not only that, but you can thrive in retirement – traveling the world, exploring new hobbies, and doing pretty much whatever you want. Assuming you follow the above steps and find ways to continue to save in retirement, your golden years can be whatever you want them to be.

Section: Your Most Important Asset

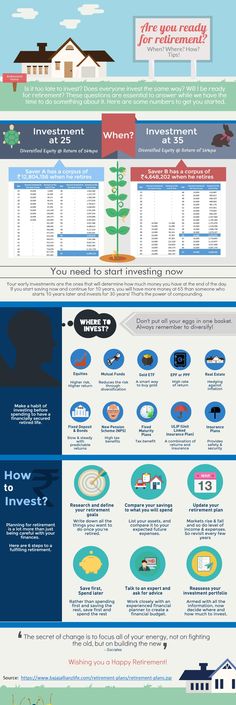

How does your income change when you retire? How much does the standard of living decrease with retirement? Answers in this article.

|

Listen to article | How your income changes when you retire is called the replacement (coverage) rate. It depends on how effectively you have transformed your human capital into financial capital over the course of your life. Don't rely on state pensions - currently they provide only 15-20% of current income. That is, your standard of living can decrease by 80-85%. |

In addition, rising prices (inflation) devalue your savings. To maintain the replacement rate, savings must be invested at a rate of return at least equal to inflation. Better yet, higher.

What can you do to secure an acceptable standard of living in retirement:

Method no. 1: consumption reduction.

Most people experience reduced consumption at retirement. The lack of funds (low replacement rate) leads to the fact that a person is simply forced to consume less. On the other hand, reducing consumption during the productive period of life allows you to increase the level of consumption in retirement, increasing the replacement rate.

The lack of funds (low replacement rate) leads to the fact that a person is simply forced to consume less. On the other hand, reducing consumption during the productive period of life allows you to increase the level of consumption in retirement, increasing the replacement rate.

Method No. 2: increasing the quality of human capital, or, to put it simply,

getting a person as much as possible salary.

A high salary, of course, will form a certain lifestyle, but in today's money for a comfortable life in retirement, a person would need 40,000 ₽ per month, which, with a salary of 100,000 ₽, implies a replacement rate of around 40%.

A higher salary will make it possible not only to increase the savings rate for retirement (say, by another 10%), but also to acquire all the necessary property in the course of work. However, this method only works if you invest your savings with a sufficient return.

Method no. 3: extending the savings period until retirement.

To do this, a person must either start saving as early as possible, or his parents must do it for him. Another option is a later retirement.

Method No. 4: investing in assets that have the potential to provide returns above inflation.

Maximizing the average annual return on investment is needed to offset the devastating effect of inflation. A person needs to choose such financial instruments that are potentially able to provide returns above inflation in the long run. This, as a rule, cannot provide a bank deposit or bonds. Among the available assets, only shares and real estate can be such instruments. This is confirmed by statistical studies of both the Russian and foreign markets.

Terminals

In order to ensure a comfortable standard of living in retirement, you need:

• invest funds with a return higher than inflation. This can be achieved by investing in stocks and real estate;

• save at least 20% of income;

• To carry out the transformation of human capital into financial (to save money for retirement) is necessary from the very beginning of employment. The more time left, the lower the savings rate can be.

The more time left, the lower the savings rate can be.

With an optimistic scenario and a personal savings rate of 20% of income, everything that you can “postpone” (save) in a year and a half of working life will provide you with approximately one year of retirement.

March 23, 2021, 12:00

4196

The CIS countries do not have the most reliable pension system: not everyone is ready to live on a $60 pension, having worked for more than 30 years. It's time to forget the "school - university - work - state pension" scheme.

In Western Europe, people start saving money from the very beginning of their career path. And in the post-Soviet countries, long-term planning is not developed, because the illusion of a feeling of a guaranteed future remains.

We describe strategies that will help you save up for a happy retirement and not worry about old age.

You save 70% of your income. Such a modest lifestyle suits those who earn significant amounts monthly. The method is gaining popularity: both among millennials and among older people. Some do not even buy new clothes, alter what they already have, buy cheap products. The story of New York lawyer Daniel, who earns $270,000 a year and spends almost nothing, was published by the New York Post.

But our task is to live until retirement, and not deny ourselves even food, right?

An old but inefficient way. You calculate how much per month you need to set aside to estimate the scale of the task. Everything would be fine, but there are factors that will prevent you from accumulating the required amount:

Achieving the goal is complicated by the fact that it is necessary not only to save, but also to invest in such a way as to circumvent inflation.

No work - nothing to postpone. While looking for a new one, live on savings. It makes sense to set aside a separate amount for an airbag. But will you pull?

Someone fell ill, a child was born, they sell tours at a discount - if the money is not enough, you will have to take it from your savings.

There are two types of dealing with securities: investment and trading. Investments are most often associated with the so-called buy & hold strategy (“bought and hold”). The task of the investor is to find the most undervalued but reliable stocks or other assets and buy them for the long term. The goal is to profit from the growth of their value, as well as through the receipt of dividends.

Trading in simple words is speculation on fluctuations in the market value of assets. If an investor, having invested money, relies solely on growth in the next 5–10 years or more, then a trader earns both on growth and on price reduction: every minute, hourly and daily.

The most popular securities are bonds and shares. The coupon yield on bonds is very low, but constant, its size does not change. Share payments depend on the company's dividend policy and, at times, the board of directors may decide not to pay dividends to shareholders. However, if we compare stocks and bonds, then stocks definitely win, since the yield on bonds, although fixed, is extremely low and hardly covers inflation. Shares, on the other hand, can grow by hundreds of percent over several years, and also bring additional income to the investor in the form of dividends.

There are also tokenized shares - these are tokens, the price of which corresponds to the price of a certain share

The token reflects the cost of a traditional asset and at the same time has a number of advantages of the blockchain:

For example, blockchain removes intermediaries from trade. To make transactions with tokens, no brokers, banks or custodians are needed. Two more pluses follow from this: a decrease in the number of commissions paid and an acceleration of the trading process.

To make transactions with tokens, no brokers, banks or custodians are needed. Two more pluses follow from this: a decrease in the number of commissions paid and an acceleration of the trading process.

So, 63-year-old pensioner Larisa Morozova has been investing in stocks for ten years and receives income from dividends. She visited 65 countries: Australia, New Zealand, the islands of Oceania, Chile, Peru, Brazil.

Today, deposits in banks do not bring much profit due to inflation. Therefore, people invest in cryptocurrency, an asset that, with the right approach, can bring huge profits.

Bank deposits, like bonds, are considered a risk-free asset class. Their main task is not so much to bring any income to investors as to protect capital. The safety of capital when investing in bonds is guaranteed by the state or the issuing company, in the case of a deposit, the guarantee is given by the bank. It is impossible to call bonds or deposits a 100% risk-free asset. The state can default as a result of a coup d'état, civil war, economic crisis and other events, even large companies can go bankrupt and banks lose their license. However, such events occur quite rarely, for this reason, the interest on deposits and coupon income on bonds (risk premium) are very low and, as a rule, close to the Central Bank rate.

The state can default as a result of a coup d'état, civil war, economic crisis and other events, even large companies can go bankrupt and banks lose their license. However, such events occur quite rarely, for this reason, the interest on deposits and coupon income on bonds (risk premium) are very low and, as a rule, close to the Central Bank rate.

Cryptocurrencies are a risky asset class, just like stocks. They do not guarantee the investor any profit, as well as the safety of capital, since they can either fall in price by tens of percent or grow by hundreds and sometimes even thousands of percent. However, it is thanks to investments in risky assets that investors get richer. In 2010, for just $1 you could buy 1310 bitcoins, which 10 years later are worth $76 million. Of course, there will be no such fantastic growth, but even now bitcoin is just starting to gain popularity, but not among ordinary people, the so-called enthusiasts, but among large investors who invest billions of dollars in cryptocurrencies.

Investor interest in bitcoin is related to many factors. Bitcoin is not in danger of license revocation, bankruptcy or default, it is not threatened with closure, since this coin is decentralized and does not belong to anyone. Simply put, the Bitcoin network is owned by every person who owns even the smallest amount of bitcoins. Its emission is limited to 21 million coins, 18.5 million of which have already been mined, and the rest will be mined until 2140. The scarcity of bitcoin and the high demand for it leads to an increase in its value over time. Against the backdrop of the non-stop operation of the printing press by the leading central banks of the world, which depreciate traditional currencies, bitcoin is an excellent protector against inflation.

As history and practice show, all risky assets grow in price over time. Accordingly, the most competent decision would be to invest money in cryptocurrencies and stocks for the long term - 10-15 years or more, until retirement.

This hinders the development of the industry, but in no way stops it.

This hinders the development of the industry, but in no way stops it. You can save money through a non-state pension fund. An organization that accumulates pension contributions, retains their value and pays out to contributors. NPFs do not pay taxes on their income, so they have no reason to earn on your deposits. But despite the security of investments in NPFs, the state does not guarantee the accumulated savings, as is the case with a bank deposit.

But despite the security of investments in NPFs, the state does not guarantee the accumulated savings, as is the case with a bank deposit.

You can rent an apartment and get a stable income or sell it. The disadvantages of this method are that in a small town it can be difficult to sell an apartment, and there are crises in the real estate market. In addition, you need to think of an additional way to earn money in case the tenants give up the apartment. You also need to take out property insurance.

Another way is to open a bank deposit. But the world is in crisis, and inflation is growing. Now this method is ineffective. The advantages are that the money is available, interest is charged, which can be added to the deposit so that the accrued interest is higher. The disadvantage is that there is a temptation to withdraw money and spend, and the regularity of replenishment of the account depends only on your willpower.

You will be paid the sum insured if you are alive by the date specified in the contract.